Reading time: 12m 15s

At the beginning of 2025, just over 240,000 people held real-world assets onchain. Fast forward to this year, over 700,000 people hold real-world assets onchain - roughly 3x the amount a little over a year ago.

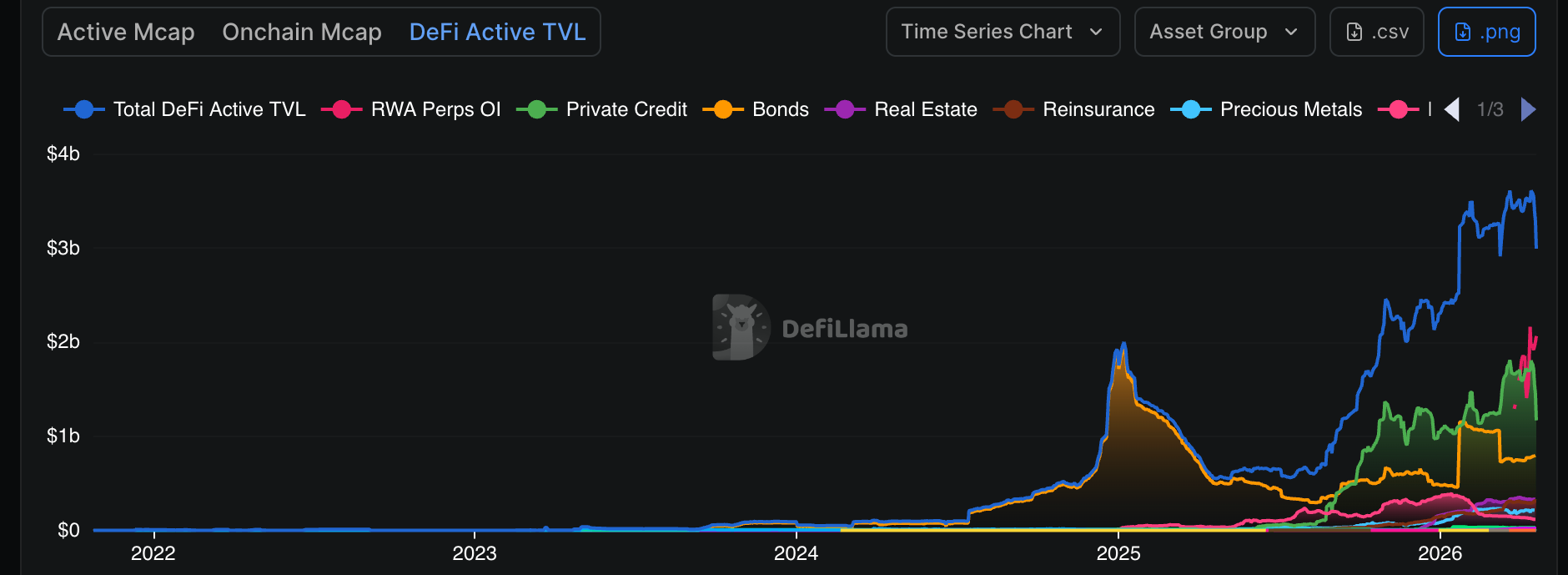

While DeFi gets absolutely defiled by North Korean mercenaries at the moment, the RWA space is silently growing into a monster, now responsible for ~ 5% of the value locked across DeFi, with ~$2.8 billion in active value deployed (look away, Lazarus).

In 2026 alone, we've had some absolutely head-smashing headlines with new entrants into the RWA scene - the NYSE announcing a tokenized securities platform in January, Nasdaq getting its own tokenization plan waved through by regulators, and tokenized treasuries punching through an all-time high of $13.79 billion.

The RWA market grew roughly 30% in Q1 2026 alone, pushing total onchain value past $29 billion.

For context, the entire tokenized RWA pie (excluding stablecoins) was $7.9 billion at the start of 2024, up 263% YoY.

The institutions that spent the last cycle pretending crypto was a scam have crept in, becoming the largest holders onchain.

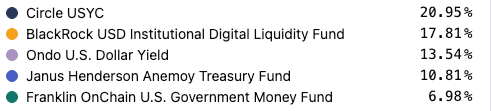

Circle's USYC sits at $2.9 billion. BlackRock's BUIDL at ~$2.8 billion. Ondo's USDY, Janus Henderson's Anemoy fund, and Franklin Templeton's BENJI - the top five tokenized treasury products alone account for ~70.09% of the entire sector.

Moreso, in the first two months of 2026, tokenized treasuries added $2.12 billion in new capital, outpacing stablecoin growth in absolute terms for the first time in history.

The wall between TradFi and DeFi isn't collapsing; it’s being taken apart, brick by brick, while everyone's distracted arguing about the Strait of Hormuz.

We took a look at the protocols driving the RWA sector towards the $100 billion mark. In this piece, we cover the seasoned players and the newcomers alike, and chalk out which ones we think can go the distance. Sit tight.

RWA protocol map

We look at leading protocols and emerging ones, along with the asset classes contributing to not just the total RWA market cap, but also to activity across DeFi, ranging from:

RWA perps open interest, tokenized treasuries, tokenized credit, bonds, reinsurance, precious metals, private equity, public equities, carbon credits, equity ETF, multi-asset RWAs (shoutout to DeFillama for the broad categorization).

