Reading time: 9m 13s

Contrary to the current sentiment, we’ve made significant progress as an industry, especially in the past few years. Let’s quickly recap, shall we?

On April 20, 2023, the European Parliament approved the MiCA framework, setting rules for all digital assets, including stablecoins, within the EU.

In 2024, the launch of Bitcoin spot ETFs marked a crucial milestone, allowing institutional investors to enter the arena, further legitimizing Bitcoin's status in the world's largest economy.

Last year, the US enacted the GENIUS Act, establishing the first federal framework for stablecoins, while the CLARITY Act (hopefully) will pass this year to establish a broader market structure for digital assets.

Together, these laws replaced 'regulation-by-enforcement,' which was the status quo for the majority of this industry's existence.

By the way, remember this lovely sunshine?

What now?

On paper, digital assets had won their long battle to be recognized as something more than a multi-level marketing scheme.

Fast forward to today, and it feels like nothing has materially changed. Bitcoin is barely hovering above its previous bull-market highs, and 99% of coins are down so bad I’d rather not talk about them any further.

Underneath the surface, however, in the meetings of every bank, fintech, and fund manager, the question of digital assets is constantly being raised. Don’t believe me? Check this.

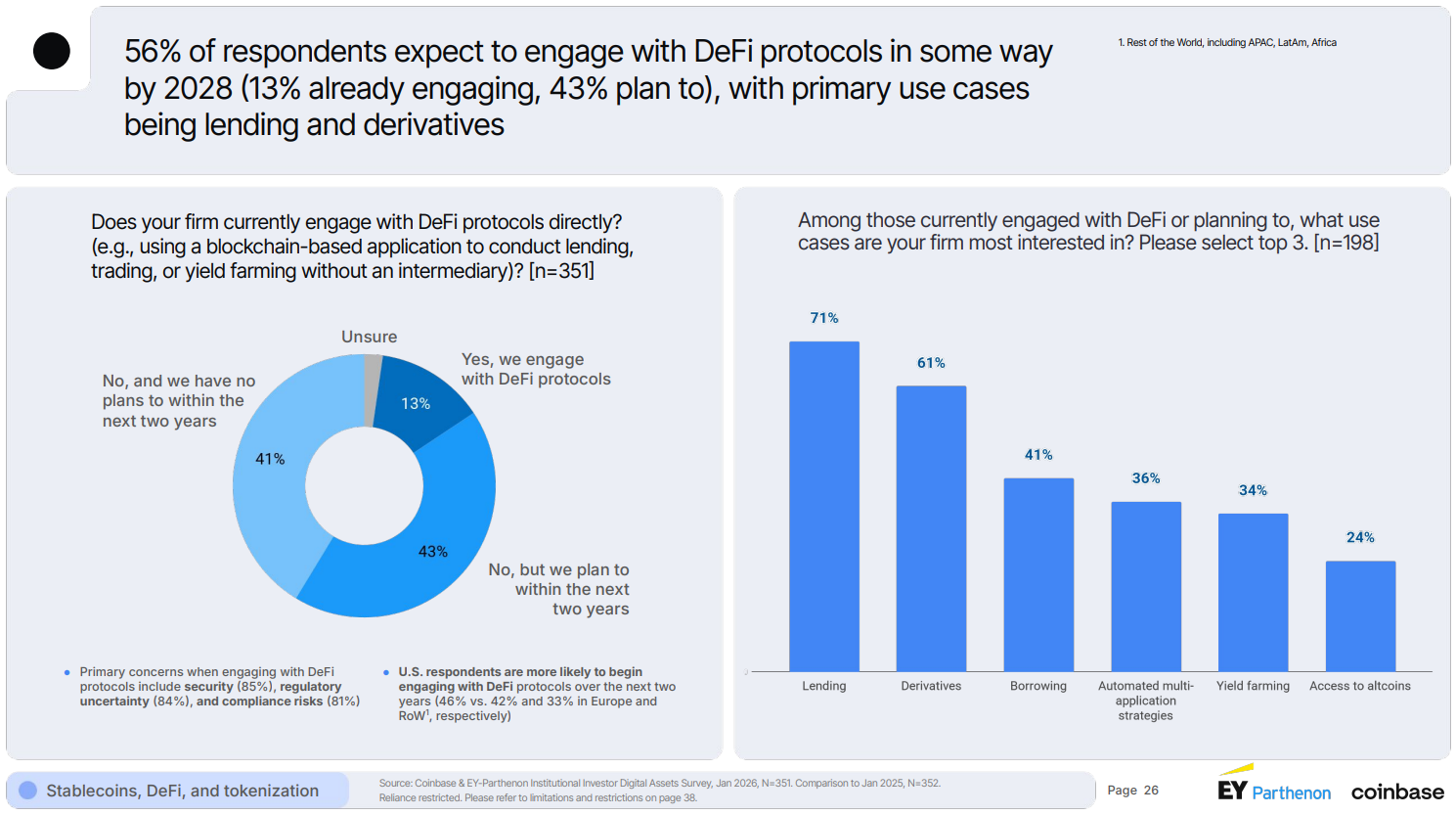

The annual EY-Parthenon and Coinbase Institutional Investor survey highlights that 73% of institutional decision-makers plan to increase allocation to digital assets in 2026, and 56% expect to engage with DeFi by 2028.

And these are not some schmuks taken from the street who still hold XRP or Carbongo, but institutional investors, including asset managers, asset owners, family offices, private banks, hedge funds, and VC firms.

While legislation remains the top concern, it has undoubtedly moved in the right direction, leaving businesses wondering how to take advantage of it. Naturally, stablecoins come to mind first.

Both MiCA and the Genius Act (in its current state) clearly state that stablecoins are to remain purely a form of payment, not an instrument for generating yield.

This means fintechs in both the US and EU can’t offer yield on USDC just like that. They have to build a separate product, route it through DeFi infrastructure, and present it as a distinct savings-like experience that mimics the TradFi setup.

