Ape-tizers:

- Pyth has launched a treasury that uses protocol revenue to buy PYTH on the open market

- Pyth’s institutional product amassed $1 million ARR just one month after launch

- PYTH commands a 60% market share in DeFi derivatives based on Total Traded Volume (TTV)

In crypto, oracles are the silent vessels of truth. Without them, each blockchain and product would have wildly different prices at any given time, making the whole system more like a bazaar than a proper financial market.

With DeFi proving to be a successful testing ground for oracles, Pyth has its sights set on a much larger goal: connecting the entire financial system and greatly improving the outdated method of price data delivery, disrupting a $50 billion industry in the process.

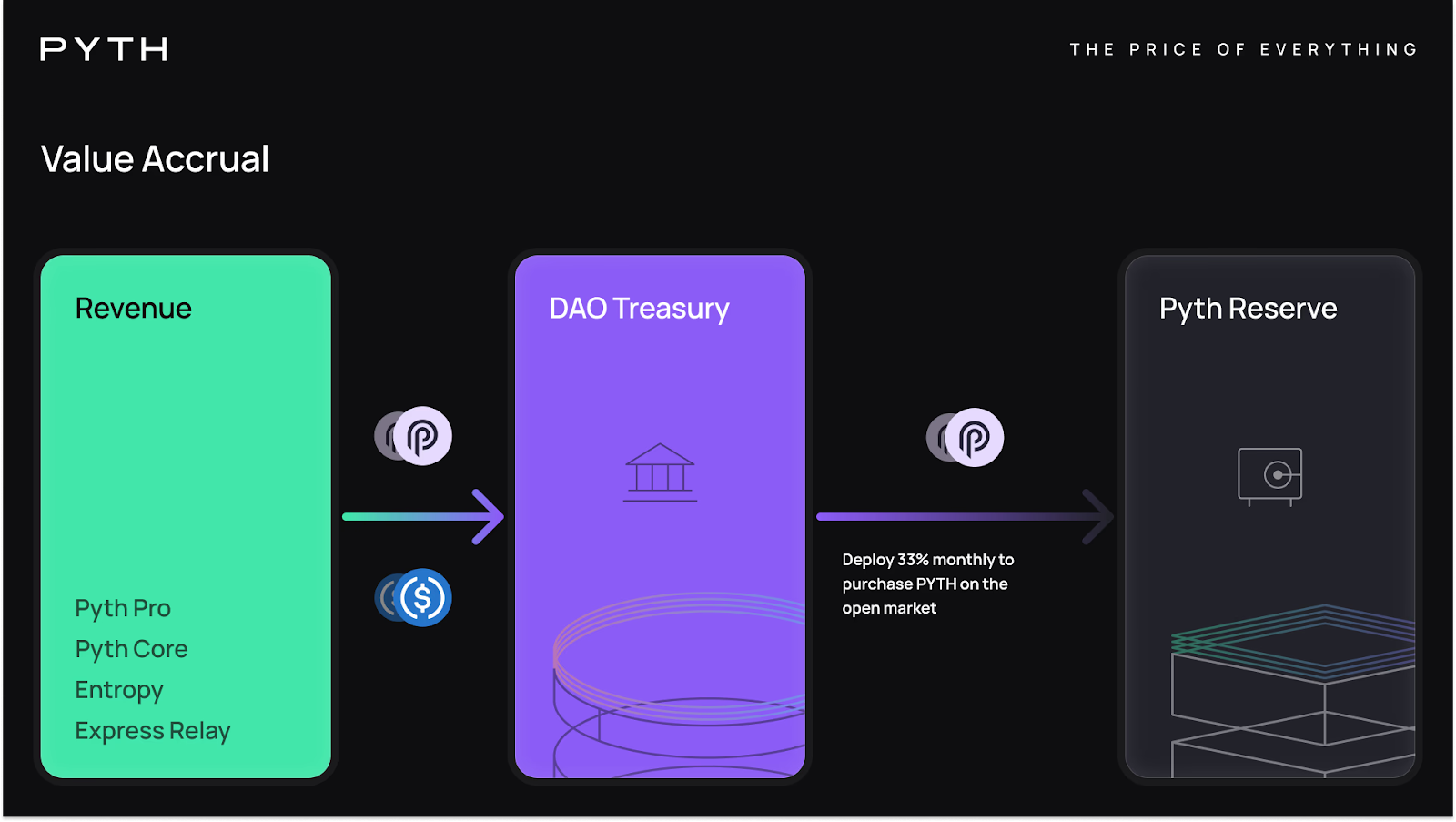

Alongside that, Pyth just introduced its largest tokenomics upgrade yet: The PYTH Reserve, with monthly purchases enhancing the token's value accrual.