Tokenized US treasuries

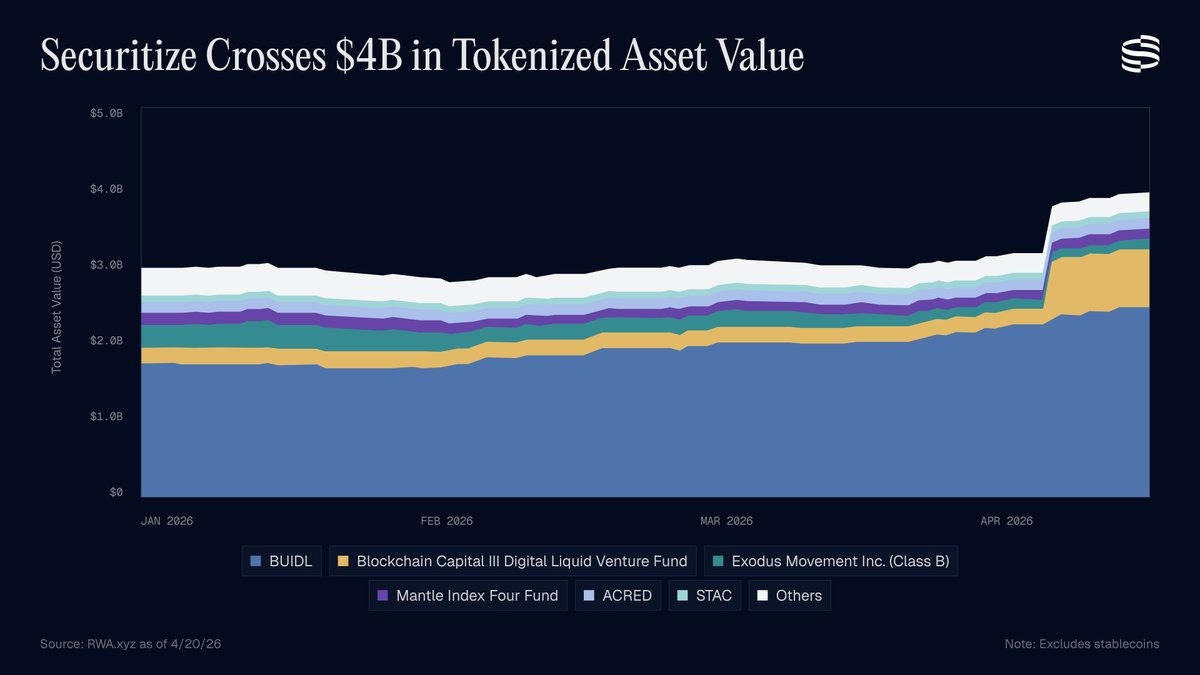

BUIDL (Securitize)

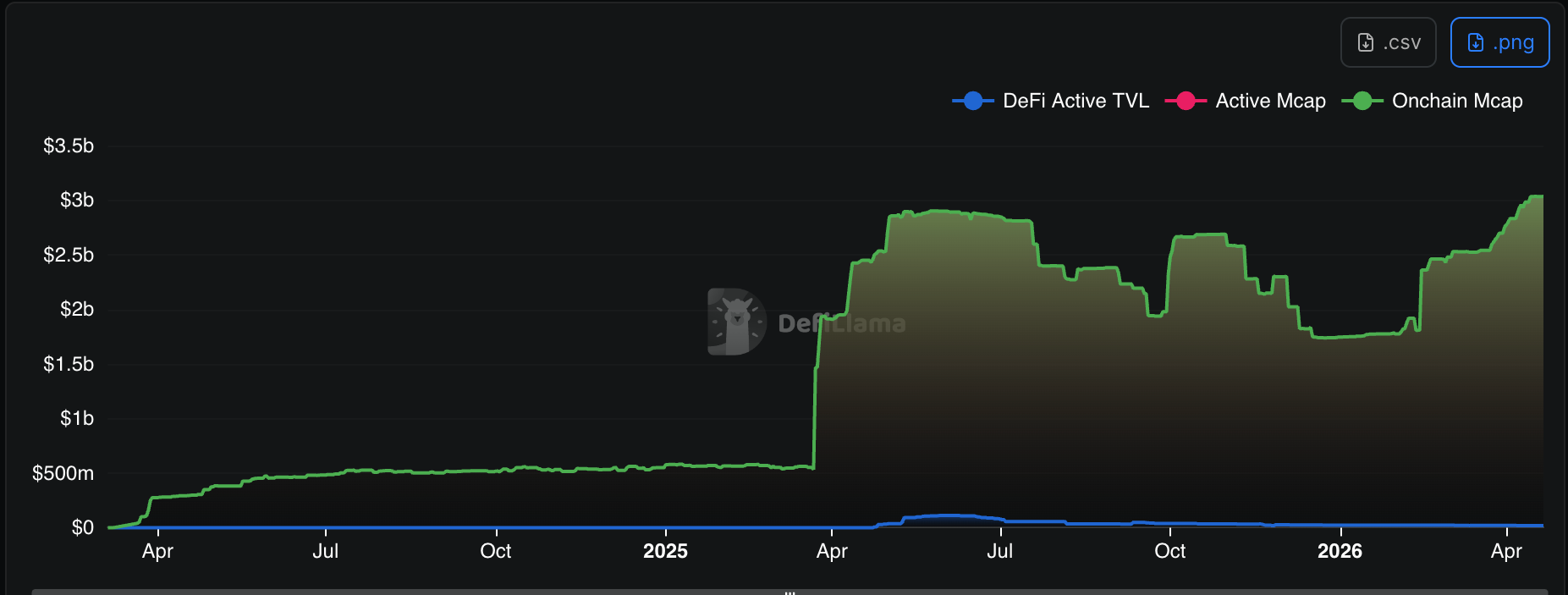

BUIDL is BlackRock's USD Institutional Digital Liquidity Fund, offered by Securitize and made available across Ethereum, Solana, Aptos, and over five other networks.

BUIDL has achieved a market cap of up to $3 billion, with $18.33 million in active DeFi volume.

BUIDL matters because it's the default institutional on-ramp between TradFi cash management and onchain composability.

It's already used as collateral across DeFi protocols, including Euler and Morpho, and when it was plugged into Uniswap in Q1 2026, it became the first regulated asset manager fund to live on a DEX.

Newer entrants in this niche include JPMorgan's Kinexys Digital Assets, UBS Tokenize, and VanEck's VBILL.

Tokenized credit

Data shows that the biggest RWA category by represented value is tokenized credit - private credit, CLOs, and asset-backed lending, with yields ranging from 5% to 12%.