You can thank the bank lobby for that.

However, integrating a DeFi yield product in-house is time-consuming, expensive, and involves multiple implementation challenges, including custody, execution, security, yield sourcing, audits, and more, leaving most to rely on multiple infrastructure providers that cover different parts of that stack.

This has led to the rise of 'Yield-as-a-Service,' a new infrastructure segment offering white-label yield products for fintechs, neobanks, and wallets that either lack the time or budget to develop these products or want to remove technical debt stemming from multiple integrations stitched together.

What is Yield-as-a-Service (YaaS)?

Yield-as-a-Service (YaaS) is an emerging category of infrastructure products that seamlessly integrate yield products into financial applications, eliminating the need to develop them in-house.

And if a product accepts stables, YaaS means those stables can generate juicy income while complying with GENIUS and MiCA restrictions.

YaaS brings the piping, execution, and sourcing of yields directly to the product's doorstep, enabling these companies to take advantage of the breadth of yields that DeFi offers.

The process is typically facilitated via APIs or SDKs, with the actual yield product surfaced to the user as a native part of the application while the underlying infrastructure remains invisible, enabling additional revenue generation and enhancing user retention.

The core addressable markets for YaaS are the fintechs, neobanks, and wallets of the world, but it can also be extended to institutional offerings and consumer apps.

Among these infrastructure providers, one stands out for its comprehensive offering, which, until recently, included same-chain and cross-chain swaps alongside bridging, and now also delivers yield.

What is LI.FI?

In case you’ve been living under a rock, perhaps too preoccupied with bridging and swapping tokens separately, LI.FI is an infrastructure provider that handles routing and execution for apps, granting them access to all onchain liquidity across chains, bridges, DEXs, solvers, and yield protocols.

Used by more than 850 partners, including Robinhood, Binance, Kraken, MetaMask, and Phantom, LI.FI has quietly become the cross-chain layer the industry runs on, facilitating over $75 billion in total transfer volume across more than 85 million transactions spanning 65+ blockchains.

