Ape-tizers:

- Since 2021, the total market capitalization of stablecoins has increased by nearly 1000%.

- The US Senate has passed the stablecoin bill, dubbed the GENIUS Act.

- With a 62% dominance in the stablecoin market, the adoption of Tether’s USDT is showing no signs of slowing down.

- As the regulatory environment in the US becomes clearer, competition in the stablecoin sector is intensifying.

Two key factors are fueling the recent rise in stablecoin adoption. First, companies are increasingly recognizing the considerable potential to reduce transaction fees by millions and enhance payment infrastructure through instant settlement.

Secondly, the surge in crypto adoption on Wall Street is supported by increasing backing in Washington. The Senate approved its framework of rules for stablecoins, called the GENIUS Act. The bill includes guidelines for consumer protections, reserve requirements for issuers, and anti-money laundering measures.

Recently, the wildly successful Circle IPO, where investors sent the stock soaring as much as 750%, has certainly proved the insatiable appetite for exposure to stablecoins.

The competition responded as well, with Coinbase revealing a partnership with Shopify to facilitate USDC payments for merchants. Additionally, payments company Fiserv launched a stablecoin to accompany the 90 billion transactions it processes each year.

What this essentially does is foreshadow what’s to come — the imminent arrival of stablecoin wars.

What is a stablecoin?

A stablecoin is a type of crypto asset that is tied to a specific value, most often matching the US dollar or, in some cases, commodities like gold or silver.

Various mechanisms keep the stablecoin’s price aligned with its peg, typically involving some form of collateral. This collateral can be in the form of reserves equal to 1:1, partial backing, or, for certain on-chain stablecoins, overcollateralization.

For USDT and USDC, two of the most popular stablecoins, the companies that issue them buy an equivalent amount of fiat currency, US short-term treasuries, or other liquid assets for reserves.

This not only ensures the company can handle redemptions, but also earns them interest, which is how they generate revenue. Simple and elegant.

Stablecoin supercycle (real)

Citibank, in its recent stablecoin report, states that the total outstanding supply of stablecoins could grow to $1.6 trillion by 2030 in its base case and to $3.7 trillion in its bull case. With the total supply currently standing at around $260 billion, that represents a potential increase of more than five times.

Naturally, major players are paying attention. Visa, MasterCard, PayPal, BlackRock, JPMorgan, Stripe, and others have indicated their intention to join or have already entered the space, aiming to capture a share of the expanding market.

On that note, let’s explore how the largest financial players in the world are approaching the stablecoin sector.