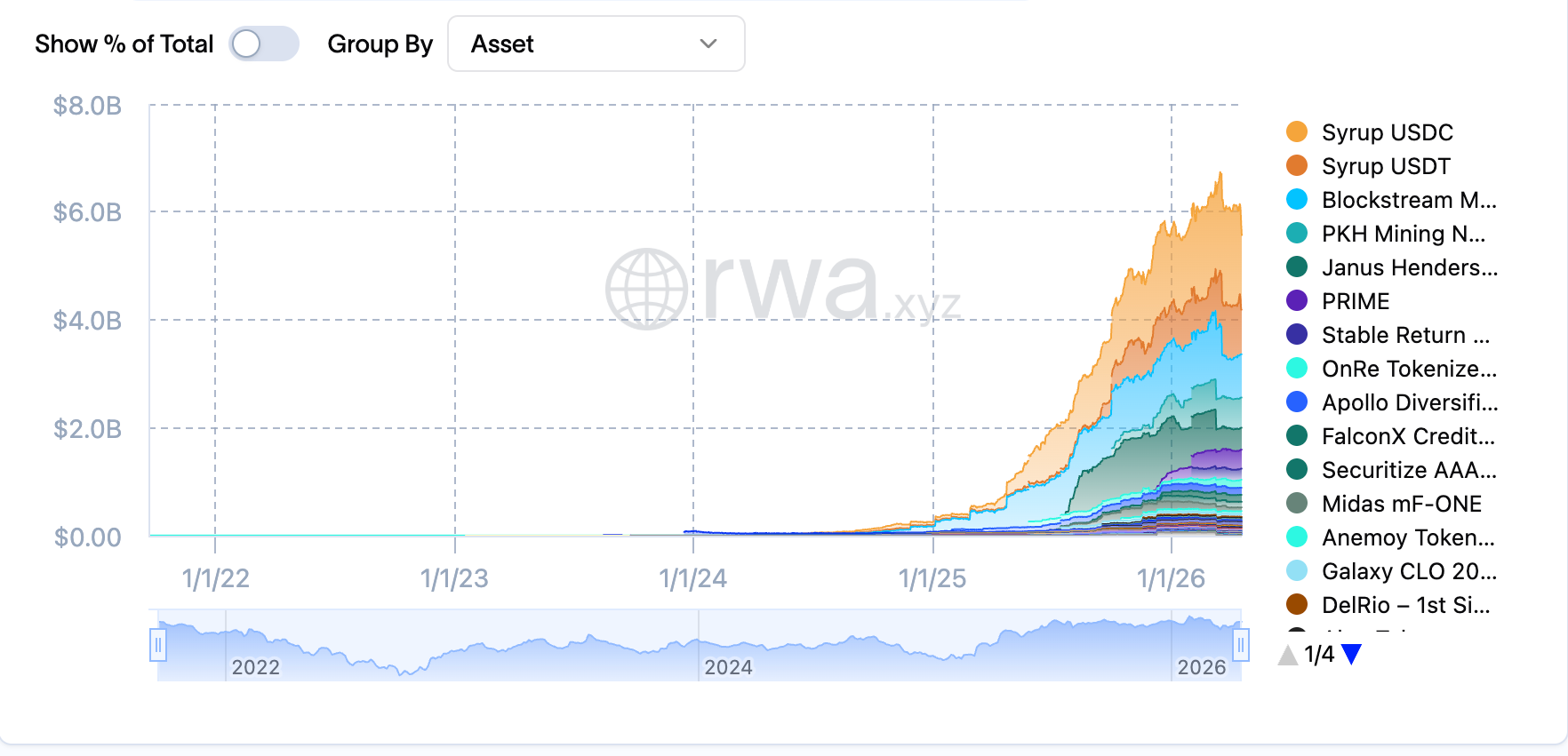

Maple Finance (SYRUP)

Maple’s syrupUSDC sits in this category, with ~$913 million in distributed value, while syrupUSDT is at $433 million. Combined, that is about $1.3 billion in onchain credit across Ethereum, Solana, Base, Arbitrum, Ink, and Mantle.

Despite Maple running into trouble in 2022 when under-collateralized crypto lending blew up, it rebuilt around institutional-grade borrower screening.

Today, the product is credit pools funded by stablecoin depositors and lent to vetted crypto-native firms and fintechs.

Maple rolled out its Cash Management Pools in late 2025, a more conservative product line that competes directly with tokenized treasuries.

Centrifuge JAAA CLO Fund

On the other hand, we have Centrifuge’s $408 million in the Janus Henderson Anemoy AAA CLO Fund, which yields up to 7.5%.

Centrifuge’s product is a fully onchain version of Janus Henderson's AAA-rated Collateralized Loan Obligation (CLO) fund, made available on Ethereum, Stellar, BNB, Base, Avalanche, and Arbitrum.

CLOs are a $1.2 trillion market offchain and JAAA is the first credible onchain version.

Centrifuge launched deJAAA on Base, bringing CLO exposure into DeFi composability for the first time.

A few new entrants in this space include Galaxy Digital's first tokenized CLO (GACLO-1) and Securitize's STAC. We believe that the thesis for this to continue growing is that every major credit fund will eventually need a tokenized share class.

