Reading time: 5m 35s

Every cycle has its buzzwords, but every now and then, something sticks.

Today, we are looking into one of those things that we think might stick.

It is called infrastructure finance (InfraFi), or, better put, infrastructure financing.

Infrastructure finance is an offspring of the intercourse between DePIN and DeFi, a hybrid model focused on funding, tokenizing, and liquidity-enabling of real-world infrastructure projects, particularly those involving abundant, renewable resources.

In simple terms, it involves using efficient, established mechanisms onchain to finance real-world physical infrastructure and earn yield from the revenue those assets generate, through tokenization, lending, and other methods.

While this sounds simple and straightforward, we think it might be what finally makes DeFi matter to normal people.

Here’s a vivid example of an InfraFi loop, of course, broken down for your morning coffee:

- You deposit stablecoins (USDC, USDT, whatever) into a vault.

- Those funds are used to finance the purchase or deployment of physical infrastructure, including GPUs, solar panels, broadband nodes, and batteries.

- That infrastructure generates real revenue (compute fees, electricity sales, bandwidth payments).

- Revenue flows back into the vault. Depositors get their stablecoins back plus a share of the yield.

Look, if DeFi, as we know it, was basically just lending stables to farm inflationary governance tokens - we’re talking looping, vanilla staking, and all those onchain antics that had us debating "sustainability" in the group chat every two weeks...

InfraFi is the complete flip side.

You are lending stables to finance actual hardware, like solar panels, that meet a genuine energy demand. The yield comes directly from the revenue generated by selling that power.

Why is this convergence happening?

If you’ve been in crypto long enough, you’ll agree with me that the timing matters when it comes to narratives - pretty much the same way ZEC was not as conventionally popular until some bald guy decided to red-pill everyone.

For InfraFi, it’s not a bald guy; it's three macro forces colliding at the same time:

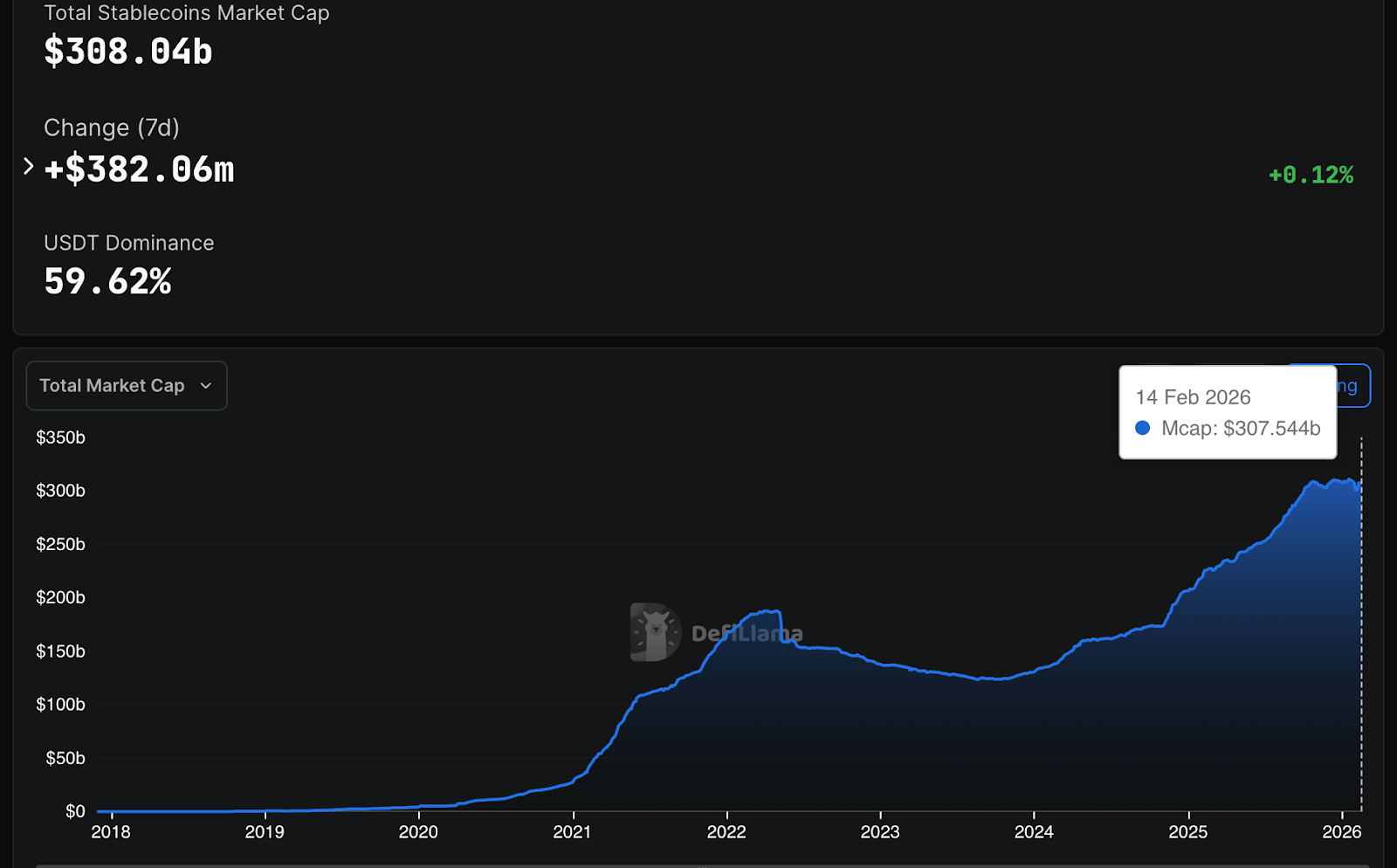

Stablecoins

The onchain stablecoin market is a $300 billion+ market. While that might be half of Elon’s net worth, it is actually not funny money.

What matters is that this is some serious dollar-denominated liquidity sitting onchain, most of it in USDT and USDC, desperately looking for yield.

With the GENIUS Act signed into law and banks integrating stablecoin rails, this number will only keep rising. The supply side of capital is basically solved.

DePIN revenue spike

Initial reports for 2025 placed DePIN revenue at $72 million despite a market cap of $10 billion, showing a significant disparity between valuation and revenue.

Since then, DePIN revenue has almost doubled, with reported revenue at $150 million across the board.

While this might still sound modest, there’s evidence that leading projects now trade at 10–25x revenue multiples, down from 1,000x+ in 2021.

DePIN revenue simply means that these products are getting real adoption, and are being used by real companies, driving real revenue rather than the arguable revenues of most crypto products.

Current projections place year-end revenue growth at $30 billion and $3.5 trillion by 2028.

Some of the companies driving this revenue are Helium, Render, Hivemapper, Akash, and Dabba. All of them are businesses with actual customers paying actual money.

The financing gulf

You don’t have to be from a third-world country to see that the likes of solar, internet, and other DePIN products are critical infrastructure in desperate need of financing for maximum reach.

Estimates are that the world needs somewhere between $10 trillion and $50 trillion in solar investment alone by 2050. That’s before you count batteries ($4–5 trillion), data centres, broadband infrastructure, robotics.

The demand side for capital is, frankly, bottomless. TradFi can’t fill this gap alone, and in the next few paragraphs, we will tell you why.

Why not just use banks?

The reality with traditional infrastructure is that something like lending takes months of due diligence, legal structuring, and negotiation.

When compared with a product like USDai that processes loans rapidly, the difference is staggering.

A solar developer with $100 million in tokenized project debt could borrow $70 million in stablecoins within minutes on Aave, then redeploy it immediately into new projects.

Moreso, access to this capital is often limited. Infrastructure funds are dominated by a handful of institutions in New York, London, and Singapore.

InfraFi opens this market to anyone with stablecoins. A retail investor in Lagos can earn yield from a solar farm in Rajasthan. If you deep it, that is something that’s never been possible before.

On the liquidity level, capital unlocks efficiently through InfraFi compared to traditional financing infrastructure.

The same dollar can finance multiple projects over time, and such capital recycling could double or triple productive capacity per dollar deployed.

Finally, DePin is structured globally, such that products can exist for specific geographical locations (Dabba in India, WiCrypt in Nigeria, as examples).

This expands further adoption of foreign-denominated revenue, naturally creating demand for alternative or foreign stablecoins besides the dollar within DeFi.

This solves one of the biggest chicken-and-egg problems for non-dollar stablecoin adoption.

On the contrary, currency adoption in the traditional scene faces stiff hurdles in cross-border use cases.

