Ape-tizers:

- Wildcat is bringing undercollateralized credit onchain, letting borrowers set terms and lenders decide if they want in.

- DAOs, funds, and protocols can now tap credit rails without selling tokens or running OTC deals.

- Recent partnerships, like with Ethena, show Wildcat’s credit markets can double as yield engines, stacking incentives on top of fixed APR.

Tabs are the oldest kind of credit most of us have ever used. Your corner bar lets you run one because the bartender knows you, you show up often, and you pay when you say you will. Restaurants do the same at scale with suppliers.

“Net-30” is just a grown-up tab. Milk and oysters arrive today, the bill gets settled next month, and the lights in the kitchen stay on. Notice how none of that looks like “overcollateralize” or “get rekt”?

That is how real economies move. Trust gets time-shifted, not by locking up twice the value of the oysters, but by a mix of reputation, terms, and the threat of getting cut off if you miss. It is messy and human, but it works. It lets businesses breathe without selling furniture every week.

Crypto, though, never really nailed this.

We built perfect ledgers and then told everyone to prepay. You want a loan, great, park a bigger pile of assets first. That is safe, but it is not how a DAO pays contributors, how a fund scales a strategy, or how a protocol buys itself a runway. What is missing is the onchain version of a tab.

Clear terms, visible risk, and the ability to say yes or no without sending a PDF over Telegram.

That’s the gap WildcatFi is tryna fill. A protocol for undercollateralized credit where borrowers set their own terms and lenders decide if they want in. Simple idea, but one that opens up entirely new ways for both sides to use onchain markets.

What is Wildcat?

In traditional banks, loans get sanctioned when you’re known. DeFi has been chasing that trustless ideal, but didn’t get the “trust” part right. Wildcat wants to bring that trust back - programmable, and still auditable.

At its core, Wildcat is a decentralized credit layer that enables undercollateralized lending on Ethereum. Instead of forcing borrowers to lock up excess capital, it lets them launch markets where they define loan terms like size, interest, and liquidity buffers.

Lenders opt in directly to these terms, creating a programmable credit agreement that lives fully onchain. Wildcat is not just consumer-facing either – DAOs, funds, and protocols can all use it to access or provide credit without going through banks or OTC desks.

Plasma recently announced a partnership with WildcatFi to build a transparent global credit layer, enabling lending models like short-term financing and real-time settlement that traditional markets don’t usually support.

Wildcat will be the launch partner when Plasma’s mainnet test goes live.