RWA perpetuals

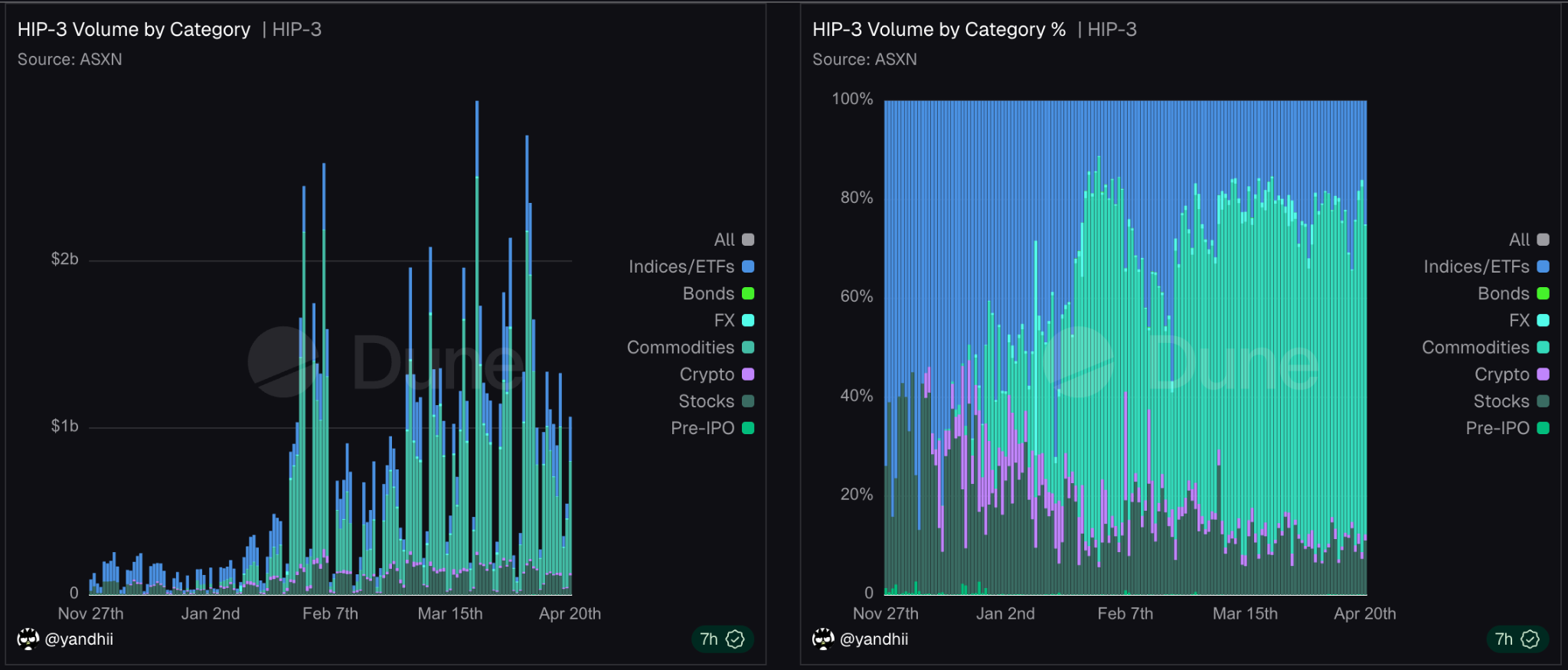

Onchain perps tied to stocks, commodities, FX, and indices are the fastest-growing RWA category, with Hyperliquid HIP-3 markets pushing huge volumes.

Hyperliquid HIP-3

HIP-3 markets have recorded over $192 billion in cumulative volume, with over 2.2 million unique traders, and $1.99 billion in total open interest (OI) as of 21 April.

But what’s interesting is that more than ~90% of this volume is tied to RWA markets. HIP-3 enables permissionless perp markets for over 100 assets, including stocks, commodities, indices, FX, and pre-IPO companies.

At the time of writing, BRENTOIL and CL (WTI crude) perp markets alone had cumulatively traded $813.89 million in 24 hours.

In fact, the US-Iran tensions saw oil perps on Hyperliquid hit a daily volume of $1.43 billion on April 13, attracting non-crypto traders who couldn't access closed traditional markets.

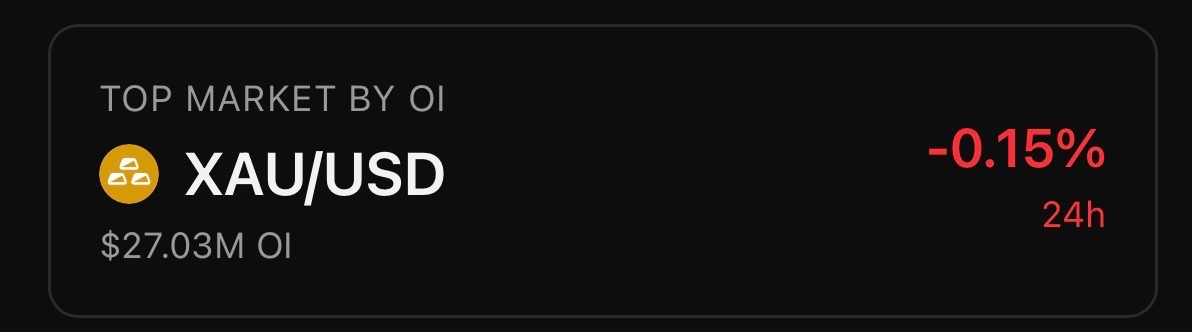

Ostium

Beyond Hyperliquid, Ostium is also doing great in this category - $50 billion in cumulative volume.

XAUT continues to maintain its position as the top market on Ostium by OI per Ostiscan as of April 21.

One thing to note, and what makes Ostium different from Hyperliquid, is that it is not trying to serve crypto traders who want RWA exposure.

Rather, Ostium is going after the $10 trillion monthly contracts-for-difference (CFD) broker market directly.

The top open contracts are gold, silver, EUR/USD, copper, and the Nasdaq 100, in that order.

Should Ostium convert even 1% of the CFD broker market onchain, it could, by itself, push the onchain RWA markets to $100 billion in OI.

Commodities (metals)

In late 2025, we observed CT take up more interest in metals - mainly gold. The metals trade has since become a staple, with copper and silver also recording significant volume in 2026.

