GM!

2025 was a dramatic year. What began as DeFAI fever quickly gave way to vibe coding, ICMs, collectibles, robotics, neobanks, ICOs, and the privacy meta wave. There was something new to grasp every single week.

PA-wise, it was a rollercoaster of highs and lows. We hit peaks, plummeted to lows, and somehow managed to survive it all.

With the calendar flipping and a whole new year in front of us, we’re back with the fourth edition of the blocmates thesis.

Without any ado, let’s jump straight into the predictions.

General-purpose blockchain valuations will come back down to earth

Crypto is winning, tokens aren’t

The end goal was never unclear, in my opinion. Crypto moving closer to traditional finance, payments, engulfing all of fintech and beyond, has always been the end goal.

Even in an industry that would argue the sky is orange and the sea is green, we can all agree (from a philosophical and directional perspective) that was the mandate.

What people either neglected or chose not to acknowledge is the end state of that success.

If crypto actually works, it becomes invisible.

And when that happens, the idea that loosely tethered, adjacent tokens should have some form of pseudo-equity, or second-hand upside, or exposure to the success of the underlying tech, is completely out of touch with reality.

From an investor-protection perspective, it’s totally mismatched.

So, where does that leave us?

I think crypto is winning. Tokens aren’t necessarily winning. And that plays out in one of two ways:

Path one: Companies, not “projects”

Real companies. Revenue-generating. Cash-flowing businesses. You know, like the ones in the real world?

This is already happening. There’s a whole stream of infrastructure providers right now that are among the most profitable companies on earth. Tether, Privy, Phantom, to name a few.

They don’t need tokens. Why would they? So some NEET can sit in their Discord and tell them that they should be doing more marketing.

Do they need tokens under the guise of decentralization? Not really. That ideal is long gone. It doesn’t make sense economically, structurally, or strategically, other than to fund additional runway if you didn’t have any in the first place.

I’ve always said:

“The best projects don’t need a token. The best tokens don’t need a project.”

That line becomes increasingly true as crypto moves closer to the real world.

Path two: Tokens as actual ownership

The other avenue is that tokens do exist, but they’re honest about what they are. They represent equity. They come with real investor protections. They behave like traditional stocks. (See 563’s piece above on MetaDAO and tokenized equity).

The difference is composability:

- They run on crypto rails.

- They’re programmable.

- They’re interoperable by default.

That’s the trade. Not decentralization theater. No pretending.

The reckoning ahead

What this ultimately turns into (and I’ll get into this later when talking about M&A) is a severe grounding in reality.

A lot of teams are going to have to confront the fact that they’re pre-product, pre-revenue, and sitting on multi-billion dollar valuations where the raise was the product.

That happens in other industries too, but crypto corrupted it at scale.

- The prodigy-founder narrative.

- The loosely defined TAM.

- The slow-burn solution to a problem the industry mostly invented for itself.

Nobody outside the industry really gives a shit. But it gives billion-dollar funds a way to justify deploying capital they’re structurally forced to deploy. And that self-referential loop is how we ended up here.

It’s pretty clear at this point that there’s been a changing of the guard when it comes to where blockspace demand actually lives. Right now, that demand lives on Solana.

Anyone trying to argue that it meaningfully lives on Ethereum, or that Ethereum securing around $80 billion of TVL somehow justifies current valuations, is missing the point. I’d argue Ethereum is overvalued by 2–3x, but I’m not going to go down that road here.

The more important issue is that we’ve ended up with people trying to value blockchains as companies. That framing is wrong.

Blockchains aren’t companies

I don’t see blockchains as companies. I see them as mini digital countries. They should be valued based on productive users, applications, and businesses built on top of them. That’s where the value is derived.

Like any analogy, this breaks down if you push it too far, but as a framework, it’s far more honest than pretending blockchains are SaaS businesses with predictable revenue multiples.

We don’t need this many general-purpose chains

That framing still doesn’t imply we need dozens of general-purpose blockchains. We don’t.

We haven’t even proven there’s demand for even three of them. Let’s be brutally honest with ourselves as an industry: Solana works. Base works. Hopefully, Monad and MegaETH will work.

One-size-fits-all, extremely high throughput, and low latency. That is great, but I am not sure it is all needed, at least not yet.

The problem with the “not yet” statement is that by the time the industry is ready for it, the second movers will swoop in with the most current iteration of infra and clean up, and it's about to happen.

The L2 shakeout was inevitable

In the 2025 thesis, there was a whole section on general-purpose L2s effectively dying. That was directionally correct.

The only real exception I called out was Base, plus more specialized L2s, which we’re now starting to see with things like MegaETH coming online.

Monad is still too early to judge. What they’ve built technically looks very good, but the open question is legacy overhang.

They raised a huge amount of money, which has consequences: cap table pressure, token dilution, and the wrong people holding excessive supply. We’ve seen this play out repeatedly over the past two years.

Teams end up fighting an unwinnable battle trying to get tokens to market and manufacture speculation, hoping network activity follows as a byproduct.

That order of operations is backwards, and it doesn’t work anymore. Even if the underlying infrastructure is best-in-class, if the corresponding token doesn’t perform well, the market ignores any fundamental brilliance associated with it.

Second-mover advantage is here with Tempo

Where things get more interesting is with Tempo.

Tempo feels like a genuine experiment: raise an extremely large amount of capital, hire top-tier developers who’ve worked on legacy systems like Ethereum, apply the weight of a serious financial company like Stripe, and secure actual grown-up partnerships.

If I were Solana or any would-be competitor, that’s the one I’d be looking over my shoulder at.

Incubated by Stripe and Paradigm, headed by Matt Huang and the technicals led by ex-Ethereum Foundation researcher Dankrad, it would be foolish not to pay attention to Tempo in 2026.

The Stripe acquisitions of Bridge and Privy now begin to make a ton of sense.

I will caveat this by saying I don’t think this looks like a chain rollout of times gone by. I am not sure what happens with a token (if any at all). There is no native gas token and a permissioned validator set overseeing the network through BFT.

Aspects to pay attention to on Tempo:

- TIP-20: Tempo’s own token standard. Kinda looks like an adaptation of ERC20 but optimized for payments, including:

- Transfer memos (32-byte notes on transfers)

- Role-based access control (issuers can grant/limit minting, pausing, etc.)

- Transfer policy hooks (comply with whitelists/blacklists)

- Reward distribution logic

- Transfer memos (32-byte notes on transfers)

- TIP-403 provides a centralized registry of access control policies (e.g., whitelist or blacklist) that TIP-20 tokens can reference to standardize and enforce transfer restrictions across multiple tokens.

Get Netscaped, nerds

The industry is getting Netscaped. You have to be severely mentally handicapped to think the first meaningful mover in any vertical is the one to always win.

Being first is not a moat. And, yes, weirdly, there is a lot of bag bias because of the underlying assets, making a lot of people rich from back in the late 2010s.

Now, the big boys are here. They watched what worked and what didn’t. They let crypto eat its own narratives for a decade.

Now, regulatory clarity is actually happening - legitimacy is here, and second-mover advantage matters more than ideological purity. This is the phase we’re in.

Distribution > innovation

Execution > timing

The old playbook is dead

Trying to win by saying it’s slightly faster, has mempool-level privacy, or has rotating sequencers was last cycle’s playbook. Everyone’s seen it now; it doesn’t fly anymore.

It’s just self-referentialism again, something this industry is completely saturated with. Don’t expect to see any of this in 2026, and if you do, it is probably an easy short.

What actually matters now?

If you want to make serious headway, go and do something that materially improves day-to-day business operations, actually works for consumers, and delivers value without needing a manifesto to explain it.

That’s where general-purpose blockchain valuations come back down to earth.

Inversion could be an interesting take on this whole idea and will be one I am paying attention to throughout 2026. Trying to bring real revenue-generating business to crypto-rails and help with distribution, whilst making them more efficient, seems like a great idea.

If nothing else, it will prove out what benefits a chain can bring to a legacy business, if any at all.

It is also impossible to ignore Robinhood and its own chain, which is expected to go live sometime in 2026.

Reality check, bucko, the big kids are here, and they’re ready to kick sand in your eyes and give you a wedgie. The days of pre-product $1 billion+ raises are dead unless you are already proven.

This leads me to Commonware, which I imagine will be one of the winners of 2026.