The number talk

In our previous article, we examined how PYTH provides accurate and verifiable price data through its sub-second data propagation, pull setup, and the role of Pythnet in powering these functions.

The purpose of this piece is to examine PYTH's current standing and explore its future outlook as the protocol enters its next phase.

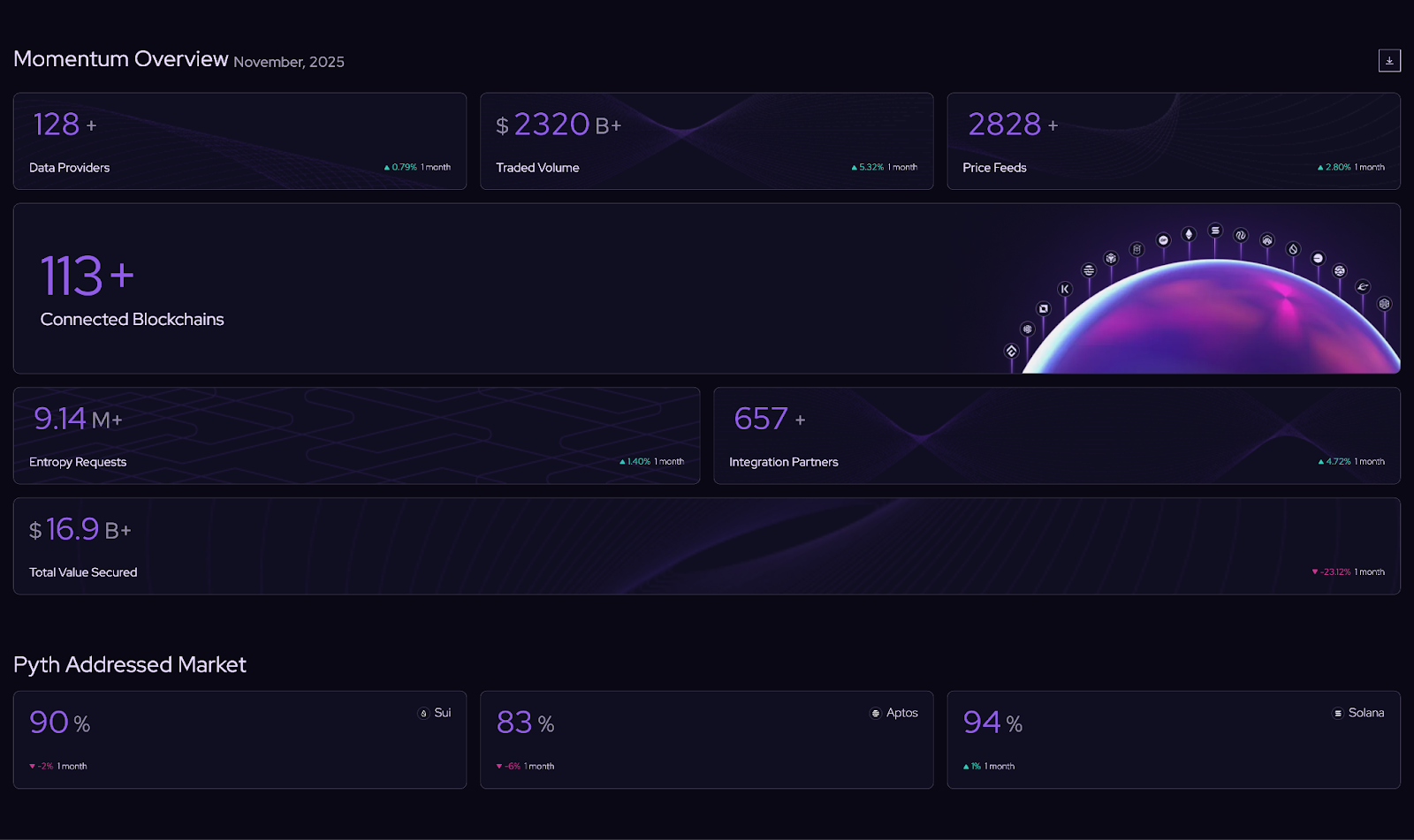

Today, PYTH provides over 2,500 price feeds to more than 100 chains across 11 asset classes, including crypto, equities, commodities, prediction markets, FX, and others, with an update frequency of up to 1ms.