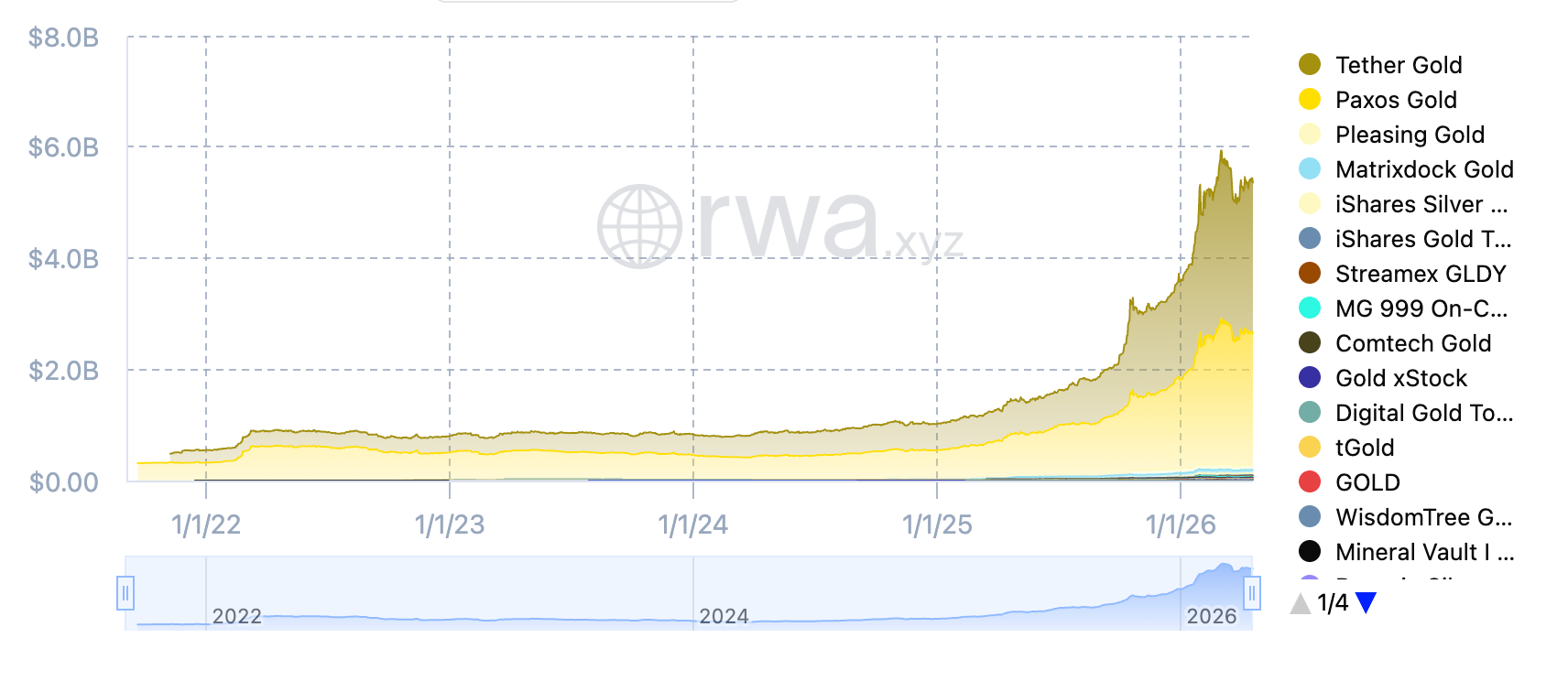

Tether Gold (XAUT)

Tether Gold leads in this spot category with $2.68 billion, up 5.66% in the last 30 days.

Each token represents 1 troy ounce of physical gold held in Swiss vaults and is available on Ethereum, Arbitrum, BNB, and Avalanche.

XAUT is the fourth-most-traded asset on Binance by volume as of April 2026, ahead of Solana, and has also contributed significantly to volume across HIP-3 markets.

Tether launched Scudo in early 2026, a fractional gold unit worth 1/1,000th of a troy ounce, aimed at smaller onchain transactions. This opens gold exposure to retail sizes that XAUT couldn't reach.

As the fear of a permanent underclass looms in the wake of AI, we expect the gold trade to persist and for gold to become the default non-USD collateral baked into stablecoin reserves and DeFi vaults.

Paxos Gold (PAXG)

It is important to note that the onchain commodities market cap is split between Tether and PAXG, with the latter at $2.24 billion, down 1.92% in 30 days.

PAXG is basically the same concept as XAUT, albeit with a cleaner regulatory position.

PAXG is issued by Paxos, a New York-regulated trust company. What this means in practice is that PAXG has access to US institutional channels, something XAUT doesn't.

Paxos has been positioning PAXG as a reserve asset for regulated stablecoins, not just a retail gold product.

Private equity

The private equity category encompasses the tokenization of illiquid private fund interests and private company shares.

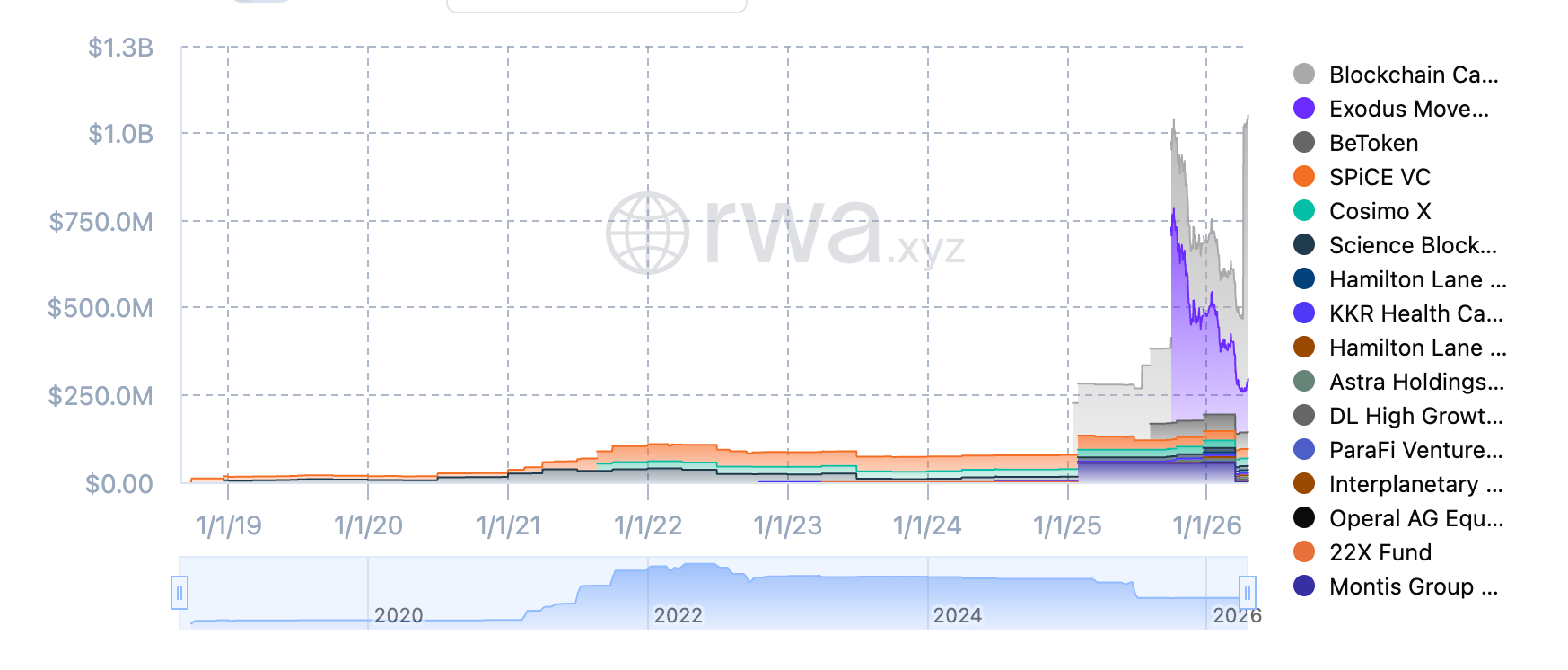

Blockchain Capital (BCAP)

BCAP leads in this category with ~$963 million across Ethereum and zkSync, up 361% in 30 days due to recent secondary market activity.

