.webp)

Reading time: 14m 37s

“67% of Polymarket profits goes to just 0.1% of accounts, while most traders are in the red. Most Kalshi users also lose money.”

I came across this headline a couple of days back while doomscrolling on Twitter.

Read that again: 0.1% of users.

Polymarket has at least 2.3 million total accounts. In the study behind the headline, roughly 1.6 million wallets were analyzed. That means fewer than 2,000 accounts walked away with nearly half a billion dollars in profits.

Meanwhile, the average user was down somewhere between $1 and $100, while the bottom 10% of traders lost ~$4,000 each on average.

The story is the same on Kalshi. Data from the past month shows that there are 2.9 unprofitable users for each profitable one.

In other words, people are donating to the markets.

Someone recently placed a bold $41,000 bet thinking hip-hop artist A$AP Rocky would say “rapper” during an appearance on The Tonight Show. The trader was set to win more than $168,000.

As it turns out, Rocky did say “rapper,” but that segment was edited out of the version that was broadcast on NBC.

As per Kalshi’s market rules, only what was said in the broadcast counted. Poor guy lost it all, but when asked if he’d go back to trading on prediction markets, he uttered, “Maybe.”

Despite the odds not being in favor of the masses, there’s something about prediction markets that keeps pulling us back into its arena.

Maybe it’s the adrenaline, the thrill of being early, being right, and turning conviction into profits. Or maybe it’s the sting of being wrong and the belief that the next trade could make up for every loss before it. Idk.

The lay of the land

Since the beginning of the year, weekly volume on Kalshi has been hovering between $800 million and $1.4 billion.

Meanwhile, for Polymarket, the number has been oscillating between $1.3 and $2.3 billion.

Things have gotten more interesting with the official rollout of HIP-4. If you have no clue what this alphanumeric phrase means, go give Emiri's breakdown a read.

TLDR: Outcome markets can now be traded on @HyperliquidX. The platform has already proved that its infra can comfortably support any type of perps trading, and now, it’s time to take the next leap.

Agree or not, HIP-4, in a way, is a direct shot at Polymarket and Kalshi.

This means, we've got three very different characters in the show now: the crypto-native OG (Polymarket), the regulated market leader (Kalshi), and the perps exchange that didn't get the memo that you're supposed to stay in your lane (Hyperliquid).

Before we get into the cage match, let's do a quick pulse check with respect to where things stand.