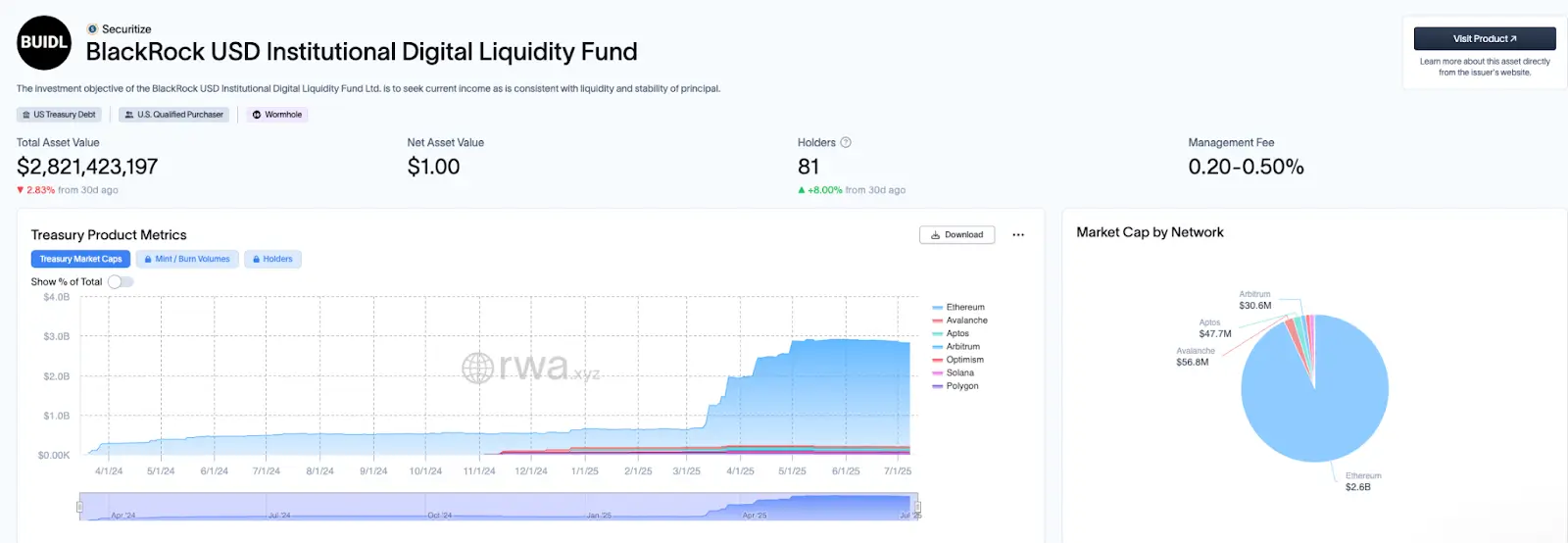

BlackRock’s BUIDL

If there is money to be made, you bet BlackRock wants a taste of it.

Launched on Ethereum in March 2024, USD Institutional Digital Liquidity Fund (BUIDL) is fully backed by cash, US Treasury bills, and repurchase agreements.

In a little over a year since its inception, BUIDL has amassed more than $2.8 billion in deposits, proving the massive appetite for such an asset.

While not the best name in town, and accessible only to accredited investors with a minimum investment of $5 million, BUIDL offers several advantages over USDT and USDC.

Its key benefits include providing intrinsic yield and a superior security profile, as it functions as a regulated money market fund.

The niche BUIDL aims to fill is critical. When posting collateral on centralized exchanges, investors are presented with two options: stablecoins that yield no interest or volatile majors like Ethereum or Bitcoin.

Since BUIDL is less volatile and provides an annual income of around 4.5%, exchanges can set lower minimum collateral requirements, allowing institutional traders to free up more capital for other uses.

JPMorgan

JPMorgan has taken a leading role among global banks in integrating blockchain and stablecoin-like technologies into its core payment and settlement infrastructure, with the first initiative, the JPM Coin, launched as early as 2019.

As of April 2025, JPMorgan's blockchain division, Kinexys, now also handles euros and British pounds. The platform has processed over $1.5 trillion in total transactions across various services, including payments, intraday repo, collateral management, and others.

Moreover, via Kinexys, JPMorgan has announced a pilot program for a stablecoin variant called the Deposit Token, which, according to their website, is an electronic payment instrument issued by a bank that represents funds deposited by a customer.

It’s essential to note that all the aforementioned offerings are available only to institutional clients.