Thanks to its cost-effective pull-oracle setup, derivatives products, especially perp DEXs, are Pyth’s main customers, accounting for 99% of traded volume and totalling $103 billion in December 2025.

Pyth has been actively growing its presence in the TradFi sector as well, most notably through its partnership with the US Department of Commerce to digitize economic data, beginning with quarterly GDP reports from the Bureau of Economic Analysis.

Recently, they also partnered with Kalshi, a prominent prediction market platform, and MembersCap to enable high-yield, uncorrelated RWAs onchain via the Tokenized Global Reinsurance Income Fund (TGRIF).

On DefiLlama, Pyth currently ranks fifth in Total Value Secured (TVS), which represents the amount of dollars “secured” by summing the TVL of each protocol that uses that oracle as its primary price source.

A metric that was effective five years ago, when DeFi was just starting, but it does not account for the actual activity or transaction volume that the oracle supports.

As trading activity increasingly shifts away from CEXs and toward their decentralized counterparts, Total Transaction Volume (TTV) stands out as arguably a better way to convey the value an oracle provides.

In this context, 60% of derivatives protocols depend on Pyth Price Feeds, and in most months of 2025, the Total Trading Volume (TTV) surpassed $100 billion.

This establishes Pyth as the leader based on the total transaction volume it handles, rather than the amount of idle capital it “secures” in money markets.

Moreover, since oracles primarily generate revenue from the volume of calls they handle rather than the assets they secure, processing more calls yields higher income, further highlighting the somewhat hand-wavy nature of the TVS metric.

Speaking of revenue, let’s address the elephant in the room - The PYTH Reserve.

PYTH Reserve

Up until this point, the PYTH token served two purposes: governance voting and Oracle Integrity Staking (OIS).

The governance part gave PYTH holders onchain voting power in the Pyth DAO, allowing voters to decide on:

- Reward structures for data providers

- Oracle fee sizes, denominations, and continuation

- Listed data feeds and publisher approvals

- Onchain program updates

As for OIS, it is a mechanism intended to safeguard the network against malicious or faulty data, where PYTH stakers delegate tokens to publisher pools and receive annual rewards capped at a DAO-set 10% rate.

Even with Dual-Purpose Staking, where tokens can be staked simultaneously for both governance and OIS, allowing holders to participate in voting while earning security rewards, this remained an unappealing value proposition, as staking only offsets the dilution caused by token emissions.

With the introduction of the PYTH reserve, this changes.

This milestone ensures that all revenue from PYTH products, i.e., Core, Entropy, Express Relay, and Pro, will now be directed entirely to the DAO-managed Treasury.

Each month, the DAO will deploy one-third of its treasury balance to acquire PYTH tokens on the open market, directly linking the protocol's success to its token.

Furthermore, to stay competitive, the Pythian Council will conduct quarterly pricing reviews across the onchain product suite: Pyth Core, Entropy, and Express Relay. This will make the protocol more agile and competitive, hopefully increasing revenue even more.

However, with current revenue figures from all but one of Pyth’s products being notable, the stakes are high for Pyth Pro and its steward, Douro Labs, to deliver.

But the initial signs for Pyth Pro are highly promising: the company already hit $1 million in annual recurring revenue (ARR) in its first month, and the team projects it will grow to $50 million in ARR within 12–18 months.

