I recently read an article that described the typical human response when tackling the hardest problems in their fields. Apparently, people don’t like dealing with the hard stuff, and understanding this provides a fragment of insight into why we haven't seen enough interest in solving insurance in crypto.

Insurance is arguably the most important aspect of crypto at the moment, desperate for new metrics that show outrageously significant progress from where we are currently at.

If you’re wondering why, think of the last time crypto spent two months without news of a protocol’s vault being hacked… yeah, right.

Trust is slowly eroding as DeFi protocols and various types of smart contracts remain susceptible to attacks. In 2026 alone, between January and May, there were over 50 incidents, totaling over $840 million in losses, a 70% YoY increase over the same period in 2025.

This spells an obvious problem, that the current security infrastructure in onchain financial systems is weak, and users are vulnerable. But the hacks aren't the interesting part anymore; we seem to have normalized those. What's interesting is what happens after.

What about onchain insurance?

On April 18, an attacker drained KelpDAO's LayerZero bridge for 116,500 rsETH, about $292 million, the biggest DeFi hack of the year as of the time of writing.

The unbacked tokens were moved to Aave as collateral and used to open roughly $190 million in bad debt, triggering contagion.

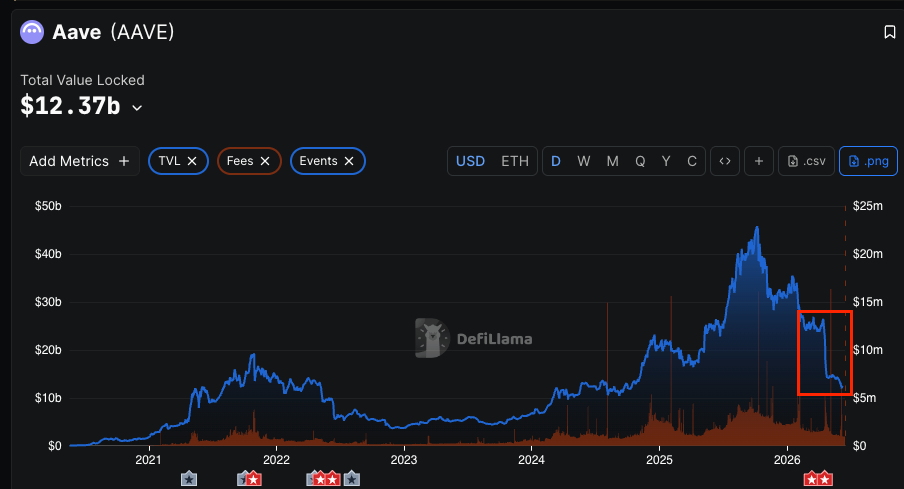

In response, Aave froze markets, causing a TVL decline from over $26 billion to under $14 billion in a matter of days. At the moment, Aave’s TVL is ~$12.3 billion.

Hacks like these affect multiple protocols and users; in KelpDAO’s case, at least 9 protocols were affected.

However, what specifically draws our attention is the industry's response after the attack.