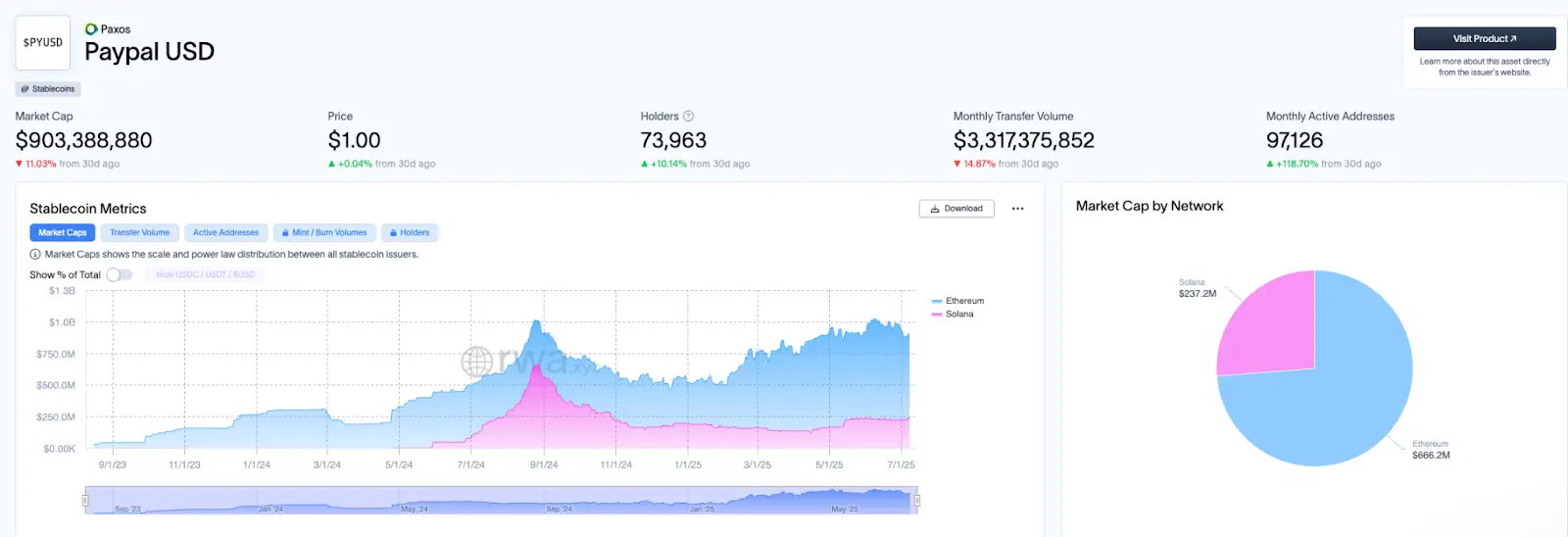

PayPal’s PYUSD

It wouldn’t be a true competition without PayPal involved. As a global leader in money transfers, PayPal boasts over 430 million users and holds a 45% market share of the worldwide payments market.

Launched back in 2023, PYUSD is issued by Paxos Trust Company and is fully backed by US dollar deposits, US Treasuries, and similar cash equivalents. PYUSD was created to facilitate seamless, 24/7 digital payments and settlements for merchants and users on PayPal’s platform.

Unlike BUIDL, PYUSD is openly available to retail investors beyond the PayPal ecosystem on blockchains like Solana, Ethereum, and Berachain, linking PayPal’s broad payment network with the expanding on-chain ecosystem.

Stripe

While not having its own stablecoin outright, Stripe has made significant progress in the space. The recent $1.1 billion acquisition of Bridge, a leading stablecoin orchestration platform, played a key role in expanding the already user- and business-friendly service.

With Bridge under its belt, Stripe launched Stablecoin Financial Accounts, targeting businesses in countries with volatile currencies to enable them to hold dollar-stablecoins.

These organizations can receive funds in cryptocurrency or via bank transfers and make payments globally using stablecoins.

Although Stripe technically has its own stablecoin due to acquiring Bridge and its USDB, it functions as a "closed-loop" currency, meaning it isn't available for public retail transactions but is meant solely for use within Stripe’s ecosystem and its business clients.

Mastercard

Now, we come to arguably the most important companies in global finance. It doesn’t matter which bank you use or at which coffee shop you’re buying an overpriced caramel macchiato sugar bomb; you'll see two names everywhere: Visa and Mastercard.

With both companies' logos visible on credit card machines and debit cards in more than 200 countries, they stand as the final domino to topple in the race for stablecoin supremacy.

Believe it or not, MasterCard already has a strong presence in the space. On June 23, 2025, MasterCard announced that it’s integrating multiple regulated stablecoins — including USDG (via Paxos), PYUSD (via PayPal), FIUSD (via Fiserv), and USDC (via Circle) — across its global payments network.

In the above blog post, they mention three core pillars where stablecoins are especially useful: enabling fast and seamless cross-border payments through Mastercard Move, offering consumers a flexible way to spend both fiat and stablecoin balances via Mastercard One Credential, and powering programmable payments and B2B settlements with the Mastercard Multi-Token Network (MTN).

MasterCard's adoption of stablecoins is progressing steadily, and Visa is also making significant strides.

Visa

To date, Visa has processed over $225 million in stablecoin volume through its participating clients, firmly establishing itself in the race.

Last year, Visa launched the Visa Tokenized Asset Platform (VTAP), a product designed to help financial institutions issue and manage fiat-backed tokens on blockchain networks.

The main idea is to offer a platform for banks to mint, burn, and transfer fiat-backed tokens, such as tokenized deposits and stablecoins, and to test different use cases in a sandbox environment.

In June 2025, Visa announced a pilot program in collaboration with Yellow Card, a major pan-African fintech, likely stemming from the VTAP initiative.

This program aims to streamline treasury operations and improve liquidity management. The partnership also seeks to explore integration possibilities with Visa Direct to broaden cross-border payment services.

While it's challenging to determine which company is further along in the stablecoin adoption cycle, I’ve noticed that all the crypto debit or top-up cards I’ve used featured the Visa logo.