Enter LI.FI Earn

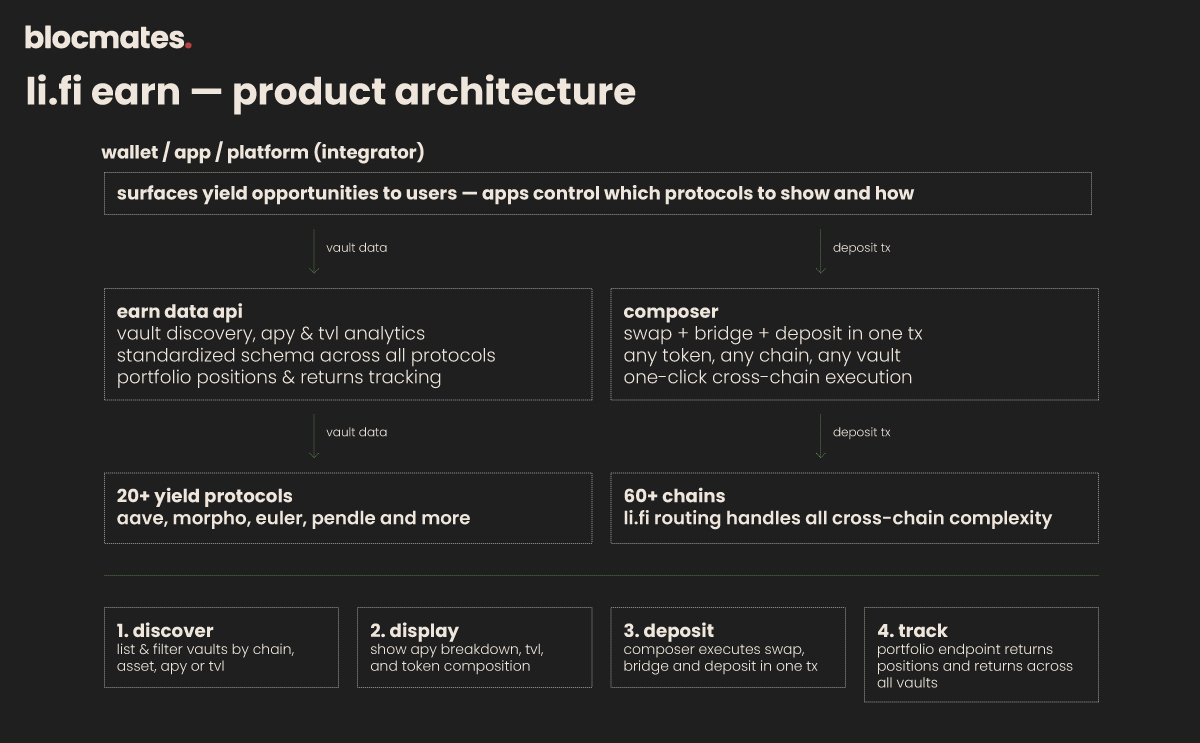

Earn is the latest addition to LI.FI's B2B product suite, building on the company’s existing API and cross-chain infrastructure.

Earn gives fintechs, neobanks, wallets, and other consumer apps the option to create yield products through a single integration, reducing the need to juggle multiple vendors.

Out of the box, Earn supports yield opportunities from 20+ protocols - Aave, Morpho, Euler, Pendle, and more - across 60+ EVM chains. For most fintechs, that's the entire addressable yield landscape handled before you've written a single line of custom integration code.

Under the surface, the product consists of two infrastructure primitives featured in LiFi’s stack: the Earn Data API, which normalizes all available vaults into structured metadata, fetches live APY and TVL, and can track user portfolios, alongside the Composer, which enables one-click deposits, cross-chain flows, and any-token-to-vault transactions.

For dashboards, portfolio trackers, and wallet interfaces, supporting execution on specific pages or sections might not be necessary. Using the Earn Data API simplifies aggregating a user’s DeFi positions across protocols without integrating each separately.

While that’s neat, the killer feature is the Composer, which comes standard for any LI.FI product, including Earn.

With Composer, LI.FI simulates and executes complex, multi-step flows across chains and assets, bundling them into a single transaction for the end user, eliminating the need to sign multiple transactions at each step.

Furthermore, given the tricky nature of DeFi, certain precautions and nice-to-haves are in place, including execution safeguards (gas estimation, slippage protection, and transaction structuring) and status tracking (completed, partial, refunded, and failed).

Important to note that the Composer currently only works for EVM chains, so the same applies to the Earn product. Rest assured that support for Solana is in the works.

If you’re curious how it works in practice, Jumper (Li.Fi’s consumer-facing app) has already integrated the Earn feature. Go ahead and check it out here.

Alright, now that we’ve established that this is the future of France for apps looking to integrate yield into their product suite, let’s actually test that theory against other YaaS competitors and see whether Earn holds up.

Mapping the YaaS landscape

Instead of a uniform sector with few differentiators, the YaaS landscape can be described as a set of distinct lanes, each addressing the same challenge from a different angle.