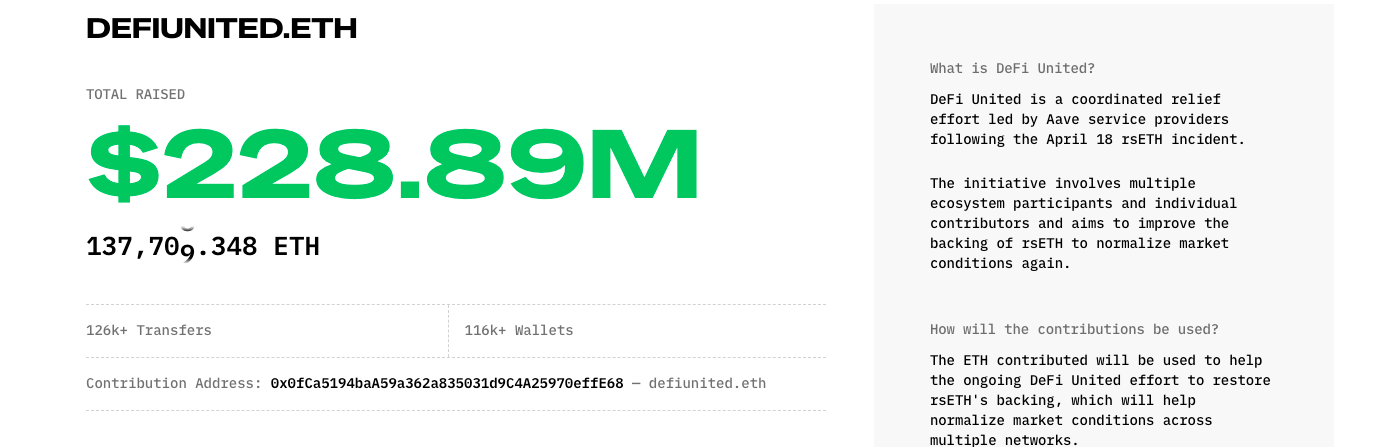

Any TradFi observer would have asked about insurance immediately and would have been surprised that the industry response was more of an improvized whip-round among the protocols that happened to be standing too close to the fire - DeFi United - a coordinated relief effort led by Aave service providers following the April 18 rsETH incident.

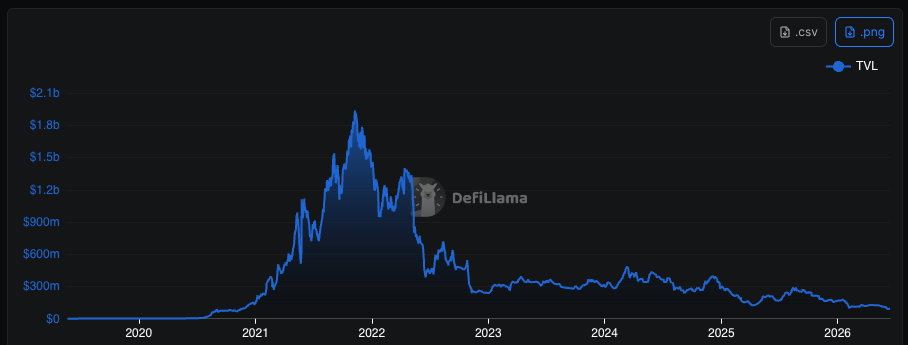

But this was expected. Crypto’s “insurance” industry has been on a decline. The total value locked across onchain insurance protocols is less than $100 million, falling from an all-time high of $1.9 billion in November 2021.

One reason for the decline may be that many early onchain insurance protocols were built as monolithic mutuals - a single shared capital pool backed a wide range of risks, while governance, underwriting, claims assessment, and capital management all sat bound inside the same system.

That structure simplified coordination, but it concentrated exposure and turned the protocol itself into a single point of failure.

Capital providers took losses across the entire portfolio rather than across clearly defined segments, which made it hard to isolate tail events, price exposure accurately, or allocate capital with any precision; when one position blew up, everyone in the pool bled, no matter what they thought they were underwriting.

In response, both old heads and new risk coverage protocols are beginning to borrow from traditional insurance, reinsurance, and structured finance.

The idea starts from a sharper question: who bears the first loss? Then it moves to segmenting capital by risk profile and building specialized pools or vaults so providers can choose the exposure they actually want.

The onchain insurance (protocol cover) landscape

In traditional insurance, equity or specific reinsurance layers often absorb initial losses. In early DeFi cover, staked capital providers (underwriters) typically bore first loss in a shared pool.

However, as we mentioned earlier, this is changing. Providers are now being allowed to choose their desired exposure between more conservative backstops and higher-yield or riskier tranches, while improving overall capital efficiency and capacity.

These are some of the protocols operating in this category.

Nexus Mutual

While Nexus Mutual remains an OG protocol in the onchain coverage economy, it has progressed into a more sophisticated risk-profiling system that allows its operation to layer coverage.