This brings us to the on-chain world, where the competition is just as intense as on Wall Street.

On-chain stablecoin warfare

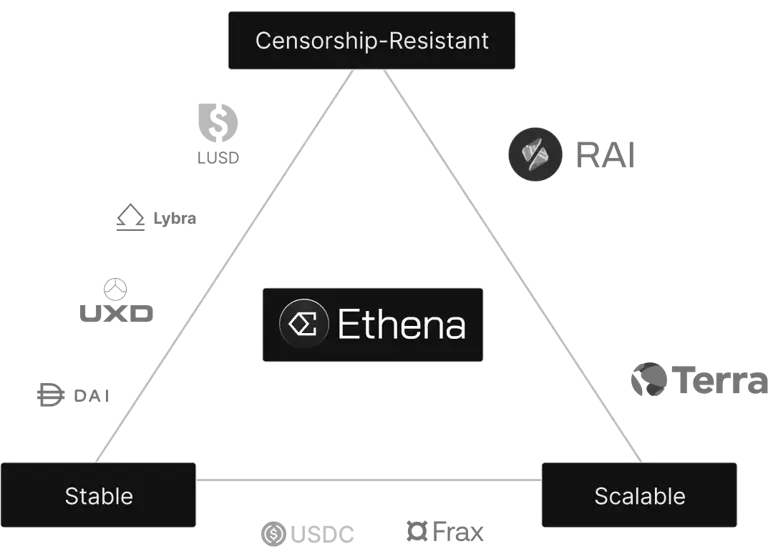

In the DeFi landscape, new entrants compete for market share by offering unique value propositions and incentives. Some provide intrinsic yields, others allow users to set interest rates, and some even introduce new layer-1 networks.

Ethena’s USDe

We’ll kick things off with Ethena, which has taken an interesting approach to maintaining the peg of its USDe stablecoin, dubbed the synthetic dollar.

Unlike its on-chain CDP cousins, USDe employs a delta-neutral strategy that involves liquid staking tokens (LSTs) and short ETH perpetual futures positions on centralized exchanges.

This setup enables USDe to remain pegged to the US dollar without direct fiat backing or over-collateralization.

A major benefit of this model is that it produces real on-chain yield, enhancing users' capital efficiency. Staked ETH earns rewards, while short perp positions usually receive funding rate payments.

These revenue streams are directed into sUSDe, a staked version of USDe, which allows holders to earn a yield while supporting peg stability.