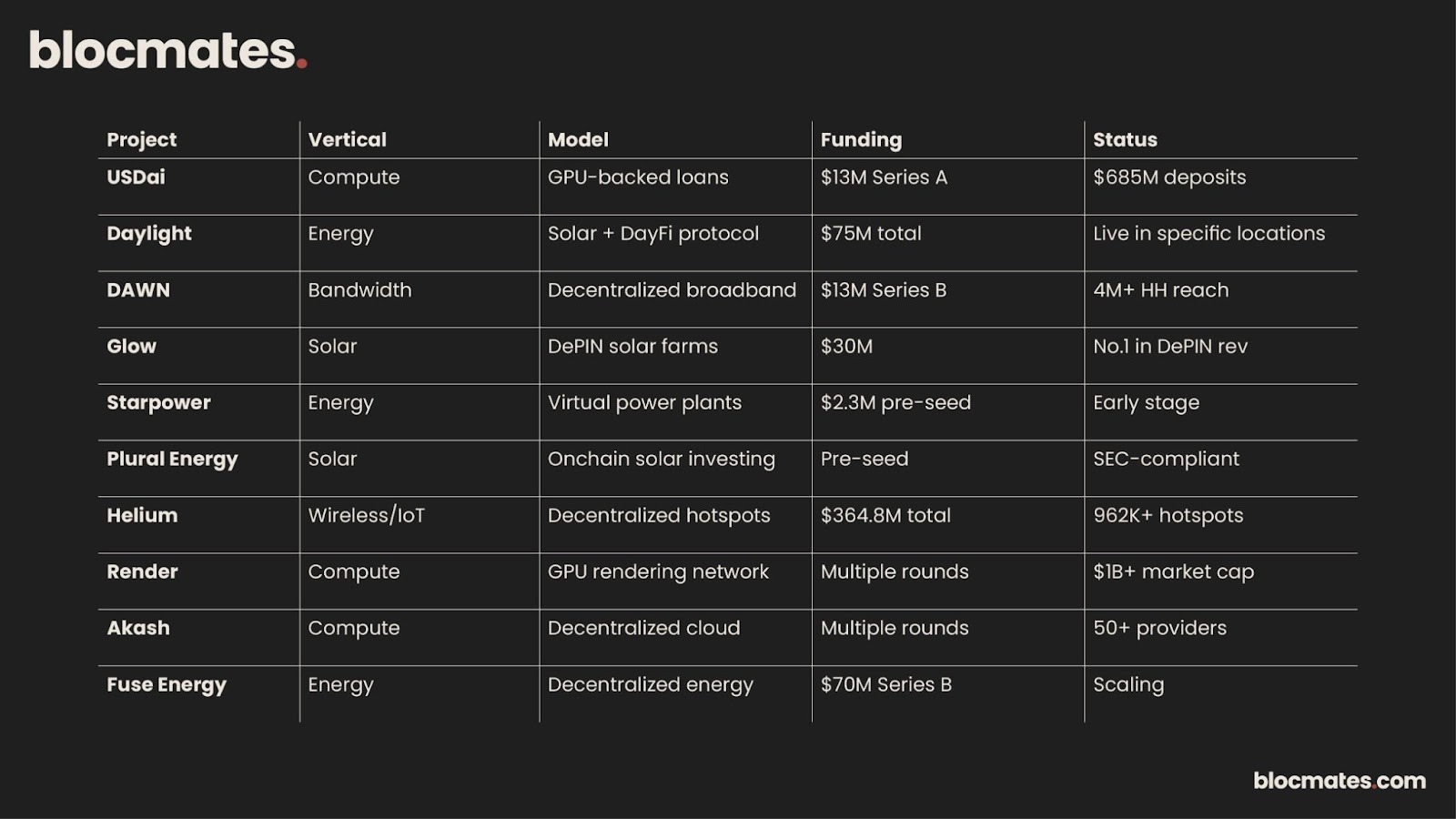

The InfraFi map

The InfraFi category is growing fast. Here’s a snapshot of players worth tracking:

Could we see Elon’s money flow into InfraFi?

Not a lot of people like to make audacious calls, but we do. So our answer is: why not?!

Let’s take a look at the facts here:

Elon Musk has arguably been the biggest solar bull on the planet since day one.

While everyone else is getting excited about nuclear fusion or whatever the current narrative is, Musk has been fading it, calling it "super dumb" for the simple reason that we have a massive fusion reactor in the sky called the Sun.

He’s done the math, and frankly, the math is undeniable. You cover a 100x100-mile patch of desert in solar panels, and you power the entire United States.

He knows it, the Chinese manufacturing sector (which is shipping 1,000 GW a year) knows it. Yet, most of the world (except China) is still stuck dealing with red tape and banking bottlenecks.

InfraFi, on the contrary, is permissionless and fast. It can fund the 100 GW/year capacity he needs for data centers without waiting for traditional banks to get their act together.

And if we know anything about Musk, we know he hates inefficiency (I mean, he headed the department of government efficiency).

Right now, US tariffs and traditional financing are artificially inflating costs and slowing down deployment.

InfraFi, on the other hand, leverages global crypto liquidity to bypass these bottlenecks. It’s democratized funding that moves at the speed of the internet, not the speed of the Federal Reserve.

Elon wants a multi-planetary future powered by the sun. InfraFi builds the financial rails to make that happen without the friction of TradFi. It turns the pro-solar rhetoric into onchain, verifiable action.

Concluding thoughts

InfraFi is DeFi growing up. It is the sector finally delivering on the promise we’ve been making since 2020, that decentralized finance can do things traditional finance can’t.

Faster capital deployment, global access, instant liquidity, and composable financial products, all crash into InfraFi.

However, it’s important to note that we are at the early stages of this - USDai has $685 million in deposits.

Daylight just raised $75 million. These are seed-stage numbers if this is truly a multi-trillion-dollar opportunity.

But that’s where the fun is, the more nascent, the better, as it allows users to align with the growth.

Considering that the early stages of crypto and DeFi were colored by a direct middle finger to the centralized structure of traditional finance, InfraFi pushes this even further.

What we now see is a new movement where decentralized capital formation becomes productive to extend into the real world, financing the things that matter and bringing the final hooks of traditional structure to its knees.

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)