We had the pleasure of hosting Patrick on the podcast a year or so ago when he was first building Commonware. Since then, it appears to be the framework of choice for the rollout of L1s into 2026 and beyond.

A set of completely modular primitives giving builders extreme levels of granular detail when building their purpose-built stack.

This is why Tempo, GTE, and others have chosen Commonware as their infrastructure provider to enable particular use cases which would take a shit ton of capital and an ungodly amount of time to build from scratch (Monad).

If I am to play out where we are headed with L1s, it is probably a full circle moment here. Hyperliquid has shown the playbook of product-first on a hyper-specific network, which allows teams to control every aspect of a stack.

We will probably see Polymarket launch its own L1 on the back of its token (POLY), dropping at some point in 2026.

When an app reaches product market fit, it will naturally want to control its own vertical and not be dependent on a general-purpose chain it has no control over.

The problem with this is that teams will leap from the PMF part and jump straight to launching an app-specific L1 and then complain why they cannot attract users residing on Solana, Base, or MegaETH due to friction.

All that to say, L1 premium is long, long, long gone, and valuations across the board will compress, and a huge power law distribution will be in the hands of the likes of Hyperliquid (HyperCore), Solana, Tempo, and maybe Polymarket once it launches.

TLDR: Hyperspecific chains built with purpose will thrive. With general-purpose, the winners are already here.

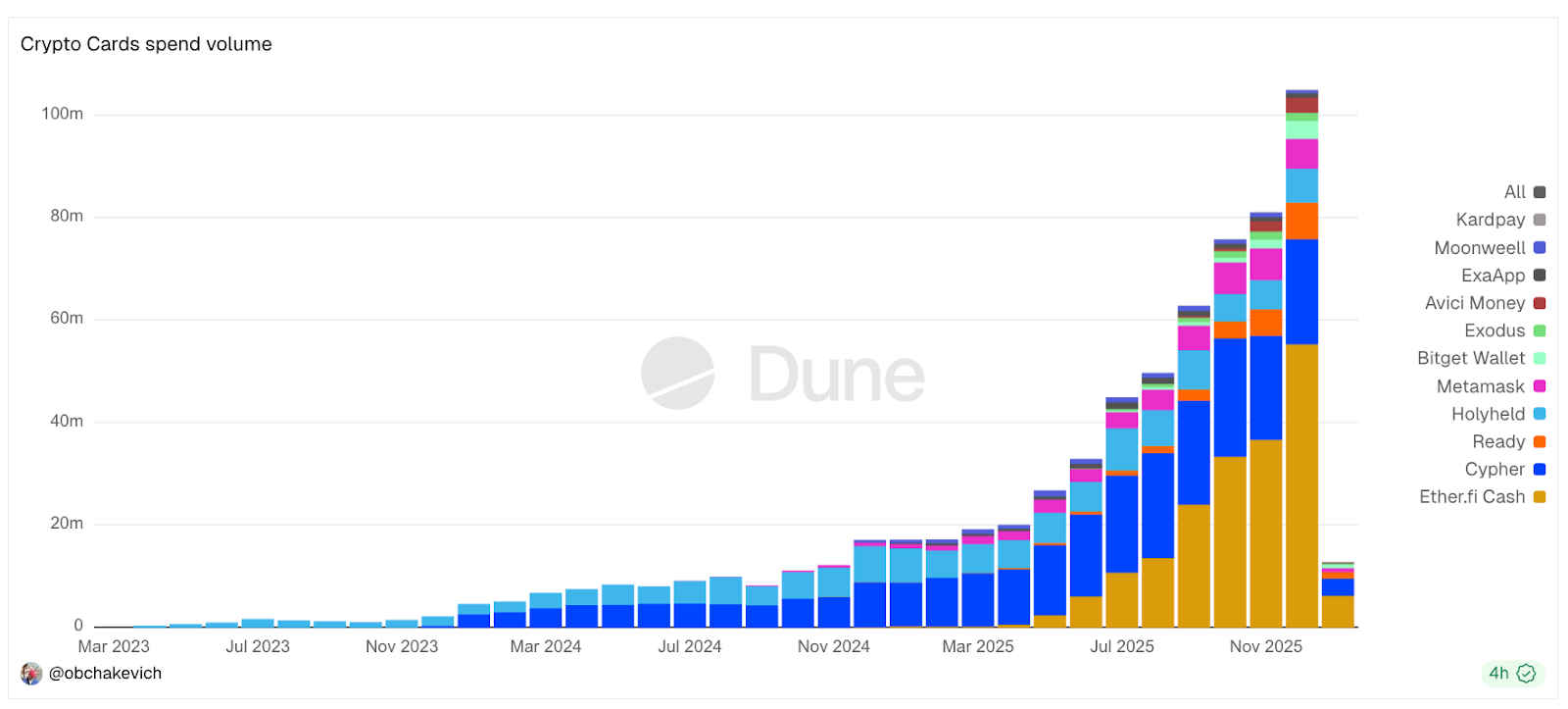

Crypto cards: The next vertical ripe for true PMF

When businesses that run on crypto rails achieve product-market fit, they become the most efficient businesses on earth.

What we have here is asset issuance (Tether), perp exchange (Hyperliquid), and a hyper-speculation memecoin casino (Pumpdotfun).

I think the next vertical ripe for true PMF on crypto rails is crypto cards.

We have had centralized crypto cards for a while now, and all major exchanges have tended to offer them.

More recently, in the past few years, we have seen self-custodial cards become a more and more popular form of off-ramping and spending.

On the backdrop of regulatory clarity, growing CEX suspicions, interesting yield opportunities for idle balances, and easier OpSec, like MPC becoming more widely available, self-custodial cards are on the rise.

There has been nearly 100x growth in month-over-month spending in the past two years, and the numbers are still tiny in comparison to their centralized counterparts.

The business model varies depending on the underlying product that owns the card. Some benefit from large TVL deposits and earn fees on DeFi integrations, i.e., money markets, staking yield, etc. Others take fees on FX conversions and swap fees.

There is some pushback, though. A lot of cashback yield, which is used as an incentive, is usually in the form of a token, which inevitably results in massive sell pressure correlated to monthly spending.

EtherFi cashback gives you Scroll tokens, Ready gives you Starknet tokens etc.

Phantom is an obvious one to watch when it comes to crypto cards, as they were the onboarding gateway of choice for the class of 2024/25, so naturally, their distribution is unmatched.

Throw their purpose-built stablecoin CASH into the mix (issued by Bridge and accepted across Stripe’s network), and you have a huge player in the card space.

I think Phantom starts to look like the closest thing we have in the industry to a Super App.

In-app trading, card purchases, white-labelled apps, perpetuals (crypto and equities), their own stablecoin, I can almost guarantee chat will happen too. That is on par with Revolut ($75 billion valuation) and is getting closer and closer to WeChat, Grab, or other Asian super-apps that dominate the Eastern world.

I also think we see hyper-gamblification enter the card space. Flip-to-not-pay, card roulette, and other degenerate ways to give you the option to gamble and not pay the full amount.

Feels like a natural progression and culmination of where finance, crypto and the demographic shift is at right now.

The winners will be those who optimise for the lifestyle aspect, taste, culture, and exclusivity tiers. Trying to win out when the space is saturated with only hyper-inflationary tokens, as the customer acquisition strategy is a waste of time, capital, and will attract the wrong user groups.

My advice would be to find a 10/10 product girl or guy who knows how to tap into culturally relevant circles, make the card something of a status symbol, kinda an IYKYK, and max out the perks.

It should be a lifestyle accessory that provokes questions.

Mergers and acquisitions will continue aggressively

This bundling of products is something I expect to see more of in 2026. We saw a huge uptick of crypto mergers and acquisitions in 2025, and I think it was due to a few things:

- Talent shortages lead to talent acquisition for larger projects.

- Lack of PMF in single-product companies, which can be rolled up into more effective, higher multiples businesses.

- Conversion of DeFi product suites over single products.

- Early DeFi vintages (2020/21) are running out of runway and/or tokens to fund operations.

- Some truly innovative and technically great infrastructure products.

Again, I think we will see more of this continue in 2026 as the shift away from speculation and drive to sustainable revenue-generating suites of products that all complement one another will probably be cheaper to acquire than to build.

Distressed teams, assets, and IP will become more readily available for acquisition, which we have already begun to see.