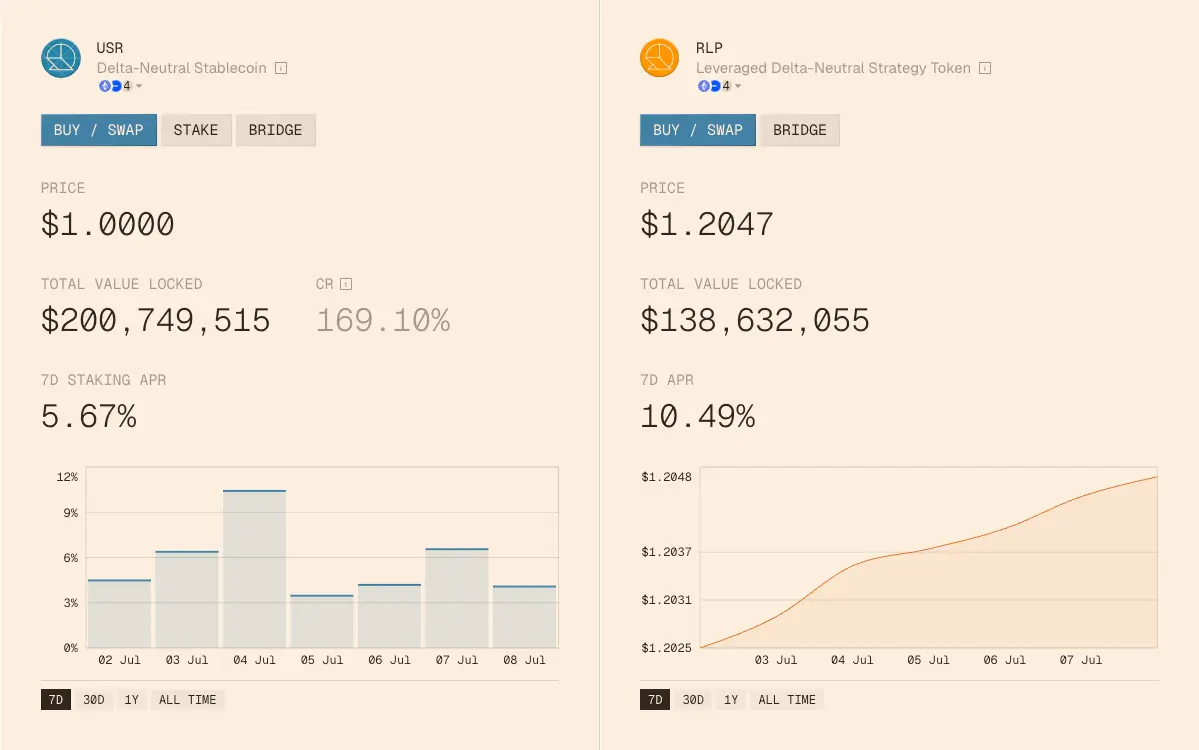

ResolvLabs’ USR

USR, ResolvLabs' stablecoin, functions similarly to Ethena. It is backed by on-chain crypto assets such as Ethereum (ETH), Bitcoin (BTC), and their derivatives like staked ETH. Like Ethena, USR preserves its peg using delta-neutral strategies and collateral backing.

However, the similarities end here, as ResolvLabs has opted to use a distinct reserve pool called the Resolv Liquidity Pool (RLP), which serves as the protocol’s insurance fund.

RLP assumes the risks associated with the delta-neutral strategy, providing a scalable protection layer for the USR stablecoin. In exchange, RLP provides attractive returns by utilizing embedded leverage.