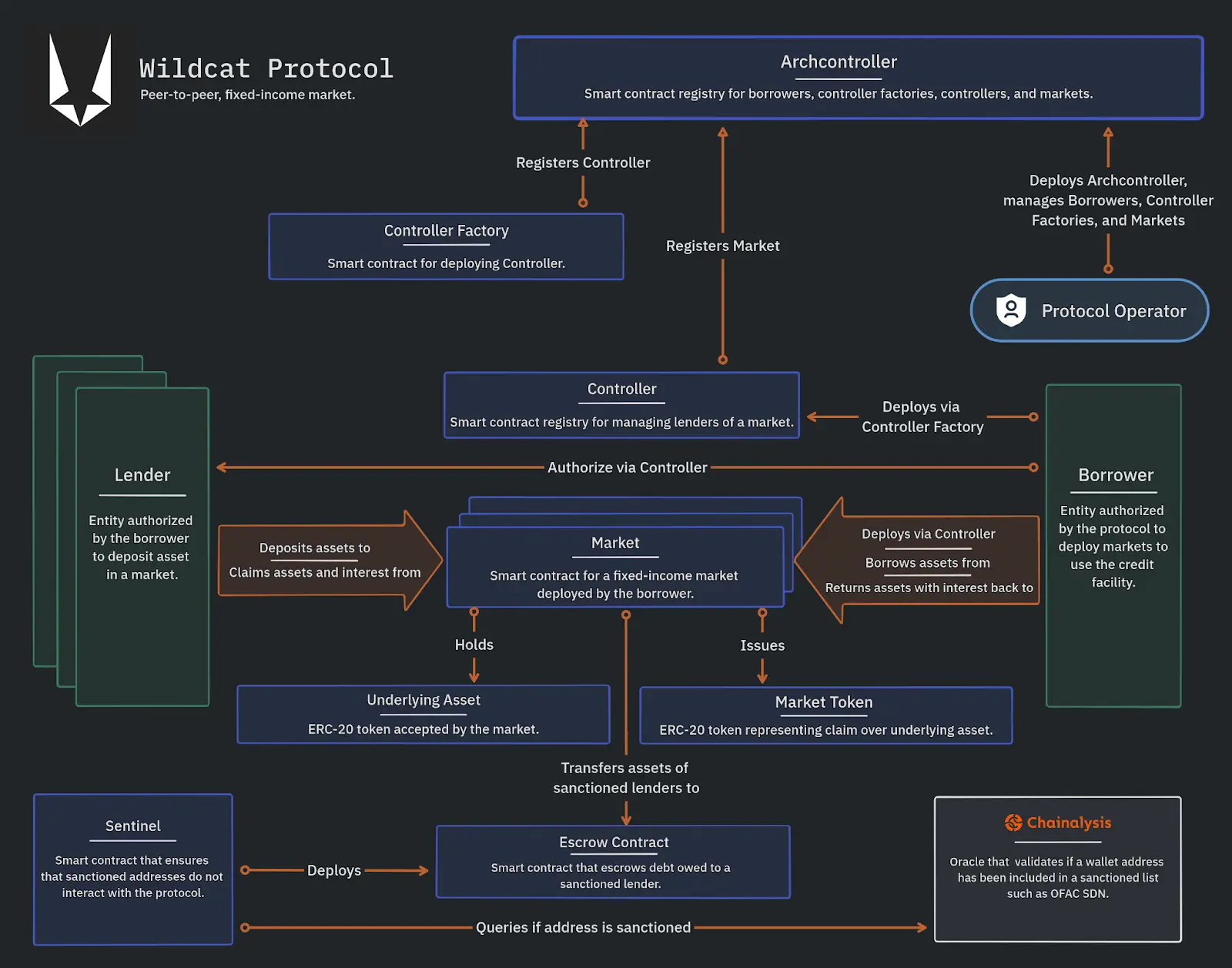

Under the hood: How Wildcat is built

Wildcat isn’t trying to sell you some galaxy-brained new primitive. It’s just credit, but actually usable onchain.

At a glance, it might look deceptively simple. Borrowers spin up vaults, lenders decide if they want in. Underneath, though, there’s a set of moving parts that keeps the whole thing from turning into a free-for-all.

Don’t get too fazed by this image, let me break it down for you in simple terms.

Archcontroller

The Archcontroller acts as the gatekeeper, making sure only approved borrowers can deploy vaults. The checks happen mostly offchain (think KYC/KYB-style vetting) so when you see a vault live, you know the borrower has at least passed some level of scrutiny.

Sentinel

The Sentinel is the protocol’s compliance layer. It runs automated checks (using Chainalysis and similar tools) to make sure lenders aren’t sanctioned wallets or flagged entities. If it finds something, it can move that lender’s position into escrow until the issue is sorted out. It’s basically the circuit breaker that keeps the system clean.

Controllers

Controllers are contracts that define how a borrower’s vault operates. They hold the borrower’s address, decide who can lend, check whether parameters make sense, and outline how those parameters can evolve over time. Basically, if the Archcontroller decides who gets to play, the Controllers set the rules of the game.

Factory

Every new vault passes through the Factory, which acts like a template and a sanity check. Borrowers can propose terms, but the Factory makes sure they aren’t sneaking in anything outrageous.

Vault

The vault is where the real action happens. Lenders deposit, borrowers borrow, and debt tokens start accruing interest. The borrower sets terms like reserve ratios, caps, interest rates, and redemption windows, and lenders decide whether to play ball.