BCAP is Blockchain Capital's tokenized liquid venture fund - one of the longest-running crypto VC firms, giving tokenized exposure to its portfolio.

BCAP has started appearing as a treasury holding for DeFi funds that want crypto VC exposure without the LP dance.

We believe that every major PE fund will eventually need a tokenized share class to access onchain liquidity. Early movers like BCAP have the regulatory and infrastructure advantage.

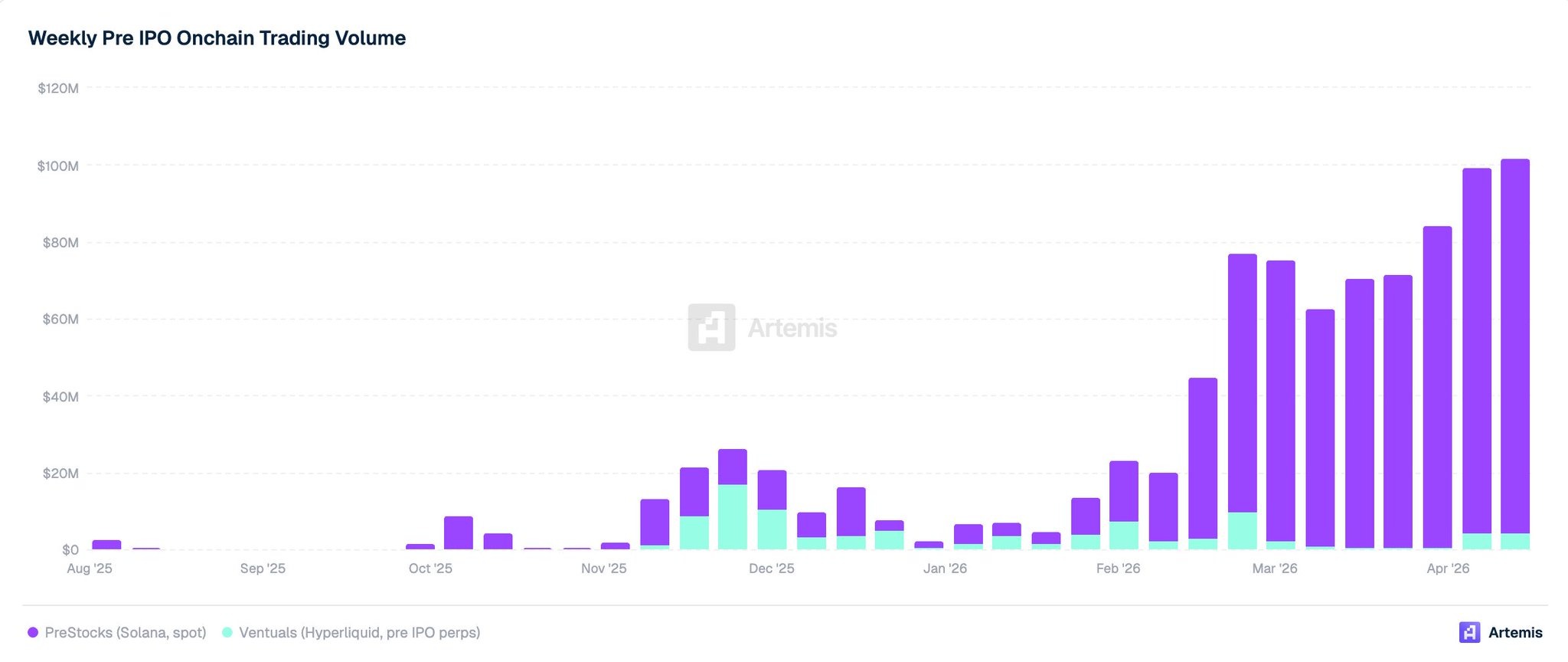

PreStocks (tokenized pre-IPO stocks)

PreStocks, as a product, provides economic exposure to private pre-IPO companies such as Anduril, Polymarket, SpaceX, OpenAI, and many more.

PreStock tokens are backed 1:1 by special-purpose vehicles that have access or exposure to the shares of these companies.

As of April, the platform has achieved over $750 million in lifetime volume across Solana integrations and has grown ~3,000% YTD in weekly DEX volume.

Public equities and ETFs

Ondo

A leading performer in this category is Ondo Global Markets, Ondo Finance’s tokenization platform, which brings publicly traded US securities onchain with institutional-grade rails.

Products like CRCLon (Circle equity), TSLAon, SPYon, QQQon at $33 million, plus a growing set of Treasury ETF wrappers (TLTon, TIPon, SGOVon, IEFon, SHYon) are all available to be traded onchain via Ondo.

Ondo is building a tokenized stock exchange for non-US investors who want 24/7 access to US equities (with custody via Alpaca Securities).

Ondo has been signing partnerships with Solana DEXs, BNB Chain issuers, and SEI to get these tokenized stocks into liquid AMM pools - trading and fractional share access are the two things retail investors globally have been asking for.

Ondo happens to be delivering both.

Reinsurance and Specialty Finance (RSF)

RSF involves tokenized reinsurance such as mining notes, litigation finance, and structured specialty credit.

To put it simply, reinsurance involves insurance companies being reinsured, in which the primary insurer transfers a portion of its risks to a reinsurer, paying a share of the original insurance premium to the reinsurer.

OnRe

The most obvious product pushing reinsurance onchain is OnRe, a Bermuda-licensed reinsurance platform that brings institutional reinsurance yield onchain.

OnRe has achieved $149 million in AUM with its latest ONyc product (a yield-bearing dollar asset) on Solana, offering up to 9.69% yield and over 5,574 holders.

ONyc yield is mainly generated by insurers offloading risks and paying contractual premiums that flow into OnRe’s pool as real yield.

Additionally, ONyc extrapolates additional yield from backed assets such as sUSDe, stacking collateral yield on top of the premiums generated from risk offloaders.

