Apart from the market being in shambles, something’s changed lately.

People aren’t flexing APYs or chasing the next farm anymore. They’re showing off debit cards.

Instead of bridging every other day, they’re loading up USDT and paying for coffee from the same wallet they stake in.

That quiet shift’s been building for a while. The new meta isn’t another L2 or restaking play. It’s neobanks.

Apps that make crypto feel like money again.

You hold stables, earn yield, and spend it anywhere Visa works. It’s simple, and that’s exactly why it’s catching on.

There are already more than 50 crypto neobanks out there, from early-stage startups to giants valued at north of $70 billion. It’s a fast-growing pack.

Let’s break down what that looks like.

What are crypto neobanks?

Neobanks aren’t new. They’ve slowly been chipping away at traditional banks over the past decade.

Revolut, Chime, N26, Monzo – all built on the same pitch: “we’ll give you everything your bank does, but faster, cheaper, and from your phone.”

They don’t hold charters or vaults full of cash. They just sit on top of licensed partners and build better UX.

That model worked. Today, more than a billion people use digital-only banks, and the market is worth hundreds of billions.

Crypto neobanks are the next version of that idea. Same clean experience, same mobile-first design, but with stablecoins instead of fiat as the base layer.

You deposit USDT or USDC, it earns yield, and you can spend it anywhere through a linked Visa or Mastercard.

Under the hood, your balance sits in smart contracts, not in a bank account that some compliance officer can freeze because you bought a meme coin last week.

The difference is ownership. With crypto neobanks, you don’t store money with them; you use money through them.

The players: Who’s building crypto neobanks right

Every startup wants to be your “one-stop financial app.” But only a few are actually shipping. Let’s talk about the frontrunners.