Wildcat V2: Bigger, leaner, on mainnet

The first version of Wildcat required a lot of manual back-and-forth. That’s why February 2025 brought Wildcat V2 on Ethereum Mainnet. V2 smooths things out by introducing “hooks,” modular conditions that can be baked into vault logic.

- Lenders can be whitelisted automatically based on NFTs, SBTs, or off-chain credentials.

- Minimum deposits can be enforced directly at the contract level.

- Borrowers can set fixed loan durations instead of just perpetual ones

Hooks cut out the logistics and make Wildcat markets easier to run, closer to proper credit rails than handshake deals in Telegram chats.

How to play Wildcat

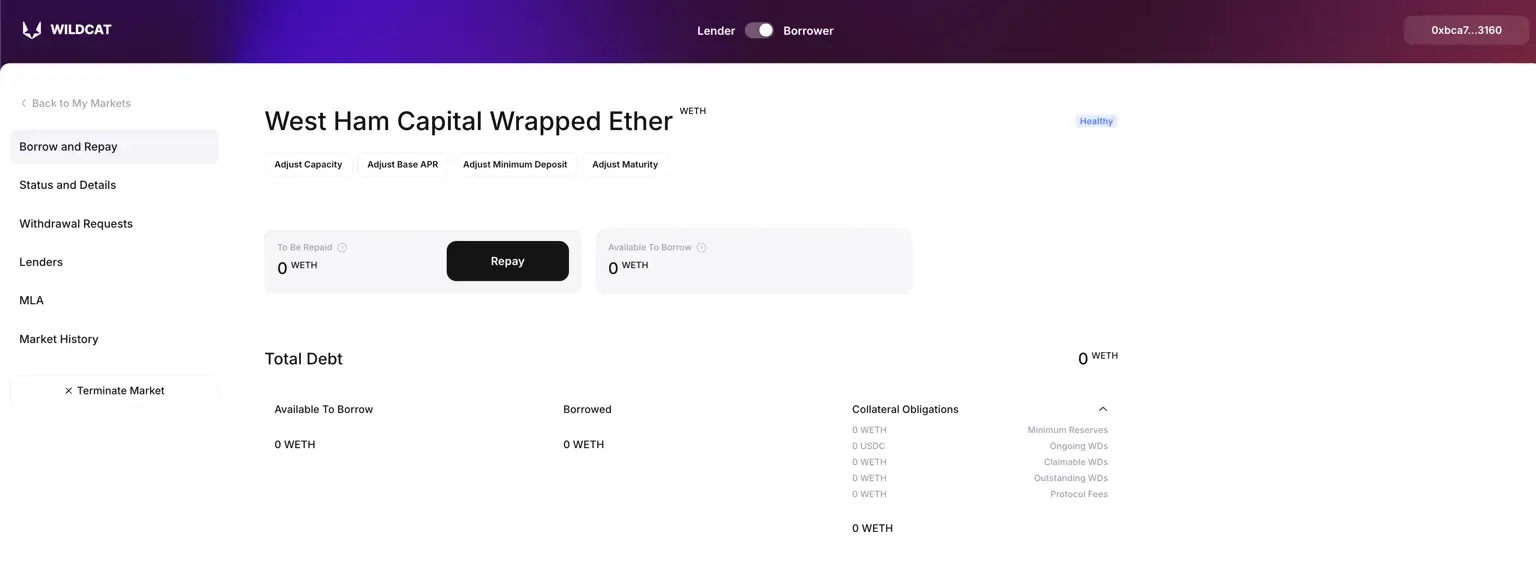

For Borrowers

As a borrower on Wildcat, you first need to be whitelisted by the Archcontroller. Once approved, you can flip into “Borrower” mode on the app, update your profile, and create a new market.

When setting up a market, you define its key parameters:

- Market type: Open-term (withdraw anytime) or fixed-term (locked until maturity). Fixed-term markets can allow early repayment or maturity reduction if you choose.