What this also does is squash valuations in line with what the real world is willing to pay for them. This aligns everything else with reality.

Again, valuation compression across the board, and this raises another question: what happens to the token during an acquisition?

Well, if the recent Circle acquisition of Axelar Labs is anything to go by, the team and tech come, the token and Discord incels stay and hold the bag.

This just reaffirms our points on token holder rights and ownership. The industry must define this year, and as we have mentioned, teams like MetaDAO with STAMP, StreetFDN, and SOAR are likely to have an interesting year.

We’re not the biggest dicks at the circlejerk anymore

The Treasury Secretary is calling for trillions in stablecoins.

The Fed is publishing government data onchain through oracles.

Both the NASDAQ and the President’s family are backing prediction markets. This is no longer a niche movement.

The big boys are here, and you thought they’d pay you for being “early” instead of keeping it all for themselves? Think again.

There will be no participation trophies, and billion-dollar IPOs (not ICOs) will be the base case for apps with PMF going forward.

But that doesn’t mean there won’t be more juice to squeeze for us retail button-mashers.

After all, this is the greatest casino in the world, and just because it’s under new management doesn’t mean it won’t reopen when enough gamblers are pounding on the door.

In our opinion, the comparison to the dot-com bubble is overdone, but it gives us some clues on how we can position. Stop holding out hope for the Pets.coms and the Ciscos, start looking for the Amazons and Facebooks.

The tech has proven itself, but the application of that tech still needs a clear vision and a world-class team to build a killer product.

Odds are there are still Instagrams and TikToks of this future still waiting to be built - and we intend to sniff them out.

The best crypto companies will not be “crypto” companies

Long gone are the days of Sandbox and Axie Infinity running to multi-billion dollar valuations on the coattails of the crypto hype machine.

You don’t get credit for just showing up anymore - crypto is just a tool, an incredible tool, don’t get us wrong, but you no longer get to sprinkle “crypto” fairy dust on a project and enjoy a 10-1000x jump in valuation.

You don’t hear any startups calling themselves “internet companies” in 2025. And just as the internet became a tool in the toolbelt, so will crypto/blockchain.

It’s plain to see that “crypto-native” projects have vastly underperformed traditional tech companies that simply leverage the tech we know and love. We expect that trend to not only continue, but to accelerate.

The winners of 2026 will not be the solo anon dev that ships a slightly cleaner, privacy-focused perp DEX.

They will be fintechs like Robinhood that tokenize equities and use blockchains to host 24/7 trading, payments specialists like Stripe that can settle instantly using stablecoins, political market intelligence consultants that leverage Polymarket data to win elections, you get the idea.

Blockchain is changing the world. But we need to break out of the echo-chamber we’ve self-erected. Open the aperture.

This is what “adoption” actually looks like, friends. Real businesses that have to deal with shit like quarterly shareholder calls and board meetings are using the technology, and now it isn’t just because being a “blockchain” company is good for PR (it’s not), but because it works and using it puts them ahead of their competition.

And not to fret, these companies generally have stock we can buy - so you aren’t getting rid of us that easily.

Tokens need a dramatic reconfiguration

2026 will be the start of a token renaissance.

And it’s about time, because tokens today absolutely blow. They're either bundled, sniped, and caballed, or their worthless governance (meme-) coins, or they’re co-opted by so many insiders and 5 rounds of VC funding to the point where 200% of their value discovery occurs before it even hits the open market.

The acquisition of Padre by Pump, Axelar by Circle, and the outrage at the Aave DAO/Labs misalignment have sparked an uprising from frustrated tokenholders, asking what it is they really “own” when they hold a project’s token. And we believe this trend will only accelerate in 2026.

We believe that real value can be created onchain and succeed not despite crypto rails, but because of them.

But it has to start from first principles. How do you align the best interests of the tokenholders with those of the project the token (supposedly) represents? We see a couple of paths:

1. Regulatory protection

2. Ownership coins

Regulatory protection through the CLARITY Act - making ICOs great again

The CLARITY Act has passed through the US House of Representatives and is expected to be signed into law in 2026.

In a very broad sense, it gives clear guidelines for projects to raise funding through token sales and designates which governing body is responsible for regulating these tokens during the sale (SEC) and when the token is resold and/or goes on to trade on exchanges (CFTC).

It’s hard to overstate how big a deal this is. If we were to go back even a year or two, token fundraising in the US has been a major pain in the ass for the vast majority of folks.

By passing CLARITY, the US is stating that it wants to be a hub for innovation, and that it thinks crypto fundraising opens the door to equal-opportunity investing for individuals as well as institutions.

It's not hard to see why Coinbase has been pushing so hard for this regulation to go through, in the right way, especially after their $400 million acquisition of Echo from Cobie.

My prediction is that Coinbase leads the industry in these launches, leveraging their political/industry connections to become a quasi-combination of YCombinator and CoinList for crypto or crypto-friendly startups looking to raise.

Look out for high-profile names that start off fully crypto-native, move into crypto-adjacent, and then teeter towards “just cool tech that doesn’t mind being associated with Coinbase.”

I don’t know about you, but I’d much rather back a project raising on Coinbase than KYC through some semi-legitimate ICO platform from overseas that’s asking for my firstborn’s middle name.

The de-stigmatization of crypto is well underway.

Ownership coins - parallel alignment

If CLARITY is the external approach to the token facelift, the rise of ownership coins is our crypto-native bet.

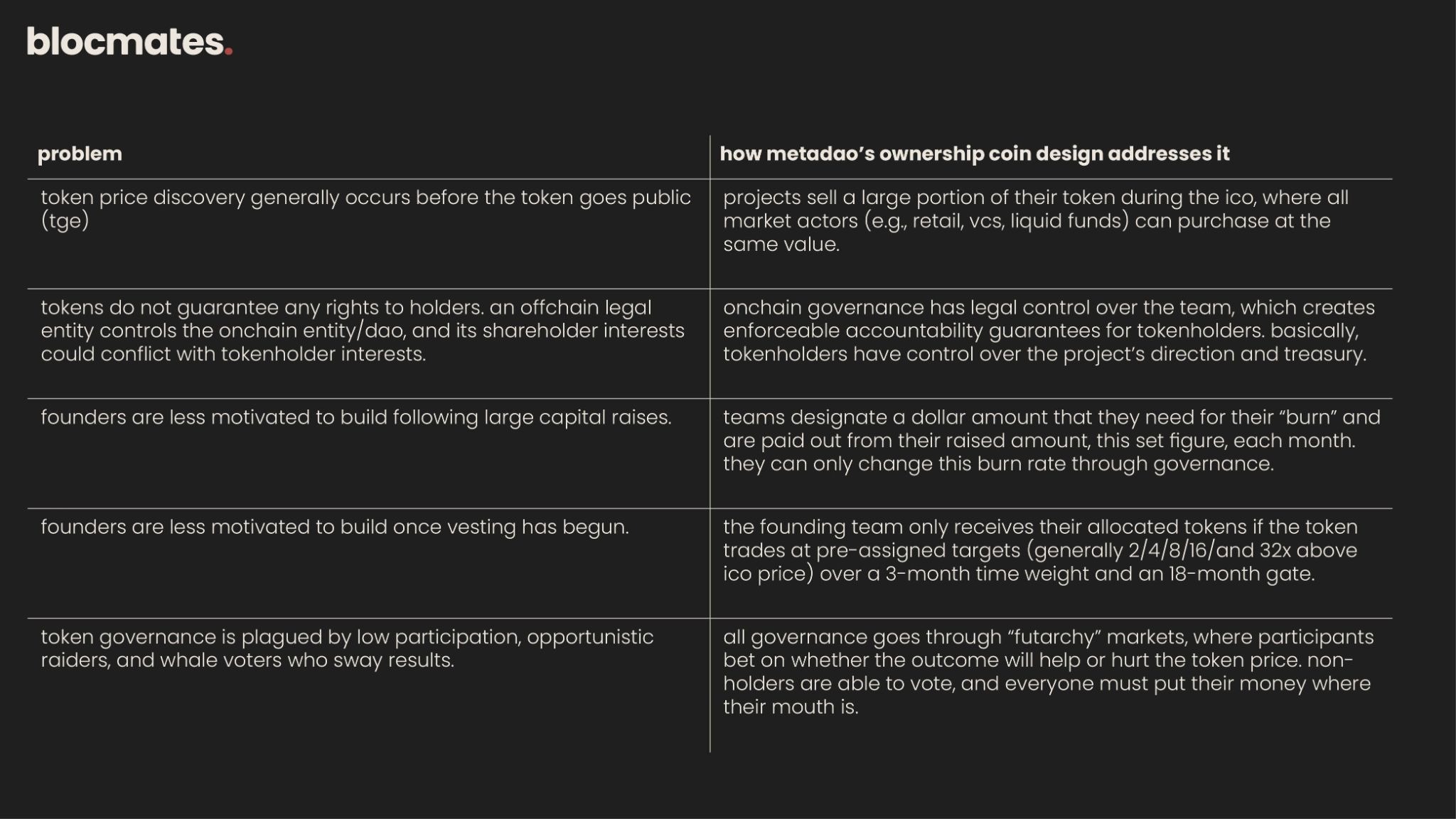

Popularized by MetaDAO, the characteristics of “ownership coins” attempt to besiege the principal-agent problem from all fronts.