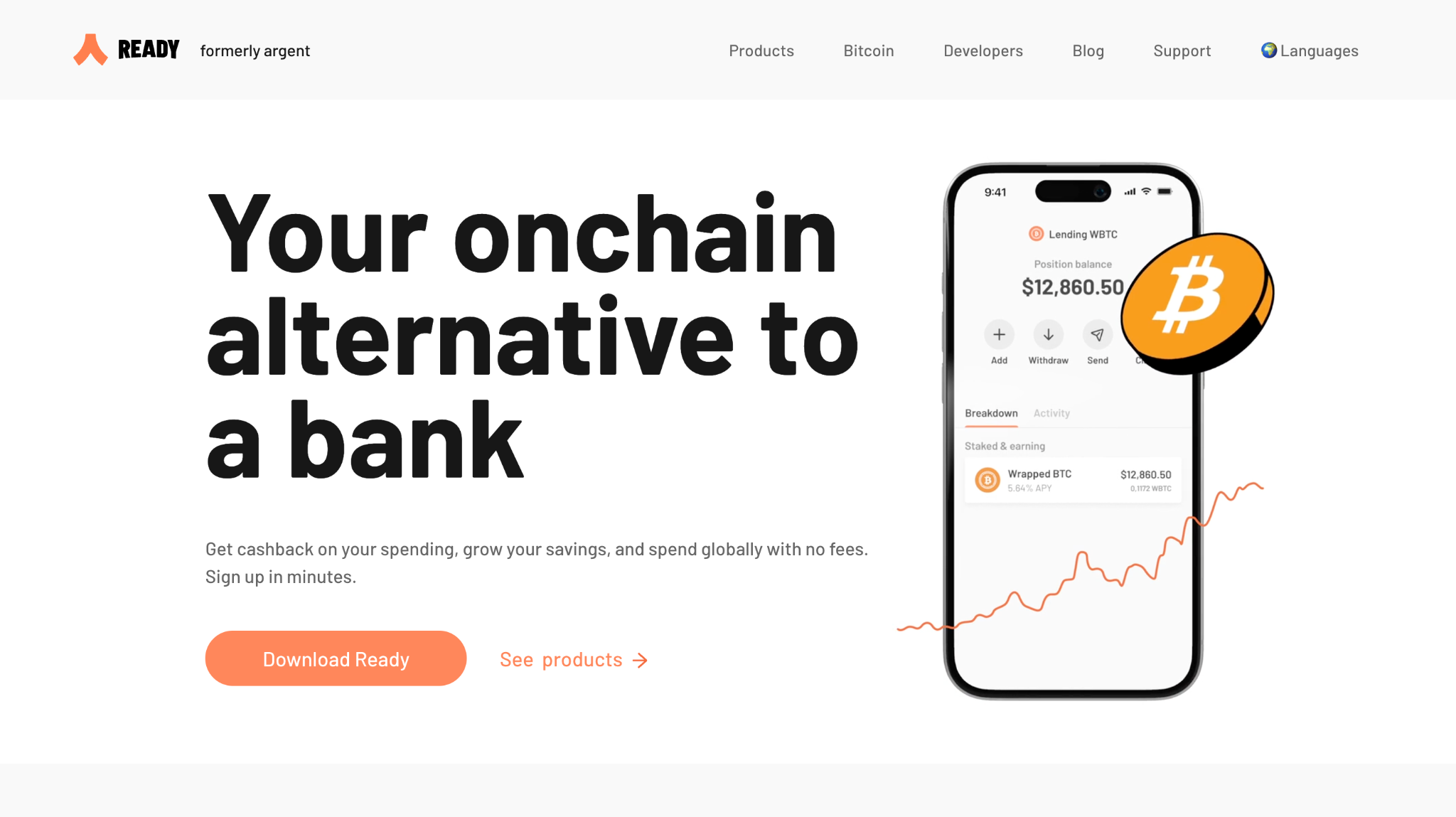

➤ Ready (Formerly Argent)

Ready is a rebrand of the former Argent wallet. With over 2 million downloads, we reckon many people familiar with crypto already have this app installed. If you don’t, here’s what it is:

Ready has clear messaging: “Spend crypto with no fees” and “Earn on Bitcoin and USDC.”

For Ready, the mission is not just to deliver a wallet experience, but to make users feel like they are using a bank app, only this time, it's onchain.

Users enjoy 0.5-10% cashbacks, exclusive discounts, and zero foreign exchange fees on their everyday spending using Ready’s crypto debit card, categorized into “Ready Metal and Ready Lite”.

Besides being able to add funds to your Ready wallet via bank transfer, the security features, such as fraud protection, 2FA, no seed phrases, and 100% self-custody, make Ready a really solid neobanking product.

➤ Tria

Tria runs on Arbitrum and feels like a DeFi-native Revolut. It’s self-custodial, multi-chain, and supports gasless transactions.

Users can earn up to 16% APY on USDC through integrated strategies, then spend directly from their wallet via Visa. No bridging, no approvals, no off-ramps. It’s all on-chain but feels like web2.

Its reward multipliers and global ramp coverage (100+ countries) make it particularly strong for emerging markets, where yield + payments is a life upgrade, not a feature.

Tria also recently closed a $12 million pre-seed and strategic funding round.

➤ Plasma One

Plasma One is built around a simple thesis: stablecoins should work like real money. You deposit $USDT, earn 10%+, and spend directly from that balance.

It’s built on a network with deep liquidity and tight ties to Tether, meaning transfers are instant and free.

You can send USDT globally, spend it through Visa rails, and withdraw it without ever touching a centralized exchange.

Plasma’s edge is vertical integration. It doesn’t just plug into someone else’s rails but owns them.

That keeps fees near zero and control in-house, a big deal in a market where third-party dependence usually kills margins.

➤ EtherFi

EtherFi started out as a restaking protocol. Now it’s turning into something closer to a full-fledged digital bank.

It already holds over $10 billion in TVL, offers auto-compounding vaults, and is rolling out Visa cards with 3% cashback.

Soon, users will even have access to IBANs and SWIFT – meaning you could, in theory, run your entire finances through EtherFi without ever touching a legacy bank.

They’re also layering in perks through The Club – a membership program with boosted rewards, partner discounts, and higher cashback tiers.

It’s basically DeFi yield farming, disguised as a credit card rewards system.

➤ MetaMask Card

MetaMask’s been the wallet of choice for most of crypto for years, but it’s always stopped at the edge of real-world use.

You could hold and swap anything, but you couldn’t spend it. That gap is now finally closing.

The MetaMask Card lets users spend straight from their wallet anywhere Mastercard is accepted.

You pick a token, tap your card, and it settles from your wallet in real time.

The key is control. Funds stay in your wallet until you pay. There’s no middle account holding your balance or freezing it because compliance got nervous.

It’s a small step on paper, but a big one for usability. They also clearly didn’t want to miss the stablecoin wars, so they dropped MetaMask USD last month.

➤ Galaxy One

Galaxy One takes the opposite route. It’s the neobank built by Galaxy Digital, the firm that already plays by Wall Street’s rules.

It brings cash, crypto, and equities into one account, offering up to 8% on idle balances.

Everything sits under FDIC and SIPC protection, so users get TradFi safety with crypto-level access.

The product feels closer to a modern brokerage than a DeFi wallet, but it gives users the same ability to move between stables, BTC, and ETFs without leaving the app.

Where MetaMask makes crypto spendable for the onchain crowd, Galaxy One is packaging it for everyone else.

➤ Avici

Thought Solana would be missing out on the neobank wave? Yeah, that’s not happening.

Avici is aiming to be Solana’s answer to a full crypto-native neobank.

It’s already live in public beta, logging $1.2 million+ in Visa card spend and around 4,000 active users.