Reinsurance is one of the few TradFi categories that actually benefits from being onchain through cross-border settlement, programmatic claims, and auditable capital pools.

Global reinsurance is an $800 billion annual premium market - should even 10% come onchain in 2026, that is $80 billion - that’d be 20% shy of the $100 billion target for the RWA industry.

On our radar

Beyond the heavyweights, a deeper bench of protocols is building under the radar - launching new RWA products, full product lines, and infrastructure that compounds into the broader sector.

Here are a few under-the-radar protocols we have our eyes on:

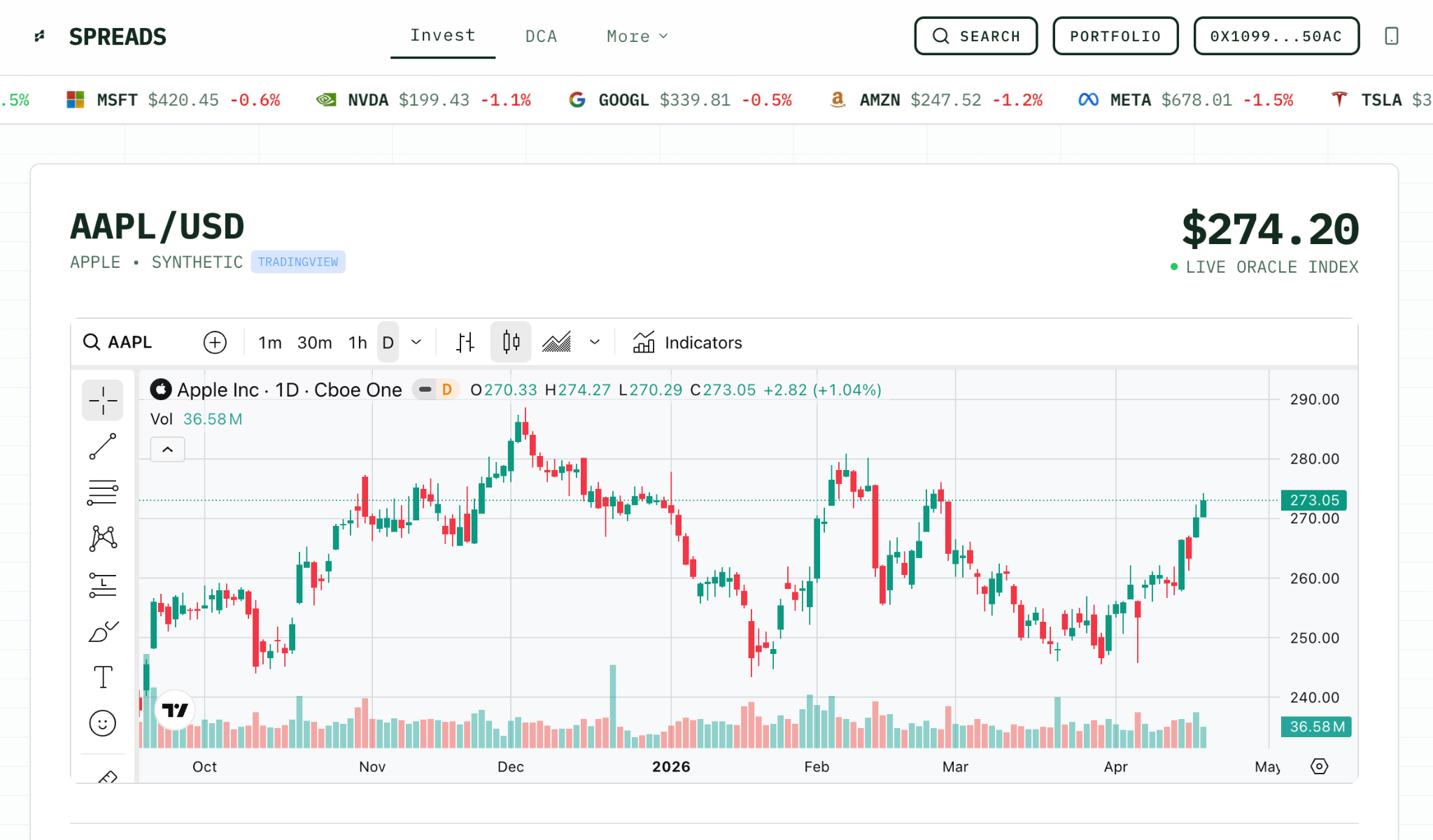

SpreadFi

Spreads is building the first onchain tokenized stock terminal, live on Ink and powered by xStocksFi.

Users can trade 50+ tokenized US stocks and indices (AAPLx, NVDAx, TSLAx, QQQ) 24-7 with USDC, without KYC.

On top of the terminal, Spreads runs copy-trading (follow politicians and fund managers), tokenized vaults, and STRC - a hackathon-winning primitive that turns any tokenized stock into programmable leverage, yield, and structured exposure.

Spreads is layering DeFi superpowers onto the $100 trillion equities market, which is exactly where retail attention is heading.

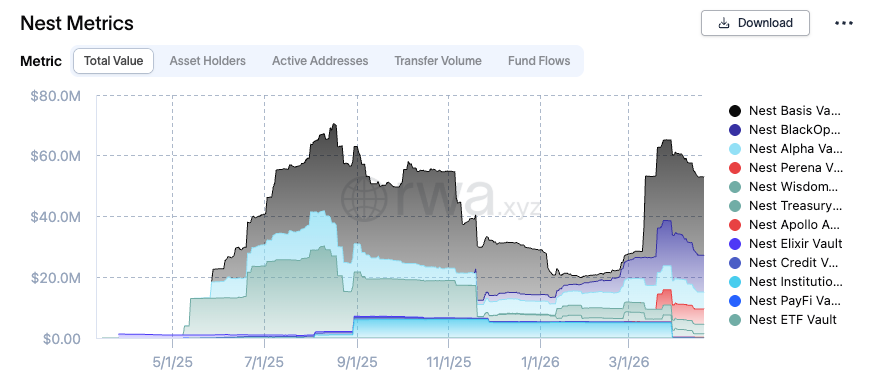

Nest (By Plume)

Another protocol on our radar is Plume’s Nest. Nest is doing what every stablecoin holder has been asking for - turning idle USDC into institutional-grade RWA yield with a single deposit.