(For those unfamiliar with the phrase, token design often pits the best interests of the investors [principal] against those of the team [agent]. MetaDAO fixes this.)

Transparency and alignment are the keys here. This is programmable money we are talking about, after all. Kinda wild that we’re only just now programming it so that everyone involved is rowing in the same direction.

Colosseum is adding fuel to the fire with STAMP, their solution for the industry to move past SAFT (and/or SAFE + token warrant) and into an era where early projects can still pick and choose their first investors and raise publicly via ICO with all of the token protection that MetaDAO has enabled.

Another project we are keeping a close eye on is SOAR, whose DRP standard leans on debt-based claims (different in practice from how ownership coins integrate onchain governance with legal entity ownership).

DRP tokens represent a senior debt obligation to the company, meaning that holders would be first in line if there were ever a liquidity issue, such as bankruptcy/dissolution.

This model actually may be easier for existing projects to adopt since they don’t have to worry about ongoing governance from tokenholders.

This trend towards more-aligned tokens is far from its peak, if we had to guess. And if you squint a bit, it’s the same frustration with “VC coins” that brought about the memecoin frenzy of 2024.

In that case, the industry threw up its hands and admitted that nothing had real value, but we think the pendulum swung too far.

2026 will center the swinging pendulum. Investor protections, tokens that march projects towards greatness, and maybe, just maybe, a unified cry for higher standards.

Tokenomics will move away from static

Crypto bros have always had a hard-on for fixed supply dynamics when it comes to tokenomics. After all, we’ve been beaten over the head with “there’s only 21 million coins, bro” since day 1, and when any project dares to push back, it can be an uphill battle. But the Overton window is beginning to shift.

Jon Charbonneau and Hasu’s proposal for HYPE was met with intense polarization, with one side (mostly .hl’s) cursing them out for suggesting that the Hyperliquid team’s original vision could be improved by mere mortals and the other side praising it for clearing up the question of how to spend a huge chunk of idle token supply.

Indeed, projects (and markets) change immensely from the time of whitepaper publication through TGE and as the protocol matures.

Why soft-lock a great idea with sub-optimal tokenomics just because “we gotta be like Bitcoin”? We shouldn’t be painting ourselves into corners of our own making.

And yeah, this is kinda still a pitch for ownership tokens, which can be minted in order to grow supply, but only if a futarchic governance vote is able to be passed (example). After all, companies can issue stock in order to fund exciting new operations - we have the tools to go toe-to-toe with the big boys now, why handicap ourselves?

Additional angles, including dynamic unlocks, will also become less and less hated. Early examples like Hivemapper opened the door to KPI-based unlocks for parties expecting emissions, but only recently have big players like MegaETH enshrined team unlocks to hitting protocol goals that align the builders with tokenholders.

Expect this to become the standard going forward, where investors expect alignment over arbitrariness.

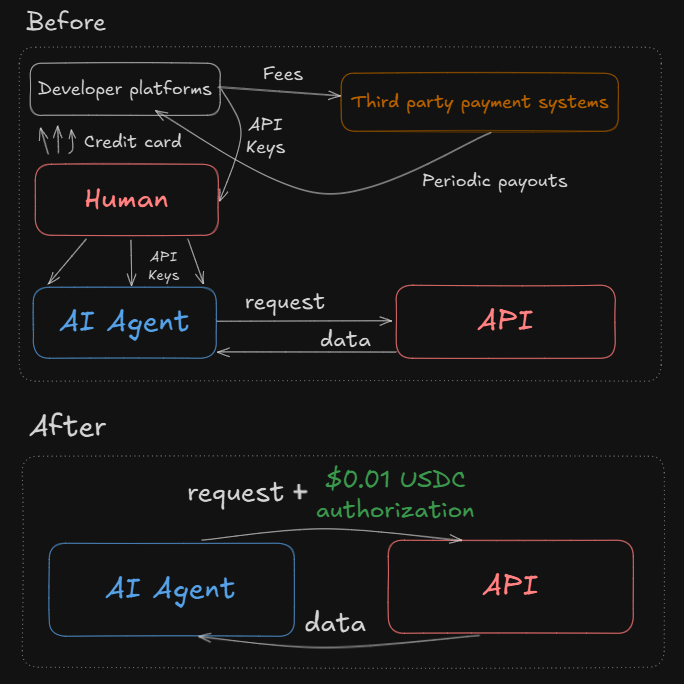

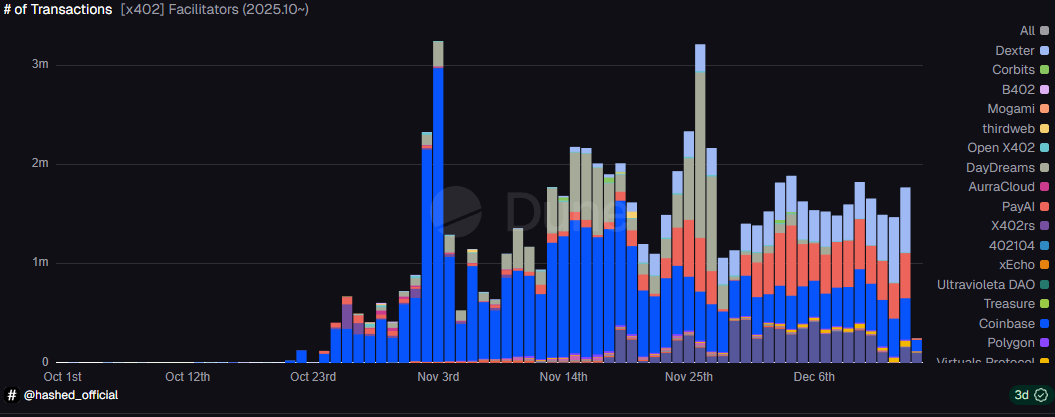

x402 is a starting gun, not a flash in the pan

In case you missed it, x402 is a standard for native internet payments between clients and servers. It’s built into native HTTP requests and has been developed by Coinbase and Cloudflare.

It allows servers to monetize APIs in great detail; removes the frictions of credit cards, such as high fees, delays, and chargebacks; and enables microtransactions at a whole new scale.

Some quick examples of use cases:

- API monetization: Cloudflare users can now “pay per crawl,” so developers and agents only pay for the data they actually consume.

- Native payment capabilities for AI agents, which can pay for data, compute, or cloud services with their crypto wallets.

- Pay-per-use for AI models via APIs.

The majority of usage thus far is coming from API services (e.g., Canza, Dexter, t54), agent experiments (e.g., x402monopoly, Lucy), and payment providers (e.g., Alsa, payAI), with activity split roughly ⅔ on Base and ⅓ on Solana in terms of transaction count.

Adoption has been as steady as it has been sticky, with names like Daydreams, Heurist, and our old friends Virtuals each trying out the tech.

Out of everything we’ve seen come (and go) from the “crypto x AI agents” field, x402 feels different. It goes beyond crypto-native; it’s browser-native.

X402 solves the original sin of the internet, which required an advertising-supported model since hosting websites costs money, and no one wants to whip out their credit card every time they Google their sports scores or Sydney Sweeney’s feet.

In the end, I’d wager that the vast majority of x402’s use will be abstracted from users, and it will be the API aggregators and application builders that capture this upside.