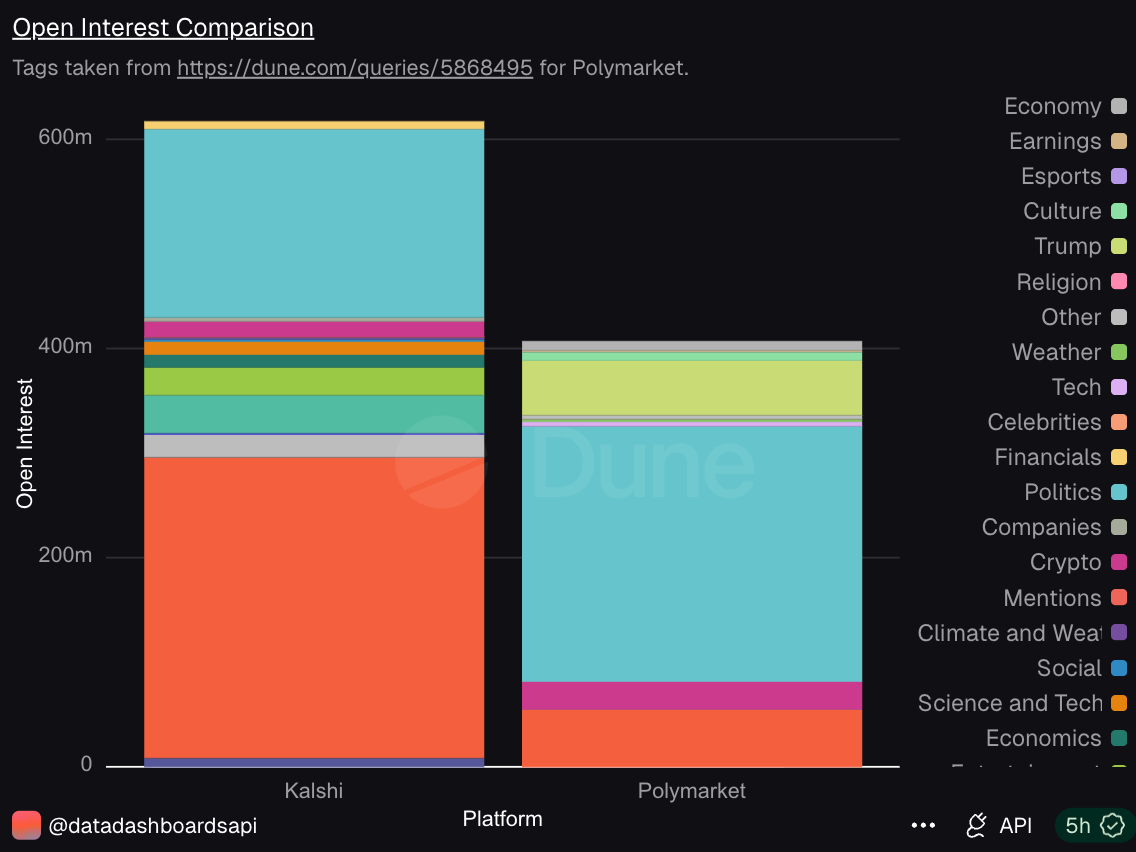

At the moment, you have markets to bet on almost everything you read or talk to your homies about. Economy, earnings, culture, tech, financials, religion, crypto, climate, science, tech, entertainment, health, exotics, the list is literally endless.

But on both Kalshi and Polymarket, sports (orange, below) and politics (blue) are among the dominant OI categories.

Kalshi and Polymarket generated around $44 billion in combined trading volume in 2025. To put that in perspective, that's more than the GDP of several small nations changing hands over what are essentially very fancy yes/no bets.

Both platforms have come a really long way. If you rewind a bit, you’ll find their monthly volume tagging below $100 million in early 2024.

From the funding POV, money has been flowing in without a hitch.

Polymarket has seen massive capital inflows, including a $2 billion investment from the NYSE's parent company (Intercontinental Exchange) at a $9 billion valuation, with talks ongoing for additional funding at $15 billion.

Kalshi has been in the same boat, too. Earlier this month, it announced a $1 billion Series F round, pushing the company’s valuation to $22 billion. Mind you, that’s a 2x jump in a span of just five months. The latest round was led by Coatue, with participation from Sequoia, a16z, and Paradigm.

Clearly, prediction markets are no longer a niche crypto playground. Despite the wins/losses, people are flocking en masse. The question remains: Will Hyperliquid be able to stand head-to-head with Polymarket and Kalshi and cement a position for itself?

How HIP-4 changes the game for Hyperliquid

Since this is the new one in town, let’s paint this side of the picture first.

One trend has been becoming increasingly prominent of late. Projects have been trying to steer away from crypto-first products. They’re instead moving towards fintech, with crypto merely being a part of the underlying rails.

As companies scale and refine their core business, they constantly look for new markets to sustain growth and meet evolving user demand.

Stepping into the prediction market was the next step in Hyperliquid's evolutionary curve. EOD, it wants to become the “house of all finance,” doesn’t it?

HIP-3 was a turning point for Hyperliquid. It enabled anyone to permissionlessly create a perp futures market on Hyperliquid’s Core infra. This turned Hyperliquid from a DEX into a permissionless financial infrastructure layer.