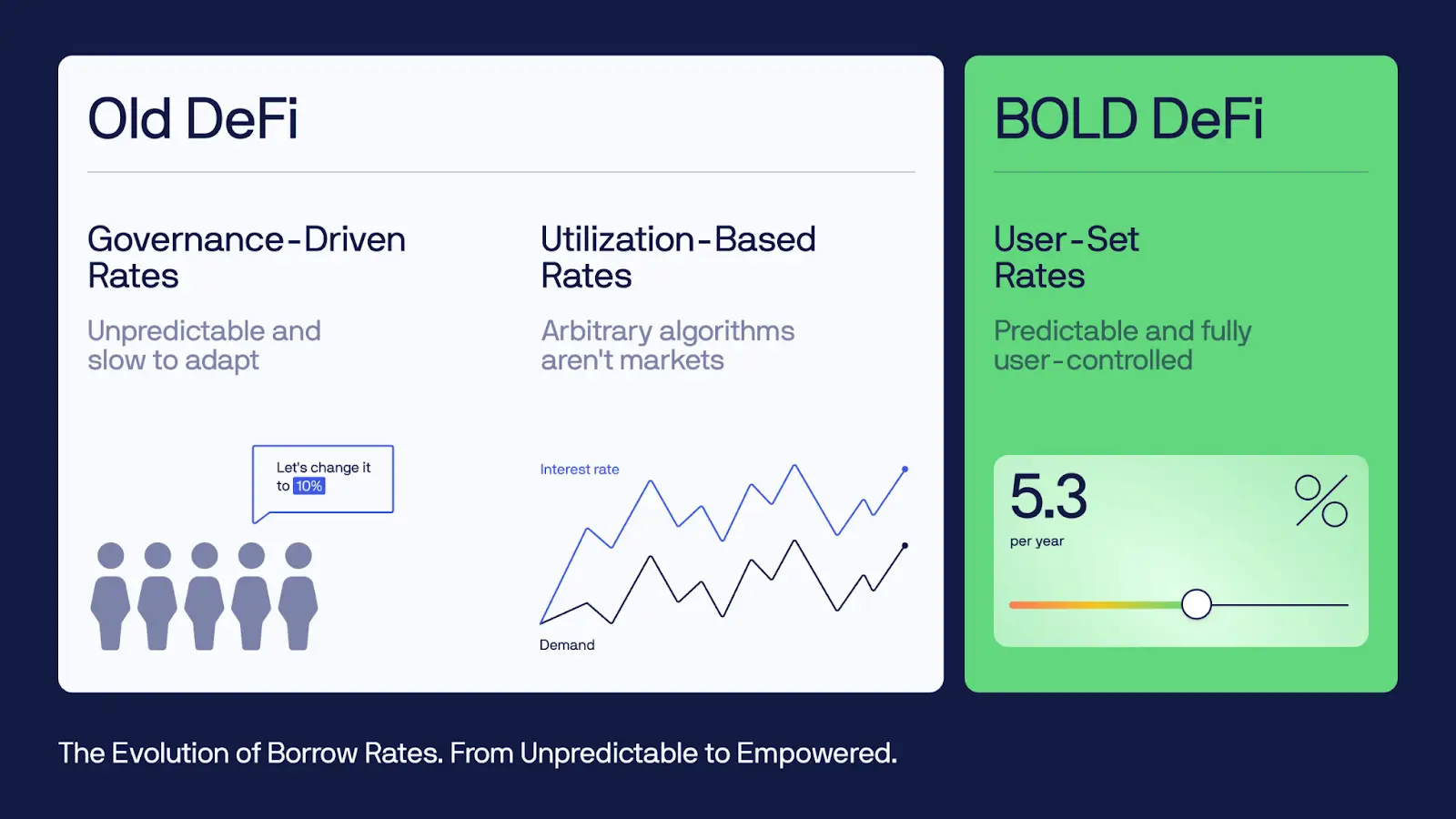

Liquity’s BOLD

The BOLD stablecoin is a decentralized, over-collateralized stablecoin that offers unique features like user-defined interest rates and greater flexibility.

Liquity uses LSTs as collateral, and the system ensures that the dollar value of collateral always exceeds the value of issued BOLD, maintaining over-collateralization.

Liquity V2 allows borrowers to choose their own interest rates for loans, giving them the flexibility to select and update rates they are comfortable with. These rates are based on their individual risk preferences, independent of governance decisions or automated adjustments.

It's clear that people continue to find new ways to optimize every aspect of DeFi, including stablecoins. The relentless desire of VCs to launch new chains also remains a constant.

Stablechains

Although I don't see why retail users would need a separate chain for daily transactions and payments, it makes sense for institutions, where most of the money is.

The company behind Tether, Bitfinex, clearly recognizes this, having invested in two projects this year dedicated to developing a blockchain that aims to offer the cheapest and fastest way to transfer stablecoins.

Currently, Tron dominates USDT flows, processing $5.4 trillion in 2024 and hosting over 69% of USDT activity. You may wonder, “Why do we need more chains if Tron has proven to be a more than viable option for stablecoin activity?” Well, let’s dig in.