Anthropic has already integrated x402 into MCP, enabling Claude agents to handle payments automatically. But this is the real deal, and I’m excited to see what kinds of experiments will be run on our little blockchains.

A couple of ideas include:

- Inference DePINs, such as Chutes, Hyperbolic, and Inference, could integrate x402 to remove the need to onboard funds from credit/debit cards and more easily onboard agents.

- Privately-hosted agent protocols could use x402 to connect to data streams and services while keeping inference and local data private.

- Honestly, I just want to be able to checkout from Amazon using my Rabby wallet - when will I be able to do this? Speaking of which, if I could also pay $0.02 to skip an ad or $1 to break through an article paywall without taking out my wallet, that’d be great.

- Even devs don’t like API key management - abstracting that away on top of x402 payment abstraction opens the door to “everything” apps that let you plug into literally anything that has an API endpoint.

All without a lick of technical knowledge - you just know it’ll cost $0.58 to complete your request because that’s what your agent is being quoted from 18 different providers.

On the crypto side, here are the trends already in motion:

- The Ethereum Foundation’s 2026 roadmap includes a focus on agentic coordination/settlement by marrying x402 with their EIP-8004 (agent registry standard for identity/discover) standard.

Also look out for EIP-7857, which aims to be a privacy layer for x402, that’s slated for 2027 but we’ll probably see the early stages of it in 2026. Note that Fhenix just launched Fhenix402 on Base testnet, their own privacy-preserving version of the protocol. - Coinbase’s championing of the protocol makes us think that they will be strongly supportive of applications building on top of their stack, including crypto/stock trading, their in-house prediction markets, credit/debit integration, and agent-driven yield generation.

- Lightning Network is actually getting a bit of love for once. LnPay from Alsa has been one of the top x402 servers by total transactions.

It’s still early, but development has been rapid, with v2 of the protocol already going live in December. If you only have the mental bandwidth to track 1 thing from AI agent land, let it be this.

Follow list:

- Nemil Dalal (@nemild): YC visiting partner & x402 ambassador, former Coinbase Dev lead & USDC lead

- Eric Reppel (@programmer): Coinbase Dev Head of Engineering, creator of x402

- YQ (@yq_acc): built 8004scan.io and writes a lot about x402

We’re not the only ones with Zero Knowledge anymore

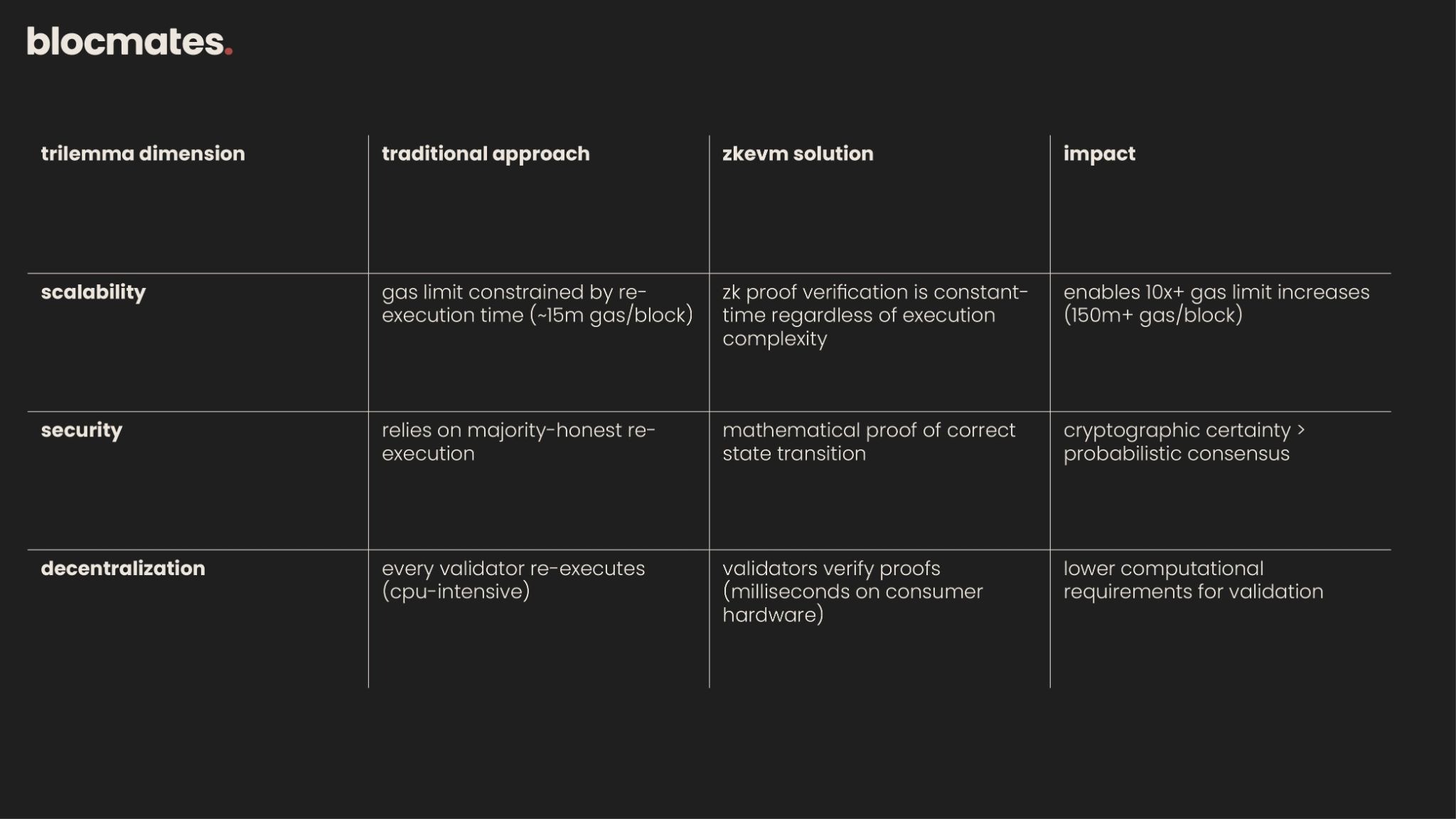

If you only half-follow the discourse of blockchain tech, you may have missed the vibe shift in Vitalik’s post here, claiming victory over the blockchain trilemma of scalability, security, and decentralization:

Ethereum infamously forwent scalability for the sake of decentralization and security, pushing for the L2 roadmap to make up the difference. But that’s not where our story ends.

PeerDAS’ (Peer Data Availability Sampling) launch with Ethereum’s Fusaka upgrade in early December allows validators to verify blob data availability through sampling just a small subset instead of downloading the full blob data.

In essence, this supports Ethereum’s goal of jacking up bandwidth through distributed work (and not “replicated” work), and it’s a big win for improving the network’s scalability.

But zkEVM takes it to another level entirely. The basic gist is that instead of requiring every validator to re-execute every transaction, they just have to check a proof to verify that the block executed as expected.

This drastically cuts down on redundant execution and actually helps all three legs of the trilemma:

The combination of PeerDAS and zkEVM results in an order of magnitude decrease in throughput requirements for validators, without compromising security (through cryptographic proofs) nor decentralization (it actually lowers validator hardware requirements).

And contrary to popular belief, this isn’t just for rollup scaling. Native mainnet apps can leverage blobs to store temporary data (leveraging PeerDAS gets us ~6x improvement over pre-Fusaka blobs), and the L1 itself will see a 5-10x throughput improvement from zkEVM as more validators adopt the technology.

So while L1 capacity increases are prerequisites for L2 scaling, they also enable direct L1 usage at higher throughput. The mainnet itself is becoming more capable, not just a settlement layer for L2s.

We’re moving away from the world of “expensive L1 vs cheap L2s” and towards our 2017 wet dream of “scalable L1 + ultra-scalable L2s.”

Or in Vitalik’s words, “you can just build on L1.”

Expect to see some hype driven to some/all of the names below once this tech starts seeing early adoption in 2026 (whether deservedly or not):

- Rollups with ZK tech: zkSync, Starknet, Linea, Scroll, Polygon zkEVM

- Privacy tech that uses ZK: Railgun, VEIL, Umbra

- Infrastructure that uses ZK: Succinct, Brevis, ALEO

- I’d even throw tangentially-related privacy projects into this: ZCash, Humanity, Worldchain, Nockchain

Crypto rails

Super Apps are the endgame for consumer crypto, so connecting the data and cross-chain liquidity required to power these apps will be key in 2026. The focus will shift to bundling DeFi apps into cohesive experiences and connecting liquidity across chains to improve product capability and UX.