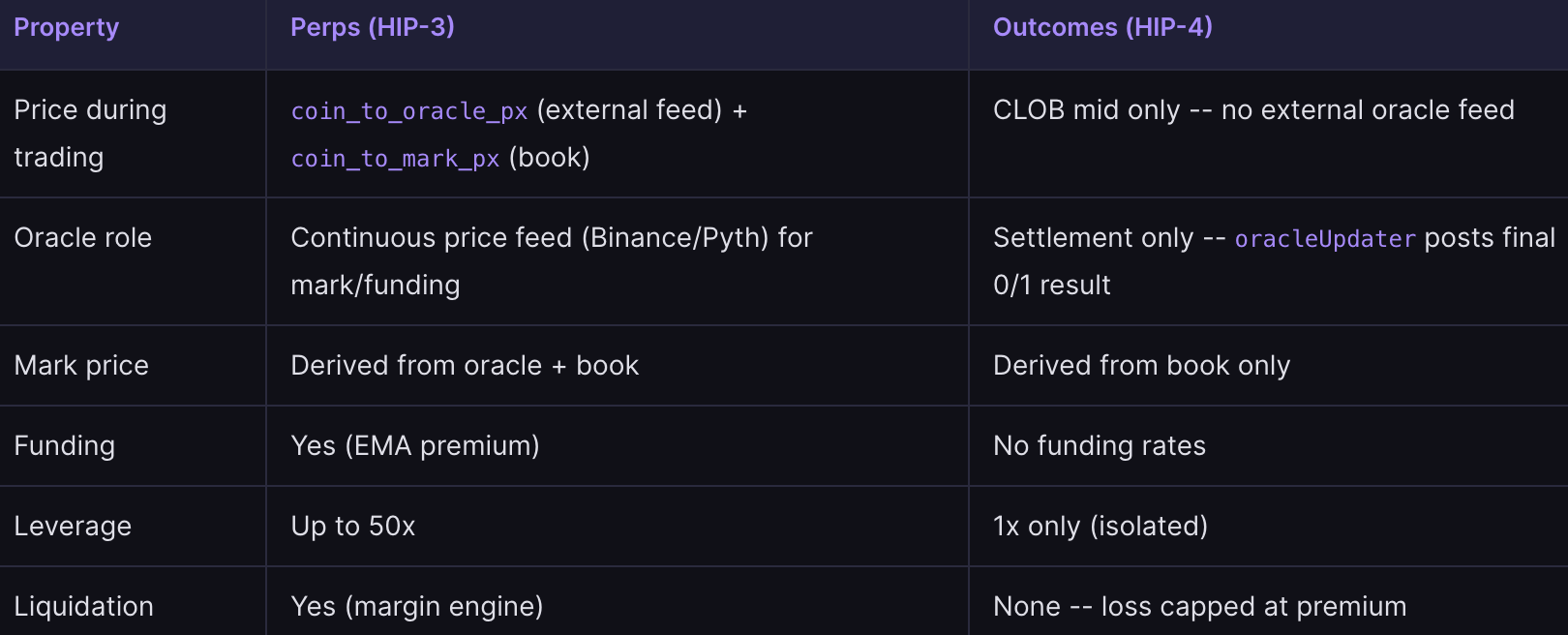

HIP-4 bifurcates into prediction markets and options; for the sake of this article, we’ll stick to the former.

Early data is modest. On launch day, HIP-4 contracts accounted for 0.7% of the day’s share.

And on the volume front, HIP-4 contracts clocked $19.2 million last week (ending May 10). Slowly, but steadily building momentum. The same is also reflected in the number of transactions, as depicted below.

HIP-4 event contracts are deployed through the same HIP-3 pipeline, but with different mechanics:

- 1x isolated margin only

- no leverage

- no liquidation

- no continuous oracle feed

- CLOB-based price discovery

- settlement happens via a deployer-designated oracle updater

Hyperliquid has registered more than $231 billion in additional volume via HIP-3, and conservative estimates suggest that the protocol can see upwards of $125 billion in annual volume through HIP-4.

HIP-4 markets: Different moves

There are four moves that you can make with your Hyperliquid prediction market position.