The app supports fiat deposits, stablecoin conversions, and self-custodial wallets, so you keep control while spending anywhere Visa is accepted.

They’re building local payment rails, onchain credit lines, and real-time stablecoin settlement, all running on Solana’s low-fee infrastructure.

The project’s IDO through MetaDAO is already oversubscribed, with $3.2 million committed on a $2 million target.

That momentum hints there’s real demand for a faster, cheaper banking layer that works across borders.

➤ UR (by Mantle)

Next comes UR, Mantle’s Swiss-regulated neobank.

While everyone else is sprinting toward yield and flashy cards, UR’s playing the long game with compliance, licensing, and distribution.

It’s backed by Mantle and integrated directly with Bybit, giving it immediate reach across Asia’s fastest-growing crypto markets.

UR accounts come with Swiss IBANs in USD, EUR, RMB, and CHF. You can send money globally via SWIFT, SEPA, or SIC, and spend through a Mastercard linked to your crypto balance.

On top of that, UR offers a 5%–6% yield on USDe deposits through its partnership with Ethena.

It’s currently in private access, but early users are already calling it one of the smoothest crypto–fiat bridges they’ve used.

➤ Payy

Payy focuses on the moment money actually moves between people. While other neobank products are built around cards, balances, and yields, Payy starts with peer-to-peer transfers as the primary use case.

Instead of forcing users into a wallet interface to complete a transaction, the payment follows the conversation. You share a link directly on WhatsApp, Telegram, or wherever you are already chatting, and the other person receives the stablecoins instantly. It removes the disconnect between talking about money and sending it.

Privacy is another clear differentiator. The transaction is proven onchain, but the details remain private, so sending money does not create a permanent public trail of who paid whom.

Funds remain fully user-controlled on the device, which avoids the risk of accounts being halted or intermediaries stepping in.

The card even lights up when you pay.

➤ VPay

VPay takes a different route from most neobanks by building automation directly into the banking stack. It’s built on Base and gives users offshore USD accounts, instant Visa cards, and onchain swaps handled by AI agents.

The app already counts 5,000 users and integrates partners like Ethy, Gloria, and Flyte, letting users trade, book travel, or manage funds inside one system. It’s part of the Virtuals Protocol, which powers the upcoming x402 standard for AI micropayments.

The token, $VPAY, has a fixed 1B supply and a $7.1 million FDV, with staking unlocking free cards, cashback, and fee waivers. It’s a small-cap play with a working product, not a concept deck.

x402’s been all over CT lately, and VPay has already been building around it. Could end up being one of the smarter bets in the mix.

➤Karma Wallet

Karma Pay brings stablecoin-first payments into a regulated banking wrapper. Users access real IBANs and routing numbers, hold fiat and crypto side-by-side, and spend via a card that settles in stablecoins.

What sets it apart: transactions trigger onchain smart contract flows that allocate fees instantly toward token burns, buybacks, and community directives. The system treats the payments stack as both the product and the protocol.

No separate yield layer or side-offer gimmicks. The value escalates via usage. Every card swipe or transfer directly increases onchain activity, which in turn reduces supply and raises protocol utility.

It’s currently available across 220+ countries and supports 50+ tokens.

The macro tailwind: Why now?

This wave was coming either way. Neobanks have already taken over traditional banking.

More than 1.3 billion people use them today, and the market is expected to step into the trillions territory over the next few years.

People just want banking that works on their phones.

Crypto is now stepping into that lane, and it brings something fintech never had: programmable money.

Stablecoins are becoming the new global dollar. They move instantly, earn yield, and after the GENIUS Act passed earlier this year, they’re now recognized as legitimate digital dollars.

That changed everything. What used to live in a gray zone is now fair game for payroll, remittances, and savings.

The strongest signal of this shift is coming from Latin America.

People there use crypto because they have to.

- Inflation in Argentina is around 178%.

- Banking fees take up 4% of Brazil’s GDP.

- Over 120 million people are unbanked, but 80% own smartphones.

That’s the real market. They’re not buying stablecoins to speculate. They’re using them to survive.

When you can hold USDT, earn a bit of yield, and spend it directly without touching a bank, you’ve already solved the hardest part.

Neobanks built on crypto rails make that possible. Regulation is finally clear, stablecoins are everywhere, and the demand couldn’t be louder.

Closing thoughts on crypto neobanks

Money that you can use, that was what crypto was supposed to be. And neobanks might finally be the path to get there.

People just want to get paid, save, and spend without fighting a bank or begging an off-ramp to work.

That’s what these new neobanks are building toward: real products, real users, and an actual reason to hold stablecoins beyond speculation.

Not all of them will make it. Some will blow up, some will fade, and a few will quietly keep building until one day they’re just normal.

And when they do, it won’t feel like “using crypto.” It’ll just feel like using money. That’s when you’ll know we’ve won.

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)