- Access control: Lenders can self-onboard (unless sanctioned) or be added manually to an allowlist.

- Underlying asset: Usually a stablecoin or ERC-20. Avoid rebasing tokens like stETH, which break interest calculations.

- Market token name/symbol: Identifiers for the debt tokens lenders receive.

- Terms: Borrowing capacity, base APR, penalty APR (applied if reserves fall below requirement), reserve ratio (minimum liquidity buffer), grace period before penalties kick in, withdrawal cycle duration, and minimum deposit.

Lenders deposit into your vault and receive debt tokens that accrue interest. You can adjust things like APR (with limits), capacity, or minimum deposit over time. Repayment is as simple as sending assets back into the vault.

Markets can be closed at any time by repaying fully, after which lenders just file withdrawals and exit. Attaching a Master Loan Agreement (MLA) adds legal clarity, though it’s optional.

Wildcat’s design leaves responsibility with the borrower - you set the terms, maintain reserves, and keep lenders engaged.

If done right, it gives you flexible, undercollateralized credit rails without the old-school backroom deals.

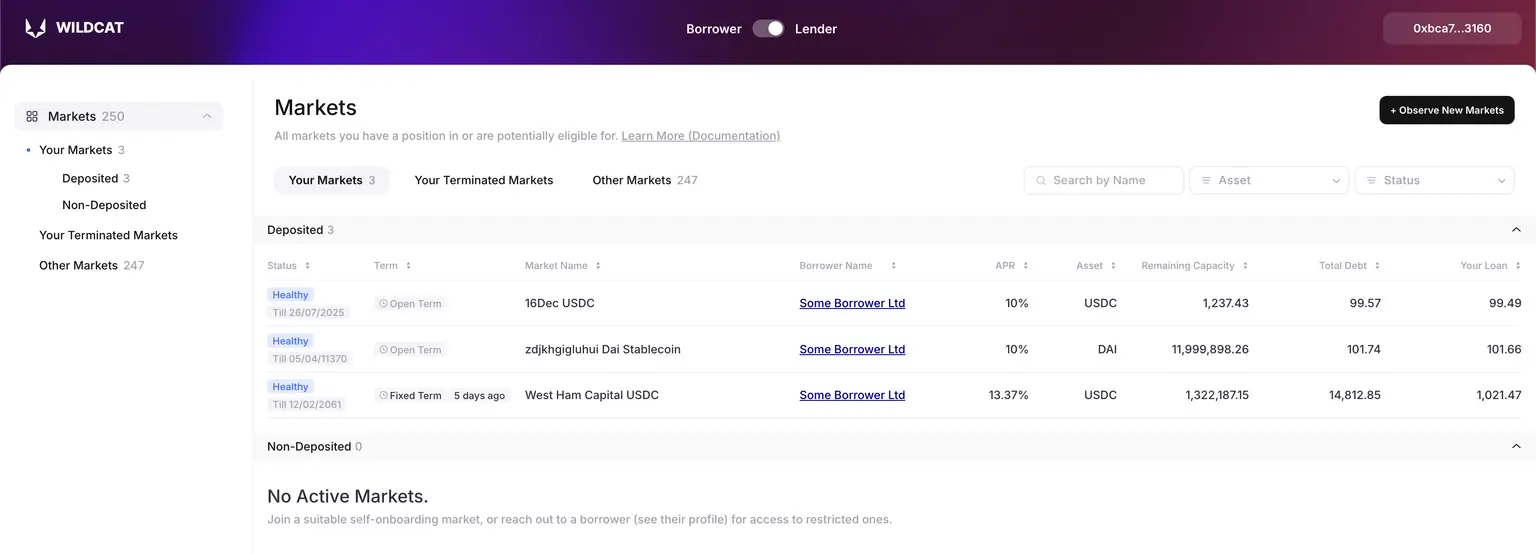

For lenders

As a lender on Wildcat, your job is just as simple: pick a market, deposit assets, and earn fixed interest. But unlike Aave-style lending, Wildcat does not guarantee repayment, and you’re taking on direct borrower risk.