SplitOutcome:

Here, you deposit 1 unit of collateral > The protocol mints you 1 YES + 1 NO > You hold both sides of the bet > You choose your direction > Want to bet YES? Sell the NO > Want to bet NO? Sell the YES > Protocol splits the collateral > You’re allotted your side > The other side goes up for sale @ the complementary price > BUY YES at 0.40 = ASK NO at 0.60

MergeOutcome:

This is the reverse of SplitOutcome > You return 1 YES + 1 NO to the protocol > In exchange, you’ll get back one unit of your collateral > You don’t need to have a directional view, you don’t need to trade

Example: You hold 100 YES and 100 NO on "ETH above 4k". Suddenly, there’s a volatility influx, and you don't want to bet anymore. Instead of selling each side separately (two trades, pay fees twice), you can merge them. 100 pairs burned, USDH back in your wallet. Spick and span

MergeQuestion:

This works in multi-outcome markets > You can redeem a complete set across all outcomes in a question > Imagine a market with 4 possible outcomes for a particular question > You hold 1 token each, i.e., a complete set > One of them will settle at 1 (the right answer), the others at 0 (all wrong ones) > A complete set is always worth exactly 1 unit of collateral > Basically, instead of waiting for settlement, you’re cashing out immediately

NegateOutcome:

Via this, you can flip your position > YES becomes NO > NO becomes YES > You don’t have to sell one side to buy the other > Dual fee, slippage risk, everything gets eliminated

The edge(s)

On Kalshi and Polymarket, your prediction market trades are self-contained. But on Hyperliquid, that’s not the case. It brings DeFi composability to the table. You can provide liquidity, you can trade perps, you can trade spot, you can wager, all under the same roof.

You can simultaneously hold a BTC perpetual long, a spot ETH position, and a binary "BTC above X" outcome contract, all within the same Hyperliquid account, all backed by a unified collateral system.

UX-wise, however, Polymarket and Kalshi have an upper hand because, c’mon, who’d wanna go place yes/no bets on a trading interface?

There’s one big asterisk tho. Polymarket’s US return has been bumpy. They no doubt spent $112 million to buy a CFTC license outright, acquiring QCEX. Its US version kinda rolled out the beta, but but but, they have a large backlog of waiting customers. To top it all, their CEO is AWOL.

So if you’re from burger land and you want to bet on Fed rate decisions on Polymarket right now... buddy, get in line. There are a million people ahead of you. Literally.

The twist to the tale

I was going through a recent article by @0xFleck and found a few interesting data points (tho there are a few discrepancies):

- ~14% of top Polymarket traders are already active on Hyperliquid. They’re using the same wallets on both platforms

- These wallets generated $1.43 billion in Polymarket volume and are running $189 million in perp notional on Hyperliquid

- Mind you, these wallets are not gamblooors, they’re sophisticated trader wallets and use leverage

- The average user uses 7x leverage on their HL positions => Every idle dollar costs them $7

- To sustain their leverage positions ($189 million), these traders deploy around $27-$29 million in margin

- Contrarily, on Polymarket, mid-duration trades that remain open for a month sum up to $18.3 million. It’s just locked up there. It can’t necessarily be deployed anywhere else. No extra yield (in most cases)

- At 7x leverage, that comes up to $128 million in trades they're not making

- The dead capital on Polymarket keeps rising ($383-$451 million) as you increase the time duration (1-3 month bets, 3-6 month bets, 1+ year bets), and when you get back leverage to the equation to figure out how much you’re missing out on, the number further inflates

So from a capital efficiency perspective, instead of letting my capital idly sit on Polymarket, I’d rather deploy it on Hyperliquid and make it fetch me more.

These figures might not be exactly accurate, and there’s likely some noise in how they've been compiled, but they do give a rough idea of how and why the user base is converging. The boundaries are already starting to blur.

Another interesting thing to note at this juncture is that Kalshi’s head of crypto, John Wang, was a key contributor to the OG HIP-4 proposal.

So, it won’t be a surprise if Kalshi uses Hyperliquid to finalize/settle trades one fine day.

The fee battle

When it comes to fees, Kalshi sticks to a two-tier structure: 7% for takers and 1.75% for makers.

Takers are orders that match immediately. You cross the spread and take whatever is already sitting in the book.

Makers, on the other hand, are orders that wait. You set a limit price and let your order be fulfilled.

The 4:1 ratio between the two rates is Kalshi's way of incentivizing LPing. If you're consistently posting orders to get filled instead of crossing the spread, you end up shelling out way less.

The P x (1-P) part peaks when the outcome is most uncertain. Contrarily, it dips towards zero whenever a contract approaches near-certainty (in either direction).

So, a contract at 5¢ or 95¢ kinda indicates that it’s on the verge of being resolved. It carries almost no fee.