The way it works is that users buy “cover” (protection) against specific protocols, custodians, yield tokens, or de-pegs.

Capital providers stake NXM (or wrapped versions) to underwrite; they earn premiums but bear first loss on claims. These claims are assessed via member voting or structured processes.

Nexus’ risk products have extended beyond pure smart contract risk to custody, slashing, and even hybrid products like Crypto Kidnap and Ransom Cover (with traditional partners for response and ransom reimbursement).

Nexus Mutual currently segments capital across 70+ specific covers rather than one monolithic pool. Stakers bear the first loss, but diversification and efficiency tools reduce systemic pressure.

Nexus Mutual also partners with distributors like OpenCover for easier access and bundled products (e.g., “Base DeFi Pass” for multi-protocol coverage on Base).

OpenCover

OpenCover acts as the distribution and structuring layer for onchain insurance, simplifying access to coverage across multiple underwriters, with most capacity currently provided by Nexus Mutual.

Beyond aggregation, the platform is developing new risk-management products built on top of existing coverage infrastructure.

Its flagship product, Covered Vaults, was launched in partnership with Nexus Mutual, Morpho, Kiln, and Symbiotic.

Users can deposit into supported vaults and optionally activate protection by staking their vault shares, covering defined technical and economic loss events without leaving their underlying strategy.

OpenCover’s approach, “Covered Vaults,” moves DeFi insurance beyond standalone policies and toward integrated, portfolio-level risk management.

Firelight Protocol

Another interesting protocol is all the way over in the XRP universe - Firelight.

Firelight explicitly addresses the question of who bears the first loss while advancing capital segmentation and borrowing from traditional insurance and structured finance concepts.

The protocol allocates first-loss bearers to the stakers in the cover vaults. They bear the primary risk. Their capital directly backs payouts on valid claims, creating skin-in-the-game alignment similar to traditional mutual or pooled underwriting models.

Concerning capital segmentation and specialized structures, Firelight uses dedicated non-custodial vaults and cover pools rather than one monolithic pool.

This allows more granular risk exposure and capital allocation, with staked assets (especially large-cap, lower-correlation assets like XRP) chosen specifically for capital efficiency and resilience.

Built-in protections

While a few protocols take up the challenge of underwriting risks, most crypto or DeFi protocols are taking the built-in approach.

Platforms in this category design risk controls such as automated stop losses, liquidation buffers, and downside caps, into the core mechanics of leveraged tokens and yield vaults.

This shifts the burden of first-loss protection from external underwriters to the product architecture itself, allowing users to access higher returns while limiting tail exposure through programmatic rules.

Some examples:

Gearbox

Gearbox Protocol provides credit accounts for leveraged farming and strategies, incorporating liquidation protections and isolated risk layers within each account.

Dolomite

Dolomite delivers a money market with structured borrowing features and customizable risk parameters that limit overexposure.

Napier

Napier Finance tokenizes and structures yield positions with built-in mechanisms to isolate and manage specific risk components.

Toros

Toros Finance provides leveraged tokens with embedded stop-loss logic and recovery mechanisms that cap losses without requiring manual intervention.

This integrated approach draws from structured finance by engineering safeguards into the instrument itself.

It reduces friction for users seeking protection without purchasing separate policies and allows protocols to handle routine product-level risks more efficiently than broad mutual models.

Concluding thoughts on onchain insurance

In reality, the onchain risk coverage economy is still far behind in comparison with the rate at which exploits occur.

The gap is a lot, but the conversations are worth having. We believe that for onchain insurance to thrive, the industry needs to deviate from its obsession with the amount of value locked onchain (TVL), and pay attention to those calling for a more important metric in total value covered.

At the moment, under 2% of DeFi’s locked value is evidently covered. For trust to rekindle in DeFi, TVC is the metric to pay attention to, and the gap between what’s locked and what is covered is a huge opportunity for anyone who adequately solves crypto’s insurance crisis.

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)