To date, the incumbents, including bridges, oracles, and intents*, have established defensible moats by solving highly specialized problems. Some examples include:

- Unit bridge to Hyperliquid

- Pyth oracle to SVM

- Chainlink oracle to EVM (CCIP and SVR)

- Layerzero (Omnichain - USDT0)

However, going into 2026, these projects aren’t just competing with their peers; they are also competing with networks at the foundation level, developing interoperability solutions.

Ethereum recently released plans for the Ethereum Interoperability Layer (EIL), which aims to unify all L2s, enabling cross-chain swaps and transfers without traditional bridges.

When this goes to mainnet, it could limit the addressable market of cross-chain bridges and potentially put L2-specific bridges completely out of business.

In addition, this new model forces new L2s to enter the market with a seriously defensible moat. If liquidity is no longer a hurdle, then the technology and unique selling points of each chain will be the deciding factors for applications and users.

It’s important to note that EIL requires adoption from multiple parties, including wallets, rollups, and dApps.

For instance, if a wallet supports EIL but a target L2 doesn’t, the wallet won’t use the EIL route, and the user will have to fall back to normal bridging/swapping. Currently, EIL is available for public testing on testnet, with no official release date for mainnet at the moment.

An alternative design path for interoperability set to experience growth in 2026 is intents.

With intents, end users submit a request, and the app relays it to a network of solvers that coordinate the underlying transactions and transfer of funds across chains if needed.

The goal is to give the user a seamless experience while solvers help to complete complex cross-chain transactions, under the hood. Some projects building intent solutions include Near and Li.Fi.

Intents, similar to bridges and oracles, will be a battle of which projects can land the deepest integrations to increase their edge.

2026 for crypto rails may not mean aggressively positive PA, but it will definitely provide insight into the fundamental rails that onchain businesses are building atop.

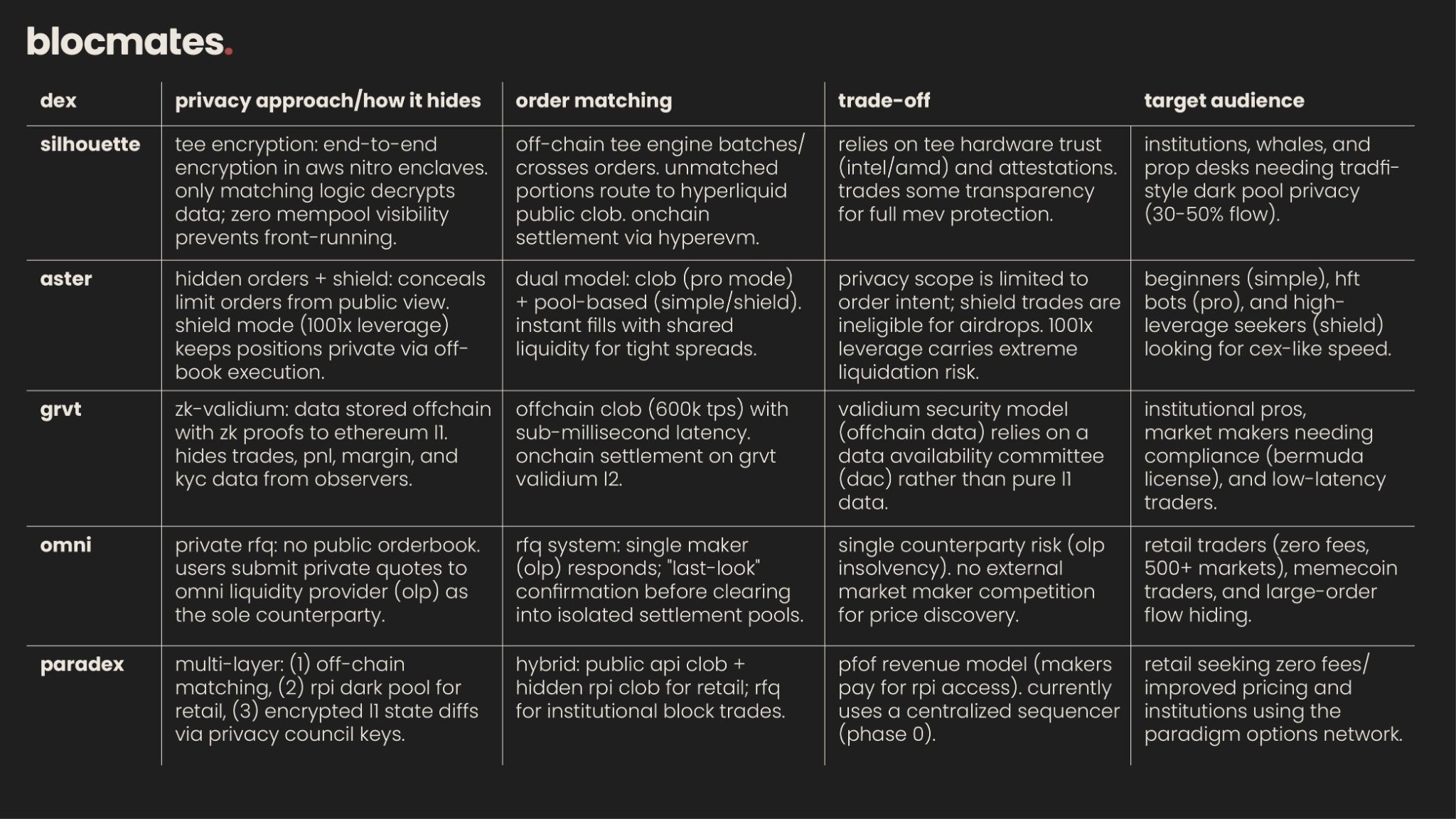

Dark pools

In 2026, onchain exchanges will compete to match the features of CEXs that whales find irreplaceable, including hiding intent and trade size. Institutional traders will optimize for execution certainty, information control, and capital efficiency.

All trades onchain, however, are public, leading to information leakage. For established traders, this poses a threat of adverse selection: when one side of the trade systematically has better information than the other.

In trading environments, this shows up as wider spreads, fragile liquidity during volatility, and repeated losses for passive liquidity providers who can be traded against ahead of price-moving events.

In this case, privacy is key because if trade intent isn’t visible, it’s harder to be selected against.

On CEXs like Binance, they address this by offering request for quotes (RFQs) and block trades, which obfuscate order size and intent until the trade is completed. This moves trades away from public order books.

However, RFQs aren’t as simple to replicate onchain permisionlessly, so for crypto, dark pools (and equivalents) are the solution.

But not all dark pools are created equal. Depending on how the platform hides details and the specific details, it will attract traders of different sizes.

For instance, platforms like Silhouette, which allow you to hide your balance, may attract more institutional users who are used to that level of anonymity with centralized RFQs.

As perp DEXs grow in popularity, naturally, comparisons among platforms will surface.

You can expect seemingly minute differences to be magnified, establishing a hierarchy over time based on whichever feature set is more sought after by whales.

Here’s a list of perp DEXs and some of their tradeoffs when it comes to privacy and dark pools:

Dark pools are a relatively new primitive, and their effect on DeFi markets hasn’t been fully studied.

In terms of risk, however, I can think of two ways dark pools negatively impact the market:

- If too many traders go dark, then the lack of pre-trade transparency can obscure order flow, making it harder for traders to infer supply and demand.

- Dark pools could be used nefariously for hedging /shorting one's own tokens with shielded transactions.

Coming into the new year, both perp DEXs and privacy are top narratives. As a result, expect dark pools – along with their effects on UX and public trade execution – to play a major role in how Perp DEXs are viewed and how their user bases develop.

DeFi: The year of lending and leverage

By the end of 2025, lending platforms reached $63 billion in TVL, becoming the largest sector in DeFi. During the same period, Perp volumes reached all-time highs and even outpaced spot DEX volumes on a rolling basis.

2026 will follow the same trend, with the focus being on venues for leverage: perps platforms on the volatile end and lending protocols on the conservative end.