However, a contract at 50¢ means uncertainty is at its peak. It carries the maximum fee. So, if you're trading balanced 50/50 markets with market orders, Kalshi will eat into your edge.

So for 100 contracts at 50¢ you’ll bear $1.75 in taker fees.

If it’s at either 30¢ or 70¢, you’ll pay $1.47.

When you move towards 10¢ or 90¢, the fee freefalls to $0.63.

Maker fees at the same junctions would be: $0.44 at 50¢, $0.37 at 30¢/70¢, $0.16 at 10¢/90¢.

Polymarket uses a similar mechanism. Earlier this year, they launched something called “maker rebates.” Essentially, a part of the taker fees is refunded to makers daily. The ultimate motive is to incentivize deeper liquidity and tighten spreads.

Kalshi simply charges a lower maker fee right off the bat.

Taker fees on Polymarket fluctuate based on the share price. As depicted below, crypto attracts the highest rate, while sports falls in the bottom-most rung.

Markets that fall under the geopolitical and world events category are completely fee-free. Polymarket does not charge fees or profit from trading activity on these markets.

Meanwhile, on Hyperliquid, you’re not charged anything while opening outcome positions. You’re charged only while closing/settling.

Only fee-paying volume is counted for outcome trading, and the docs outline six scenarios (minting/burning permutations and combinations) that fall under the special cases.

Outcome trading doesn’t support rebates for makers. Users who’d receive rebates for spot and perp trading pay zero fees on maker orders.

Hyperliquid hasn't published a standalone HIP-4 outcome fee breakdown confirming things, but afaik, HIP-4 taker fee should be somewhat similar to perps (0.045% at base tier) or spot (0.07% at base tier). It might drop a bit depending on your volume/staking discount.

On the terminal, a disclaimer reads, “Perps, spot, and outcome volumes are counted together to determine your fee tier, and spot and outcome volumes count double toward your fee tier. Only fee-paying outcome trades contribute volume. Scaled fees above also scale volume contributions. Negative fees are rebates. Staking discounts do not apply to maker rebates.”

Sort of nuanced, so let’s go part by part:

"Perps, spot, and outcome volumes are counted together," which means all three market types feed into one unified 14-day rolling volume number that determines your fee tier. Not three separate tiers.

"Spot and outcome volumes count double." So, if you trade $1 million in outcome markets, it counts as $2 million toward your tier calculation, helping you reach lower rates faster. Basically, the same rule that already existed for spot now extends to outcomes.

"Only fee-paying outcome trades contribute volume.” As I highlighted earlier, opening and minting outcome trades are free and invisible to the tier system. Only closing and settling (where fees actually apply) move your volume number. You can't manipulate your tier by spamming free mints.

"Scaled fees above also scale volume contributions.” If you get a fee reduction (say, growth mode cuts fees 90%), your volume contribution is also cut proportionally. You can't get full-tier credit while paying reduced fees. The system is internally consistent.

"Negative fees are rebates.” When the maker rate goes negative in the fee formula, that's not an error. It means the protocol pays you. Pretty straightforward.

"Staking discounts do not apply to maker rebates.” If you're already getting paid a rebate as a maker, staking HYPE won't increase that rebate further. The staking discount only cuts the fees you're paying, doesn’t amplify the money coming back to you.

Outcome markets are somewhat on equal footing with spot and are deliberately weighted to help active traders rank up faster. So yeah, instead of having an outright number, it’s variable based on all the x-factors highlighted.

Airdrop speculation

Coming to tokens, Polymarket's CMO Matthew Modabber confirmed, "There will be a token, there will be an airdrop," on the Degenz Live podcast, but said the company is first focused on making a strong return to the US market before launching it.

Plus, even Shayne has indirectly given hints on Twitter.

This has, however, put farmers at the forefront. Many users are now using the platform to increase their chances of qualifying: betting in large volumes, exploring new markets, and reinvesting winnings rather than cashing out.

Some have taken it further by placing offsetting bets, voting both Yes and No on the same market to artificially boost their trading volume. Multiple reports point out that up to one-third of Polymarket's presidential election volume may have come from this kind of activity.