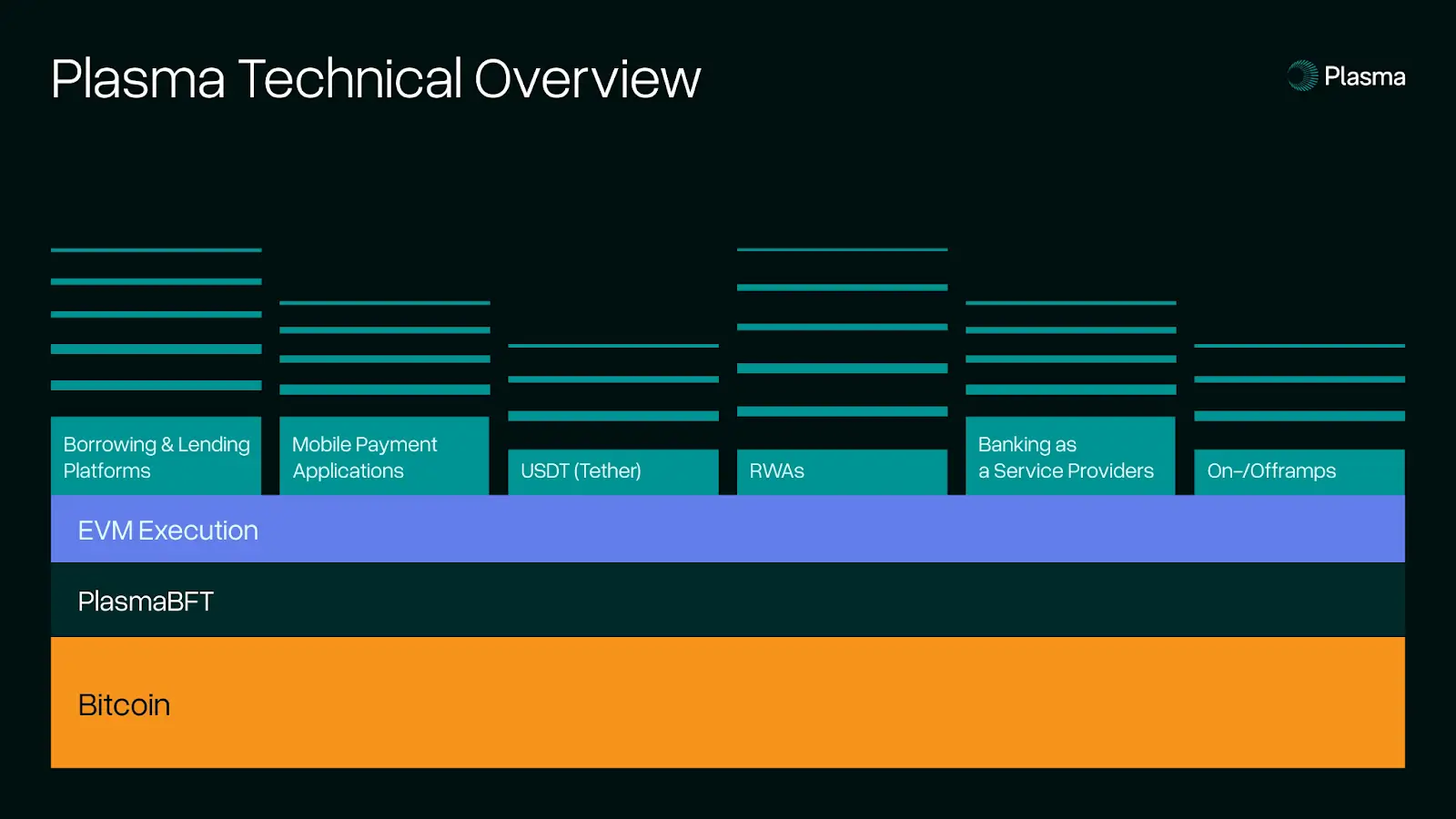

Plasma

Plasma, backed by Bitfinex, argues that there is still room for improvement and aims to become the canonical stablecoin settlement layer. Initially, the chain will launch with USDT as the main stablecoin, but the company seeks to integrate other options such as Ethena’s USDe.

Plasma offers zero-fee USDT transfers, allows paying fees in stablecoins, supports thousands of TPS, provides Bitcoin-backed security, and is fully EVM-compatible.