Vaults are backed by tokenized real-world assets from partners like Superstate, with native deposits live across BNB and Solana (Perena), so users don't need to bridge.

Nest is built on Plume Network, composable across DeFi, and currently running PNP Season 1 - a points program tied to PLUME token allocations. The protocol has garnered over $50 million in distributed asset value and has over 10,000 monthly active addresses.

RWAX

Our eyes are also set on the purpose-built network chains, creating the perfect environment for RWAs to thrive.

One such project is RWAX, which is building a specialized blockchain environment (L2) that brings traditional real-world assets ranging from commodities to tokenized stocks, private credit, and other RWA assets onchain in a tokenized, tradable form.

Beyond direct tokenization, RWAX is going the user-friendly route with a Super App that enables portfolio tracking, yield, and direct asset swaps - basically a one-stop shop for everything tokenized hard asset onchain.

Pareto

Pareto (originally Idle Finance, now Pareto Credit) is building an important addition to onchain finance: institutional-grade private credit rails.

Instead of retail lending pools, Pareto runs customizable credit vaults, structured credit facilities, and a synthetic dollar (USP) backed by crypto deposits lent to vetted institutional borrowers.

Its FalconX Credit Vault on Morpho, co-managed with Gauntlet, already sits at $126 million.

Pareto is acting based on the certainty that DeFi needs credit expansion, and the way to get there is through composable, onchain infrastructure that asset managers and institutions can plug into without rebuilding the wheel.

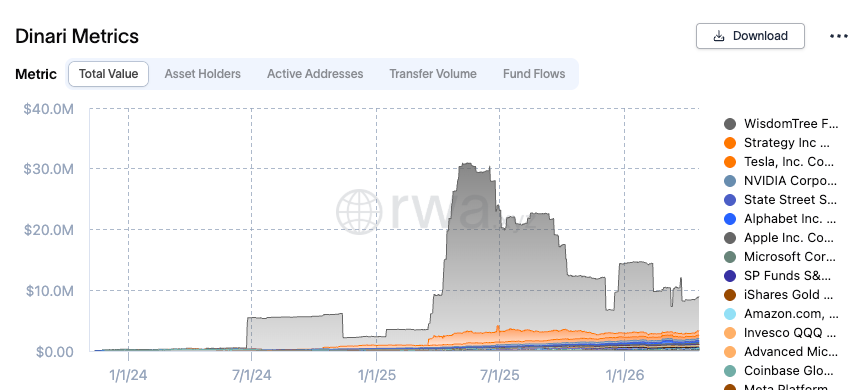

Dinari

Dinari turns real US stocks into programmable onchain tokens that fintechs and crypto platforms can plug into their apps.

Dinari’s dShares are 1:1 backed by actual shares held in regulated custody, dividends are paid automatically in stablecoins, and the asset library already includes over 230 stocks and ETFs.

The platform is SEC-registered as a transfer agent. In fact, it was the first tokenized equity platform to receive a broker-dealer license in the US, and recently launched the Dinari Financial Network - its own Avalanche-based L1 for 24/7 settlement of tokenized securities.

Dinari serves 25,000+ customers across 80+ countries, mostly through partner fintechs.

Vesta Equity

Bringing homes onchain or access to real estate has been a major quest in crypto for a while now.

Vesta adventures along this line as a real estate company using onchain systems to modernize home equity access.

Vesta’s MO allows homeowners to sell fractional shares of their property to willing purchasers.

The idea is for homeowners to have ready access to spendable liquidity without losing their property.

On the other hand, purchasers of these shares are simply buying at a premium the property's future appraised value.

Should the said property be sold on the market, the buyer will receive a share of the property's appreciated value.

Vesta operates the entire process (underwriting, tokenization, management, and perfect data room) through a native financial operating system called VEFOS.

Brickken

Our eyes are also set on Brickken - an infrastructure RWA protocol operating as an institutional-grade SaaS platform for the tokenization of a broad range of real-world assets.

Brickken simplifies the tokenization process by providing a toolkit that reduces paperwork for issuers.

Users or issuers can create and launch tokenized securities in minutes, handle investor onboarding with automated compliance, manage the end-to-end process from cap table to secondary trading, and unlock liquidity through fractional ownership, all while complying with regulatory requirements.

Obligate

On the bond scene, our radar is on Obligate - a Swiss-regulated protocol for onchain debt capital markets.

Obligate is an institutional-focused solution that allows issuers to create and launch digital debt instruments in hours.

The idea is to cut time and costs by up to 80% using smart contracts to replace agents.

Obligate works end-to-end across issuance and distribution, supporting multiple chains, while partnering with security providers such as Fireblocks to offer robust, institutional-grade infrastructure.

Inversion

Inversion is a crypto-native private equity firm with a pretty-based strategy: acquire profitable traditional businesses, fix outdated systems, and do some financial plumbing using blockchain tech, all while retaining the existing team.

Inversion’s goal is to drive real economic activity onchain, through struggling but revenue-generating businesses that have long existed and survived outside of the crypto world.

The operation begins through a very tight threshold for what comes through the door. Companies or businesses must meet the $1 million+ EBITDA benchmark, have recurring revenue, a strong team, and high finance-related costs to be considered for acquisition.

Concluding thoughts

The story in 2026 isn't whether RWAs are happening. It's how fast, and through which rails.

The largest institutions on the planet are building the pipes - BlackRock, Franklin Templeton, Circle, Apollo, Janus Henderson - alongside newer entrants swimming in a pool full of whales.

We strongly believe the industry is maturing at light speed, so much so that the $100 billion benchmark feels like a joke.

The bottom line is that structured products deserve better storytelling. Most of them today don't have the distribution or the narrative to reach retail - and that matters more than ever.

AI and automation are rewiring how people earn, and a whole generation is drifting toward passive income and investing as the default wealth-building path.

The protocols that explain themselves clearly are the ones that catch that wave. The ones that don't are the ones retail walks past, even when the product is good.

For retail, our advice is not to chase BUIDL-sized funds, but to patiently wait for protocols bringing low-cap tokenized stocks onchain, or look out for those offering pre-IPO stocks, like PreStocks.

We believe this is the category with the largest asymmetry (for spoiled crypto-native retail) left in the sector.

None of this is financial advice. Feel free to do further research before checking out any of the platforms mentioned above.

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)