Pyth Pro: Disrupting the $50 billion financial data market

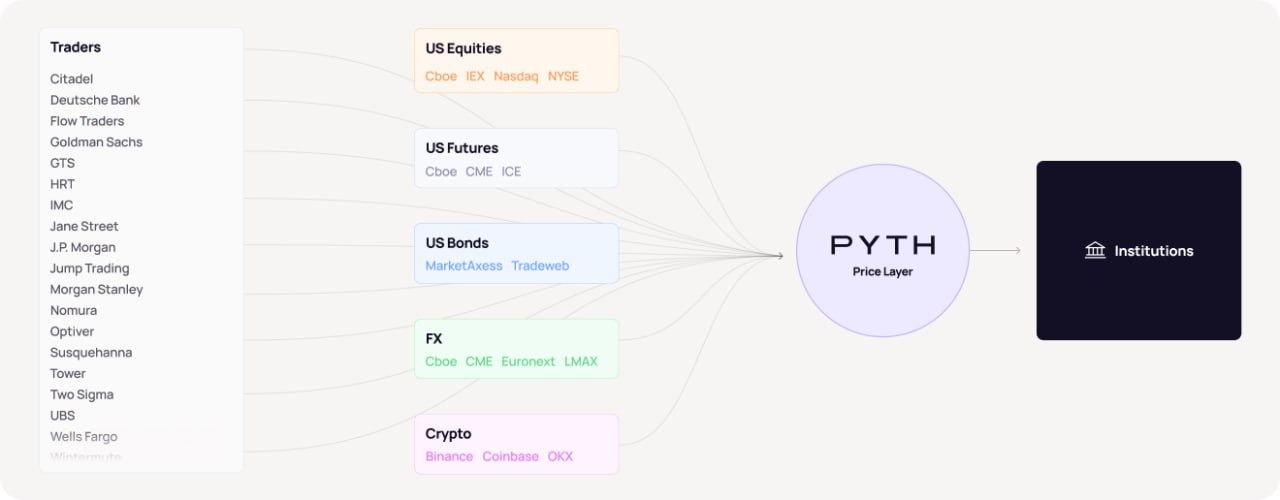

Pyth Pro is an innovative subscription service designed to transform institutional access to market data across various asset classes, including crypto and equities.

Built in collaboration with Douro Labs, it serves as a strong alternative to established data resellers such as Bloomberg and Refinitiv.

With its source-driven data model, Pyth Pro enables institutions to connect directly with traders and exchanges, ensuring transparent, trusted pricing.

The service offers unified global coverage, simplifying access to comprehensive market data without the silos of traditional vendors.

The cost and transparency differential is stark: Pyth Pro charges $10,000/month for complete cross-asset coverage (2,500+ feeds spanning crypto, equities, FX, commodities), versus Bloomberg's opaque contracts exceeding $250,000/month for incomplete bundles, a >90% cost reduction that Pyth attributes to disintermediating downstream repackagers.

If Pyth Pro can capture just 1% of the $50 billion data market, this would generate $500 million annually, with 60% of that going toward the DAO (40% toward Douro Labs), leading to more than $100 million in yearly token purchases.

Road ahead

Launched in 2021, Pyth’s journey can be divided into two distinct phases.

Pyth’s first chapter focused on a single objective: developing and expanding the infrastructure to validate and distribute institutional-grade data onchain.

With more than $2.5 trillion in cumulative transaction volume, a commanding 60%+ market share in DeFi derivatives, over 600 integrations, and the publication of US Department of Commerce data, Pyth has well exceeded that goal.

Looking ahead, we know that all of finance will inevitably be deployed onchain. And it just so happens that Pyth is already ahead of the pack when it comes to pricing RWAs such as equities, commodities, FX, and more.

This is not a coincidence.

After many discussions with partners and users, the team recognized that the data Pyth possesses is highly valuable not only for blockchain applications but also for traditional finance, which depends on an outdated distribution model and legacy providers that are way too expensive.

The key moat lies in Pyth’s ability to legally distribute price feeds through first-party sourcing. Moreover, with the new administration in place, builders are now more confident than ever in launching products that utilize these price feeds.

If the institutional product, Pyth Pro, continues to chip away at the sector, it will effectively enter a clear, blue ocean, with its only competitors being the dinosaurs still plagued by analog, fragmented systems and exorbitant pricing on their services.

Even so, some questions remain, such as the token’s supply overhang and the full extent of their Pro product's ability to displace the incumbents.

Nonetheless, the institutional strategy, paired with the Reserve, sets Pyth apart from competitors, as revenue from real network usage remains largely unseen, with most depending on upfront business agreements to introduce products on new chains.

Most importantly, it shows the team's commitment to the protocol by directing the entire revenue stream to the DAO, rather than keeping it all for themselves.

And in my book, that's a huge green flag.

Ultimately, the mix of proven execution, improved tokenomics, and a massive untapped market makes Pyth one of the most promising infrastructure plays in crypto.

Thanks to the Pyth team for unlocking this article. All of our research and references are based on public information available in documents, etc., and are presented by blocmates for constructive discussion and analysis. To read more about our editorial policy and disclosures at blocmates, head here.

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)