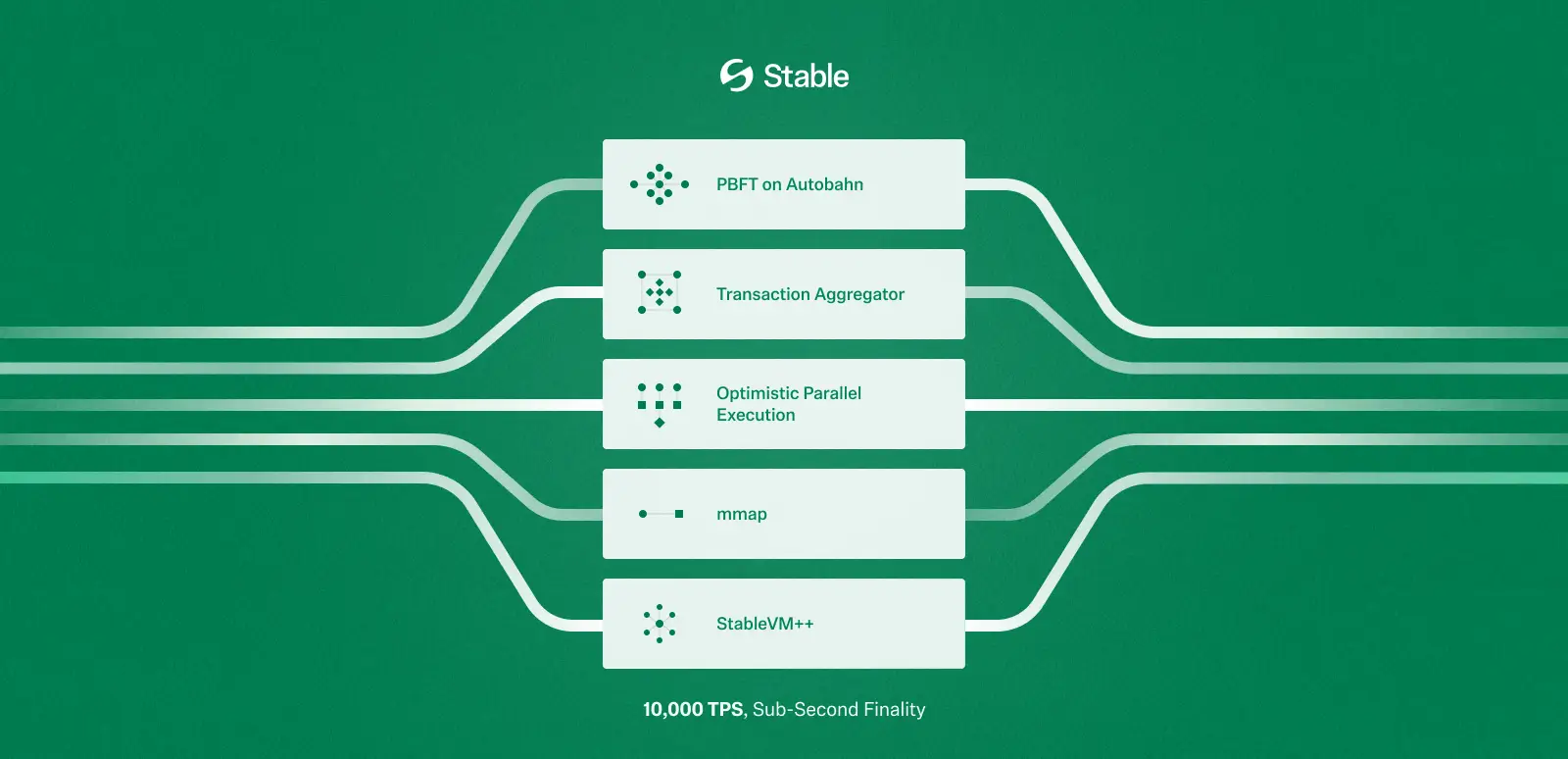

Stable

Stable is another Bitfinex-backed chain that recently obtained funding in June. Like Plasma, Stable operates as a layer-2 network on Bitcoin.

Both platforms appear to target the same market — namely, institutions — and offer similar features, with only slight differences, including zero-fee USDT transfers, USDT as a gas token, and EVM compatibility.

Although both mention that retail users will be able to use these chains for payments and transfers, it’s clear that their primary focus is on developing solutions for institutions.

Both projects explicitly state in their documentation that they will provide private transactions designed for institutional regulatory compliance, with Stable also mentioning the provision of dedicated blockspace for institutions.

Codex

Akin to Plasma and Stable, Codex, a stablechain that launched mainnet in June, is focusing most of its efforts on enterprise solutions. However, Codex has a few tricks up its sleeve that are distinct from both.

Codex delivers enterprise-grade stablecoin solutions through Codex Avenue, enabling instant fiat-to-stablecoin and stablecoin-to-stablecoin swaps at wholesale rates (for example, USD to USD stablecoins near 1:1) across multiple regions, currently in Private Alpha.

Its atomic off-ramps, planned for Q4 2025, incorporate compliance checks into transaction execution, ensuring that failed transactions revert to prevent stuck funds. This guarantees seamless and risk-free fiat delivery for businesses.

Final thoughts

The stablecoin ecosystem has undeniably gained remarkable momentum, with continuous funding and growing interest from industry players, Wall Street, and global markets alike.

While countless projects are emerging, the overarching trend is clear: stablecoin supply and adoption are expanding rapidly, reshaping the future of digital payments and finance.

Looking ahead, the trajectory of this space remains open to several possibilities. The dominance of major players like Tether and USDC may persist, especially if institutional-focused stablechains continue to integrate deeply with traditional finance.

Conversely, smaller, decentralized stablecoins such as Ethena could carve out a niche as censorship-resistant alternatives amid increasing global economic uncertainty.

Ultimately, the pace and shape of stablecoin growth will heavily depend on regulatory developments, particularly in the United States.

With a significant 180-degree shift in policy, projections like Citibank’s estimate of a $3.7 trillion stablecoin market capitalization by 2030 may well become reality, signaling a profound transformation in how money moves and is managed worldwide.

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)