Markets come in two ways:

- Self-onboarding: Anyone can deposit (unless flagged by sanctions checks).

- Borrower-approved: You’ll need to be whitelisted by the borrower.

If the market uses an MLA, you sign it with your wallet, locking in enforceable terms. If not, you can still deposit directly.

When you deposit, you get market tokens (1:1 with the underlying asset). These tokens accrue interest automatically. Depending on borrower settings, market tokens may be freely transferable or restricted to approved wallets.

Withdrawals don’t happen instantly. Each market has a withdrawal cycle defined by the borrower. To exit, you burn your market tokens and wait for the cycle to complete.

If reserves cover all requests, you’re paid out in full. If not, you receive a proportional share, and any leftover claims sit in a queue to be repaid as the borrower replenishes reserves.

It’s not risk-free: repayment depends on the borrower’s discipline, and Wildcat won’t bail you out. But that’s the point, you’re lending directly, onchain, with programmable terms and visible risk.

If you want the detailed step-by-step version, the docs cover it pretty well.

Grabbing the limelight

Wildcat is starting to gain attention for one simple reason: it’s actually landing real deals. Just last week, they spun up a market where lenders could put USDe to work with Hyperithm at 11.5% APR and, on top of that, stack 20x Ethena points. For anyone farming points or squeezing yield, that’s about as meta as it gets.

Visibility is also ticking up. DefiLlama already tracks Wildcat pools right alongside Aave, Compound, and Co.

That kind of dashboard presence matters since it signals the market is starting to take Wildcat seriously and not just as some experimental credit primitive.

And the institutional angle is hard to ignore. Hyperithm opened a $10 million USDe market, and Plasma tapped Wildcat as its launch partner to build a global credit layer. That puts Wildcat in the middle of both DeFi-native and TradFi-adjacent flows.

It’s early, but the momentum is real. They’re not just pitching “onchain tabs” anymore but have actual people running them.

Why Wildcat is important

Most of DeFi still pretends credit only works if you lock up more than you borrow. That keeps traders happy, but it doesn’t look anything like how businesses or communities actually run. Wildcat is basically bringing back real credit dynamics.

Here is why that’s important:

- No overcollateralization: Traditional overcollateralized models work for traders, but not for DAOs, funds, or protocols. Wildcat removes that roadblock and unlocks usable credit. It basically ditches the “2x collateral or get rekt” model.

- Clear, programmable terms: Borrowers set the parameters, lenders choose if they accept them. Everything is written into the contract, no “trust me bro.”

- Broader use cases: Beyond speculation, Wildcat gives DAOs, protocols, and funds a way to raise working capital without selling tokens or relying on banks.

- Transparent risk management: Compliance checks, optional MLAs, and visible vault data keep lenders informed and give borrowers credibility. You basically know what you’re signing up for.

- Composability with DeFi: Markets can integrate with existing ecosystems (like the Ethena points example), turning credit markets into yield and incentive engines.

Concluding thoughts

The thing that strikes me about Wildcat is how obvious it feels once you see it. Credit is not new; we’ve been running on it forever, but onchain, it’s always been this awkward dance of “lock up more than you borrow or get nothing.”

That model works for traders and speculators, but it doesn’t look anything like how actual businesses or communities operate.

The funny thing about credit is that it has always been a social game dressed up as finance. Behind every “net-30” invoice or bar tab is the same simple premise: you trust me, I’ll make good on it, and if I don’t, you cut me off.

Somewhere along the way, crypto stripped all the human parts out and left us with math problems and collateral requirements. Safe, sure, but sterile. Nobody builds an empire by prepaying their way through life.

Wildcat feels like a pushback at that rigidity. The potential is there – DAOs, funds, protocols – anyone tired of the prepay culture can finally get access to real credit rails.

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)