Perp DEXs

In crypto, traders prefer placing leveraged directional bets as opposed to holding spot assets. But it’s not surprising: Perps offer easy shorting, and give traders leverage to increase value per dollar – basically a trader’s dream.

This trend can also be seen across major CEXs, where Crypto futures volume for BTC was 3x or more spot volume over the course of 2025.

Now, in 2026, perps platforms are introducing more commodities, equities, and Pre-IPO stocks, giving us a glimpse of whether that same appetite appears for TradFi assets.

In addition, markets for GPUs, trading cards, and Polymarket bets will help to gauge interest in long-tail markets.

Beyond asset listings, perp DEXs will compete on execution quality and privacy. However, small traders and whales prioritize different things.

Typically, smaller traders are more price sensitive compared to whales who’ll often pay a larger upfront fee for lower overall execution cost (less market impact and info leakage).

Over time, these preferences will segment platforms by their user base: pro and retail.

Pro platforms are more likely to attract sticky liquidity from whales, while “retail” platforms, on the other hand, risk commodification in an overcrowded market, where the competition comes down to incentives and fees.

To support the growth of open interest (OI), perps platforms will need deep liquidity, which makes Perpetual Demand Lending Pools (PDLPs) increasingly important.

Top-performing platforms won’t just optimize for the trader experience but also for vault structures and making returns more predictable.

Platforms that capture sticky liquidity will become “liquidity primitives” that developers can build structured products on top of, which means wider distribution and… more liquidity.

Early PDLP-style structured products include:

- Unitas SUSDU (Jupiter JLP)

- Hyperlend wHLP (Hyperliquid HLP)

- Gauntlet hJLP (Jupiter JLP)

- gUSDC PT/YT (Gains gUSDC)

Hot take: With speculative activity fueling PDLPs, they may go down as one of the top growth assets of 2026.

Lending and low-risk DeFi

Lending platforms are becoming the poster child for “low-risk DeFi” - apps that democratize access to payments and savings in valuable asset categories.

According to Vitalik, to be considered in this category, an app must have the following characteristics:

- Contribute to the network economically through large volumes of ETH as collateral and high volumes of transaction fees.

- Provide irreplaceable value, which, in the case of lending markets, means democratizing global access to savings.

If you’ve been paying attention to our reports, this ecosystem-level flight to “low-risk DeFi” is not surprising.

Over time, networks require simple yet positive-sum products that generate revenue, and naturally, lending markets have grown to fill this gap.

Historically, lending markets have been one of the most durable products in DeFi. They’ve survived all previous market downturns and narrative shifts in crypto, and now, hold the spot for the largest category with a TVL of $63 billion.

Liquidity begets liquidity, right? Established platforms like Aave and Morpho attract third-party apps to plug in, offering their users access to onchain vaults.

This creates a distribution flywheel where integrations lead to more flow and more liquidity.

In 2026, there are a few primitives I believe can increase liquidity and capabilities of lending markets:

- Cross-chain intents: Cross-chain intents could increase yield rates by aggregating lending opportunities across networks based on the most competitive rates. For example, push the boundaries of yield achievable from “low-risk DeFi” apps.

- Hybrid-lending primitives: Lending platforms that combine lending with primitives like DEX liquidity pools can help to increase deposit yield during times of trading volatility.

The above examples should help to enhance yield rates for “low-risk DeFi” strategies in 2026. But, in general, leading markets are a foundational primitive that offer potential for many future applications.

Vault curation

Vault curators are essentially onchain portfolio managers that combine existing products, like lending and trading, into automated strategies called vaults.

Presently, vault curators control a combined $5 billion in TVL across platforms like Morpho, Kamino, and Jupiter Lend.

Currently, the top vault curators by TVL are:

- Steakhouse $1.6 billion

- Gauntlet $1.266 billion

- Sentora $581.1 million

- K3 Capital $297.8 million

- MEV Capital $232.14 million

Together, they’re one of the first groups to make a concerted effort towards risk management in DeFi.

Gauntlet, specifically, publishes in-depth research on the mechanics of DeFi primitives and recently released the Vault Book, documentation detailing how vaults and curators operate.

Over time, vault curators will help to establish what is considered “low-risk,” and this authority will give them influence over where liquidity flows.

For example, established risk curators that deploy vaults to a new platform could be seen by retail as a stamp of approval, easing the friction of onboarding new liquidity.

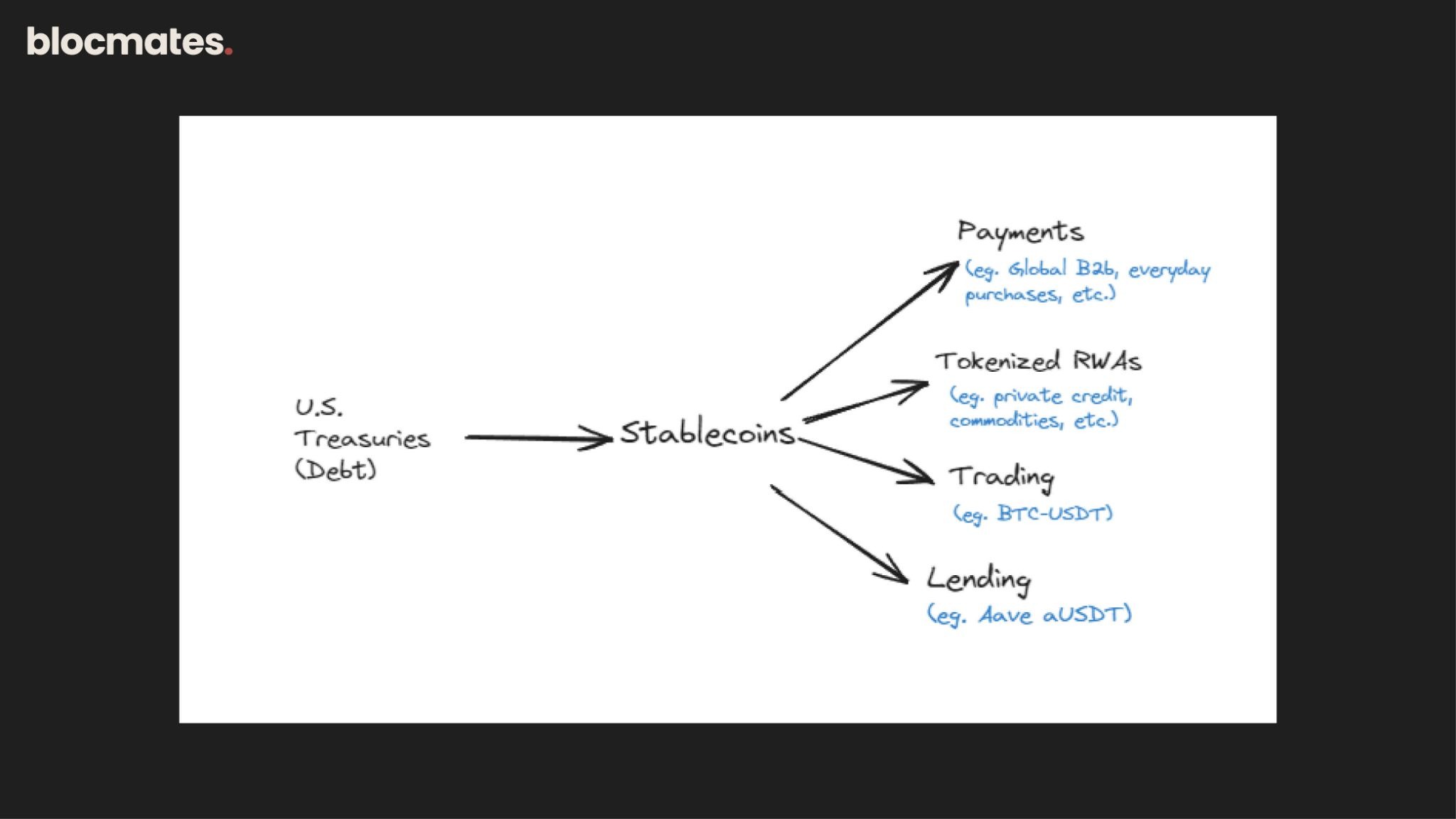

Stablecoins

Stablecoins are used in pretty much every corner of the industry, and as a result, they are crypto’s most successful product, from both revenue and adoption standpoints.

In emerging markets, citizens rely on stablecoins for everyday purchases, and institutions and businesses are continually integrating stablecoin rails to improve capital efficiency.