But Shayne has always jumped to defense and highlighted that Polymarket’s Terms of Use expressly prohibit market manipulation. Ultimately, it’s just a platform that wants to provide users with the fairest analysis possible.

$POLY-linked premarket perps are trading around $27, implying an FDV of roughly $27 billion. To put things into perspective, HYPE has an FDV of about $40 billion, according to data from CoinGecko.

Premarket prices aren’t 100% reliable either. A lot of these markets don’t have deep liquidity, so even a few trades can push valuations around hard. Again, just a rough idea, remember.

Kalshi, for now, is on the other side of the spectrum. It spent years navigating regulatory battles with the CFTC, secured designated contract market (DCM) status in 2020, and later scored a major legal win over the agency in its fight to list election contracts.

Since the platform is fully regulated in the US, the whole business is built around licenses, compliance, and traditional market structure rather than crypto-style token incentives. That probably takes away the “own a piece of the platform” angle.

People can trade event outcomes on Kalshi, but they don’t really benefit if the platform itself becomes massively successful. There’s no direct access to its upside. In TradFi, that usually comes through owning shares in the company, maybe through an IPO someday, but right now, Kalshi users are just traders, nothing more.

Meanwhile, the US is a major headache for Polymarket, sure, but even outside the US, things aren't exactly welcoming. The platform is geoblocked in places like Singapore, Thailand, and Taiwan, while Japan has partial restrictions. Hong Kong regulators have also started paying closer attention to prediction markets in general.

Hyperliquid doesn’t really have that same baggage. Its audience is much more crypto-native and heavily concentrated in Asia, where the trading culture is already huge.

In short, Hyperliquid already has a token tied closely to platform activity (long live HYPE), Polymarket is right behind on the same path, but Kalshi’s hands seem to be tied by legal/regulatory clauses that don’t outrightly allow for a token launch at all.

Who’s the better trader: Perp vs. prediction market users

This is the question HIP-4 is going to answer empirically over the next few months, and it'll be genuinely fascinating.

Polymarket's core users are kindaaa sortaaaa prediction market specialists, i.e., people who follow political developments obsessively, read economic data releases, and have strong calibration on macro events. They're not necessarily traders in the traditional sense. They have skin in the game.

Hyperliquid's user base is overwhelmingly perp traders. They think in terms of delta, leverage, and liquidation. They're fast, they're sophisticated in market plays, and they're extremely fee-sensitive.

The hypothesis that perp traders will dominate prediction markets rests on market efficiency: if you're good at reading order books and identifying mispriced bets, binary outcome contracts are just another instrument.

But again, no matter how much you try to sophistically answer this question, one thing’s for sure, “It’s no different than if you go to Vegas with your friends.”

To wrap it all up

I don’t think I’d wanna call this the prediction market war. I feel it’s about three fundamentally different bets on what the future of event-based trading could look like:

Kalshi is betting that regulated, US-compliant, brokerage-style prediction markets will win the mainstream. They're probably right for a certain segment: retail investors who want a fun alternative to index funds but without the crypto complexity/headaches.

Polymarket is betting that global reach, transparency, and crypto-native UX will dominate the information-trading layer of the internet. The POLY airdrop is the community retention play. They’re tryna keep power users farming while they sort out US regulatory re-entry.

Hyperliquid is betting that composability wins. If you can hold perps, spot, and prediction markets in one account, why would you ever open a separate Polymarket account? The HYPE flywheel is the cherry on top.

For now? Kalshi is your go-to for your regulated US macro bets. Polymarket for your crypto-native global markets and your airdrop farming. Hyperliquid for your perps-adjacent outcome bets, and if you want to hedge your BTC long with a binary contract without ever touching a separate app/tab.

And going forward, who knows, who’d end up integrating with whom?

At the end of the day, a win for one will ultimately be a win for all. Agree or disagree, it is what it is!

P.S. Since HIP-4 has just been rolled out, most data points are raw. Everyone’s been gathering numbers from multiple sources (some of which are updated, some of which are not). Most dashboards reviewed are in their experimental stage and seem to be using different computation methods, so take all figures/estimates mentioned in the article with a grain of salt and make sure you DYOR.

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)