Privy and Dynamic

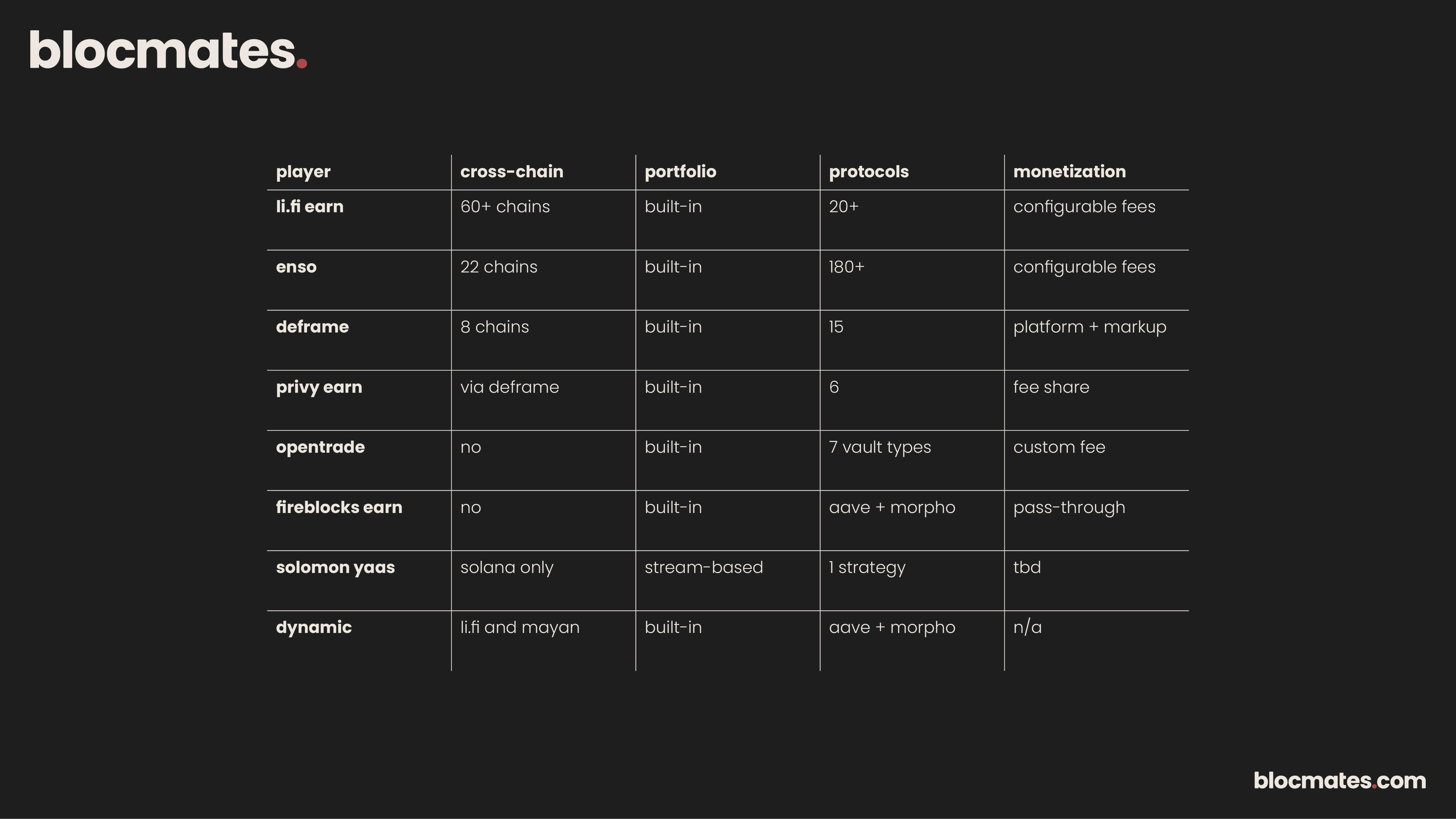

On one end, you have wallet-native solutions that bolt yield onto existing infrastructure, tapping into a few established DeFi protocols via yield recipes.

In Privy's case, that's achieved by deploying a fee wrapper contract on top of an ERC-4626 vault: user deposits flow into the wrapper rather than the underlying vault, with a configurable share of accrued yield captured as vault shares.