However, there are still Western countries like the US that lack the PoS integrations and merchant distribution to integrate stablecoins into everyday life.

In 2026, this will change. Expect more stablecoin deployments and integrations.

Stablecoins in DeFi

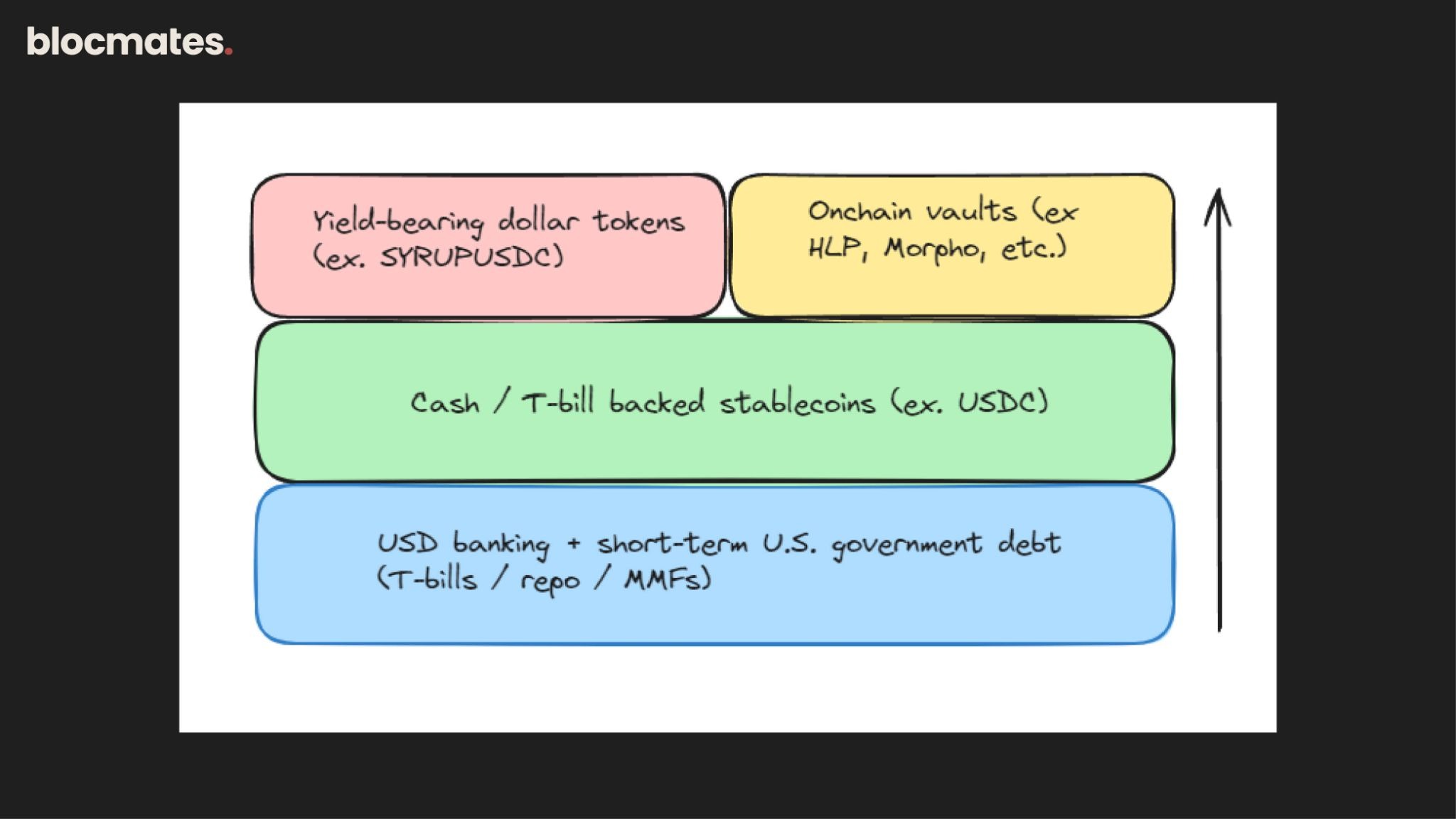

With regulations like the US GENIUS Act and EU MiCA, the landscape is evolving. These frameworks establish a base layer for fiat-backed stablecoins that behave as “cash-like” tokens.

Over time, that clarity should ease the friction of integrating stablecoins into payment stacks, including B2B payments, payroll, and eventually point of sales flows.

In December 2025, YouTube unveiled a feature to let creators receive payments in PYUSD via PayPal. Integrations like this are only the beginning.

In addition, with a formalized base layer, it pushes yield-bearing stables up the stack into wrappers, strategy vaults, and tokenized products.

Clearer compliance around how products should be structured will encourage more projects to go to market without fear of getting stuck in a grey zone.

They can either choose to launch a payment-compliant stablecoin similar to USDT and USDC or a yield-bearing dollar token like Franklin Templeton’s BENJI, and Ondo’s USDY token.

That said, even after the GENIUS Act passed, banks in the US have been lobbying hard to close the yield loophole.

GENIUS already restricts issuers from paying holders yield “solely” due to holding/use/retention. But this still allows third-party apps to integrate in the backend and issue yield via DeFi rails –mimicking deposit interest.

Banks see this as a threat because if you can earn a higher interest rate with stablecoin deposits, then why use a bank?

As a result, they’re using this round of follow-on legislation to limit “stablecoin rewards to only merchant-facing transactions and excluding stablecoins held for safekeeping from reward eligibility.”

In other words, they’re trying to treat stablecoins like credit cards. You only get rewards if you spend.

If this made its way through Congress, it would limit the amount of third-party integrations possible, slowing the “superapp thesis”.

At the same time, this would consolidate yield to onchain vaults, while leaving some yield-bearing tokens in a regulatory grey area. In this future, documentation and product design will make a world of difference when considering going to market.

While this doesn’t completely stifle the growth of stablecoins, it will shape the design space for future builders.

Whether or not the loophole gets closed, banks are still moving to integrate stablecoins; they just want to do it on their own terms. For banks, stablecoins provide immense benefits. Lower operational costs, higher transaction speeds, and more capital efficiency are just a few.

Stablecoins-as-a-service (SAAS)

This ripple effect will expand past DeFi, making it attainable for virtually any business to launch a proprietary stablecoin.

Not every business will need one, but for businesses with looped economies, private stablecoin offers access controls and a claim over fees that can be rerouted to enrich the network.

Some early projects offering stablecoin as a service include:

- M0

- Coinbase

- Ethena

- Bridge by Stripe

- Tempo TIP-20

With the correct infrastructure in place, crypto becomes part of the toolbelt of all these Fortune 500 companies. Leaving this out of the stack risks being left behind.

Ultimately, this all contributes to the endgame: Stablecoins becoming household names worldwide.

Conclusion

If there’s one thread running through all of this, it’s that crypto is no longer allowed to pretend. Not about decentralization. Not about ownership. Not about value creation. The industry spent a decade telling stories - some visionary, some vaporware, and now the bill is due.

What’s emerging in 2026 is a harsher, but ultimately healthier, equilibrium.

Real businesses are using crypto rails not because it looks good on a pitch deck. They're using it because it makes them faster, cheaper, and more capital-efficient.

Tokens are being forced to justify their existence in concrete terms, and chains themselves are being repriced.

This new phase favors distribution over innovation, execution over timing, and second movers over pioneers who confused being early with being right.

Crypto winning means crypto becoming boring, invisible, and everywhere - embedded in payments, markets, and software stacks where nobody stops to ask if it’s “onchain.”

I’m sure we’ve missed a few points here and there, but we’ll keep rolling out follow-up research articles as and when new narratives pick up steam.

We hope this thesis gave you something of value, and we wish you all the best as we head into the 2026 battlefield.

Footnotes

If you are looking for a place to chat about the markets, then the blocmates Discord is open to everyone for free. You can join here.

We also have an active community on Telegram. You can join here.

If you enjoyed this report, this is only scratching the surface of what we cover at blocmates.

Last year, we dropped over 130 free research reports, 50+ podcasts, 260 newsletter editions, 50+ premium research reports, and more than a dozen IRL interviews.

Expect bigger guests, better content, and more value from us this year. You can follow all the action on our Twitter/X account here.

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)