Dynamic partners with Aave and Morpho to bring yield directly into its wallet interface. On Aave, users supply assets directly to the protocol, whereas on Morpho, deposited assets are converted into an ERC-4626 vault managed by a curator, Sentora.

Fireblocks

Fireblocks adopts a similar strategy, but targeting institutions. Its Earn product integrates directly into its custody platform, sending idle stablecoin balances to Aave and a Sentora-curated Morpho vault (the same as for Dynamic since Fireblocks acquired the company) using the existing approval workflows and policy controls that clients are familiar with.

Deframe by Pods Finance

Rather than wrapping existing wallet infrastructure with yield capabilities, Deframe generates the raw transaction bytecode needed to interact with a DeFi protocol and returns a transaction object for the user to sign with their wallet, while the protocol-specific logic is handled under the hood.

With two integration methods, API or SDK, Deframe supports swaps, cross-chain operations (facilitated via Mayan and Symbiosis), and 13 protocols, including Aave, Compound, and Curve.

Enso

Enso goes deeper, offering access to 180+ protocols and a bundling API that can handle complex DeFi strategies, giving DeFi-native teams a broad toolkit for portfolio, balance, TVL, APY and execution use cases.

OpenTrade

On the other end, you have compliance-first providers like OpenTrade, where the unique value proposition is the legal wrapper rather than extensive DeFi access.

All loans go through OpenTrade SPC, a segregated portfolio company registered in the Cayman Islands, managed by an independent board and an FCA-regulated investment firm, with a security trustee holding collateral on behalf of lenders.

Yield products are then structured as ERC-4626 vaults across tokenized US treasuries, bonds, commercial paper, and actively managed DeFi strategies.

Solomon Labs

Solomon’s approach doesn't fit neatly into any of these lanes. Rather than providing infrastructure for fintechs, it streams yield directly to holders of its USDv stablecoin, completely eliminating the need for staking or deposit flows. It's a fundamentally different take on the problem, and one worth watching.

What's notable is that some of these products weren't built to win new customers; they were built to deepen relationships with existing ones.

For example, Privy Earn is a natural “upsell” for developers already on Privy's wallet infrastructure. The same is true for Fireblocks Earn and Dynamic, but on the institutional side.

The practical implication is straightforward: if you're not already in their ecosystem, these products weren't built for you, leaving the field open for alternatives.

This brings us to Li.FI Earn, which I believe embodies the term Yield-as-a-Service most aptly.

It's a service that brings you yield, period. Not a legal team, not a recipe from which you have to stitch together a product, not an accompanying wallet infra, simply yield.

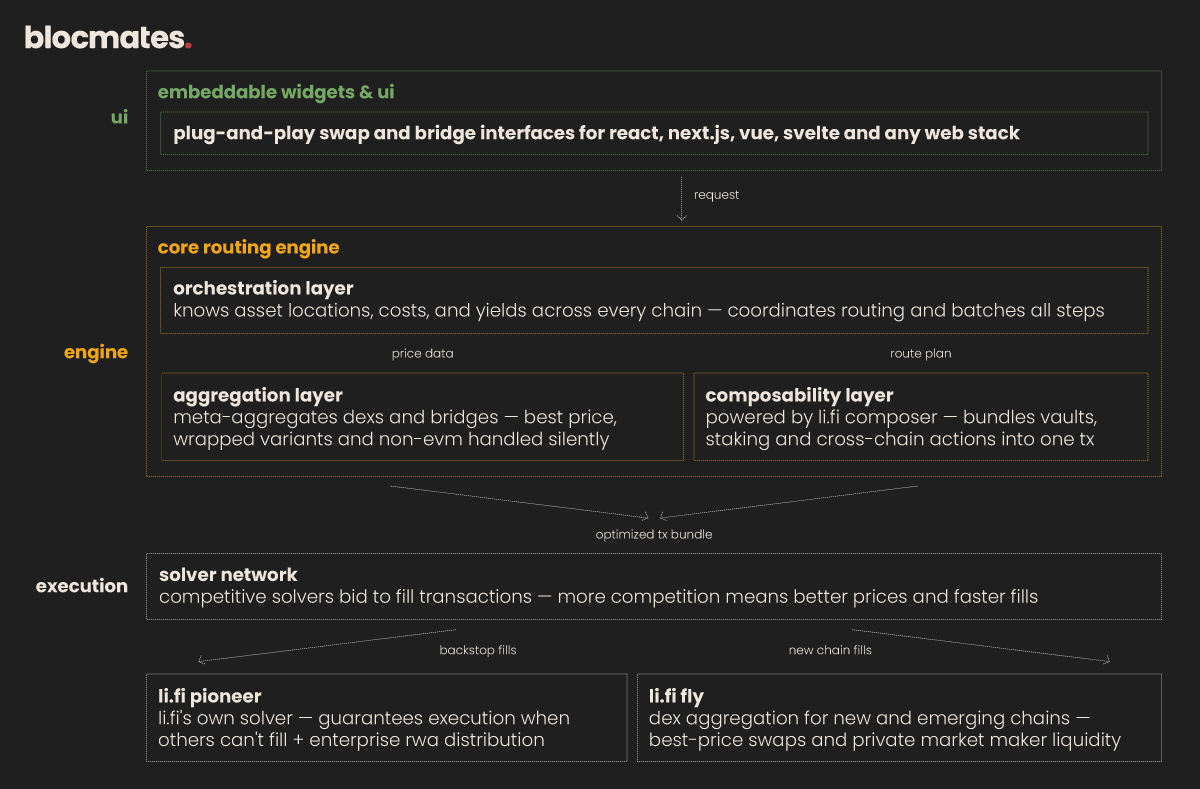

The journey to this simplicity was built on years of developing cross-chain infrastructure, a proven solver network, and advanced routing logic capable of identifying the best path across over 65 blockchains within a single transaction.

Even if you only intend to feature just a few chains and protocols, it's nice to know that there is no ceiling, with support for new and relevant chains on day one.

LI.FI’s edge

Going back to the EY/Coinbase report I mentioned at the start, a key takeaway reveals exactly what’s needed to move the industry further and why Li.Fi has the edge over other YaaS offerings.

“...given faster settlement and more continuous markets, scaling will depend on converting regulatory progress into implementable rules and buildout of interoperable rails with sufficient liquidity to support institutional size.”

On the interoperability front, LI.FI's protocol layer handles everything from routing to execution. It knows where assets are, what they cost, and which yields are available across every supported chain, then finds the optimal path and bundles multiple steps into a single transaction.

On the liquidity side, LI.FI has a solver network comprising a set of solvers and market makers that bid to fulfill user trades. LI.FI also features its own solver to guarantee transaction fulfillment whenever third-party solvers are unavailable.

And to top it all off, the LI.FI Fly DEX aggregator supports new chains from day one, granting them access to the entire ecosystem.

With the undeniable interoperability expertise under their belt and infrastructure capable of handling institutional size, moving into yield was a natural horizontal expansion that required codifying it into two API endpoints.

But as we know, that’s just one part of the equation. With the Lazarus Group on the loose and kids vibe-coding novel attack methods with LLMs, security is arguably the most important part.

With over eighty independent smart contract audits performed (since 2024) before the launch of any feature, a bug bounty program with up to $1 million in rewards, and a dedicated security team specializing in blockchain and DeFi security, alongside annual web2 security tests, the LI.FI team takes security very seriously.

As for the available DeFi protocols, let’s hope they treat security just as diligently.

Concluding thoughts

TradFi and crypto-native products are converging. That convergence point is characterized by blending traditional rails with blockchain, without revealing the product's nature to the user at all. The DeFi mullet, if you will.

No matter your starting point, one thing is abundantly clear: new chains and yield opportunities are always emerging.

What that means practically is that opportunities will keep knocking on your door faster than any in-house team can track.

The infrastructure you choose today needs to be extensible enough to absorb that without forcing a reintegration conversation when you've got real users and real volume on the line.

Nobody wants to duct-tape five providers, manage fragmented liquidity, and pray nothing messes up mid-transaction.

And yes, while I would realistically only trust a few key lending platforms with my hard-earned money today, that doesn’t mean this will always be the case.

The winners here will be those who can abstract away all the complexity while still giving users access to the full breadth of what DeFi has to offer. And LI.FI, imo, will be one among them.

Thanks to the LI.FI team for unlocking this article. All of our research and references are based on public information available in documents, etc., and are presented by blocmates for constructive discussion and analysis. To read more about our editorial policy and disclosures at blocmates, head here.

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)