.webp)

Reading time: 10m 59s

The world is finally waking up.

Soon, the concept of a market opening at 9am and closing at 4pm, like some video game, will become an archaic one, similar to waiting three business days for a wire transfer or physically calling your broker to place a trade.

You will be asking yourself, “Why the hell was that even a thing?”

The rising popularity of crypto has proven that 24/7 markets are intuitive, efficient, feasible, and simply a better way to trade.

Don’t take my word for it; the movement has already begun. Nasdaq has been seeking to introduce “round the clock” 24/7 markets, NYSE Arca got approval to extend trading hours to 24/5, and Wedbush Securities launched a 24/7 exchange for US equities that’s been approved by the SEC.

I think you get the idea, 24/7 markets aren’t just a gimmick for the “crypto bros.” It’s a real phenomenon that’s the backbone for truly global financial markets.

Why do 24/7 markets matter?

What might be considered foreign to someone from a TradFi background is merely the norm for those of us still active in the chaotic world of crypto.

The primary reason why 24/7 markets matter is accessibility, a core part of crypto’s ethos. Just because a person is born in another country doesn’t mean that they should be excluded from being able to trade in certain markets.

Open accessibility for anyone, at any time of day, from anywhere in the world, is a powerful phenomenon.

If a person living in Thailand and the United States of America can trade the same asset in BTC at any time of the day, why shouldn’t the same be allowed for something like TSLA shares, or oil futures, or silver?

Open accessibility is a core pillar for truly global, borderless financial markets.

Fortunately, we live in a world where the rails already exist, with crypto markets being the perfect proof of concept (though it’s much more than just that). It’s proof that 24/7 markets can exist and are intuitive, efficient, and globally accessible.

Blockchains have always been the ideal form of truly digital-native money, but in terms of scalability, it has only recently reached a point where high-volume, high-frequency markets can exist fully onchain.

With that hurdle now crossed, you are already seeing the rise of 24/7 markets for ALL assets on exchanges like Hyperliquid, where traders can now trade US equities, indices like the S&P 500, commodities like Gold and Silver, or even equities from other foreign markets.

The pricing problem

The issue has never been the concept of 24/7 markets; I think the rising volumes on Hyperliquid can be a testament to that.

The issue has always been pricing infrastructure.

The onchain world has been almost shackled by the legacy oracle infrastructure monopoly. Let me explain how, as there are two layers to this problem.

First off, legacy oracle providers ultimately hold all the aces. They have the final say over which assets can be listed as they decide whether a data feed is worth providing or not.

So, they may decide that it is worth their time to create an oracle for NVDA shares, but what if someone wants to trade more long-tail assets, like a small-cap or pre-IPO company?

Developers are ultimately at the mercy of these companies because it is incredibly hard, insecure, and expensive to build their own oracle infrastructure.

Secondly, the underlying technology of how legacy oracles work is not programmable enough to bring non-crypto assets onchain into 24/7 markets.

When markets are closed, how does one obtain pricing data for pre-market, post-market, overnight, or weekend periods?

This means, even if legacy oracle infrastructure is used, there’s still a need to create custom pricing logic for non-market hours.

This essentially shifts the technical burden of custom pricing logic onto the developer/deployer.

It’s a heavy technical lift, time-consuming, and expensive. On top of that, it will lead to price discrepancies across venues with different deployers, and there will be a LOT of room for price manipulation.

With that, we come to the topic of today's article.

A product that has rebuilt infrastructure from the ground up to make it dynamic, programmable, and intuitive. A product that will accelerate the growth of 24/7 markets for ANY asset. A product that is already proving its might, having facilitated 10 billion+ volume in its first eight weeks.

Let’s look at how SEDA will be the backbone of 24/7 markets.

A SEDA primer

For a complete breakdown on everything SEDA, check out this article first. But here’s the TLDR.

SEDA is a layer-1 (L1) blockchain designed for programmable oracle infrastructure. Similar to how Ethereum hosts smart contract logic for applications, SEDA hosts data feed logic for applications.

Here’s a good way to think of it: SEDA is to oracles what AI agents are to search.

Much like search engines, traditional oracles are static, manual, and limited. You request data and receive some results; that’s it. Much like AI agents, SEDA makes things more dynamic with more flexibility, control, and customizability.

At the heart of SEDA is its core innovation called Oracle Programs (OPs).

Oracle Programs are smart contracts that hold custom logic for a data feed. It can be thought of as the customizable brain for the oracle feed that an application receives.

SEDA has two distinct product offerings:

- SEDA Core is the default method for data delivery. This is a fully onchain, trustless way to query any data source and deliver the results to any chain.

- SEDA Fast is a high-speed version of SEDA’s regular onchain data delivery designed specifically for applications that may need real-time or near-instant data delivery.

In short, SEDA is a one-stop shop for all your custom pricing needs, offering programmable oracles with full customizability to allow pricing of any asset for 24/7 global markets.

It allows the creation of fully customizable pricing logic for any non-crypto asset, whether a popular stock or a pre-IPO company. It’s the epitome of simplifying the implementation of complex financial instruments and will undoubtedly be the backbone of 24/7 markets.

Now that you’re up to speed with what SEDA is, let’s look at a real-life example of SEDA in action.

SEDA x HIP-3

Hyperliquid has now firmly established itself as THE go-to venue for all your onchain trading needs.

However, it was HIP-3 (Hyperliquid Improvement Proposal 3) that actually took Hyperliquid from just another onchain perp DEX to the house of all finance.

HIP-3 introduced a permissionless system that allowed anybody to deploy their own perpetual market directly onto the HyperCore engine. This framework meant that anybody could list any asset they wanted.

All that’s needed is:

- 500k HYPE staked

- Market parameters (leverage limits, fees, etc.)

- Oracle(s) for pricing

Just like that, you can trade any financial asset onchain.

Want to trade TSLA? Done. Want to trade silver and gold? Done. Want to trade treasury bills? Done. Hell, they recently even brought the S&P 500 onchain.

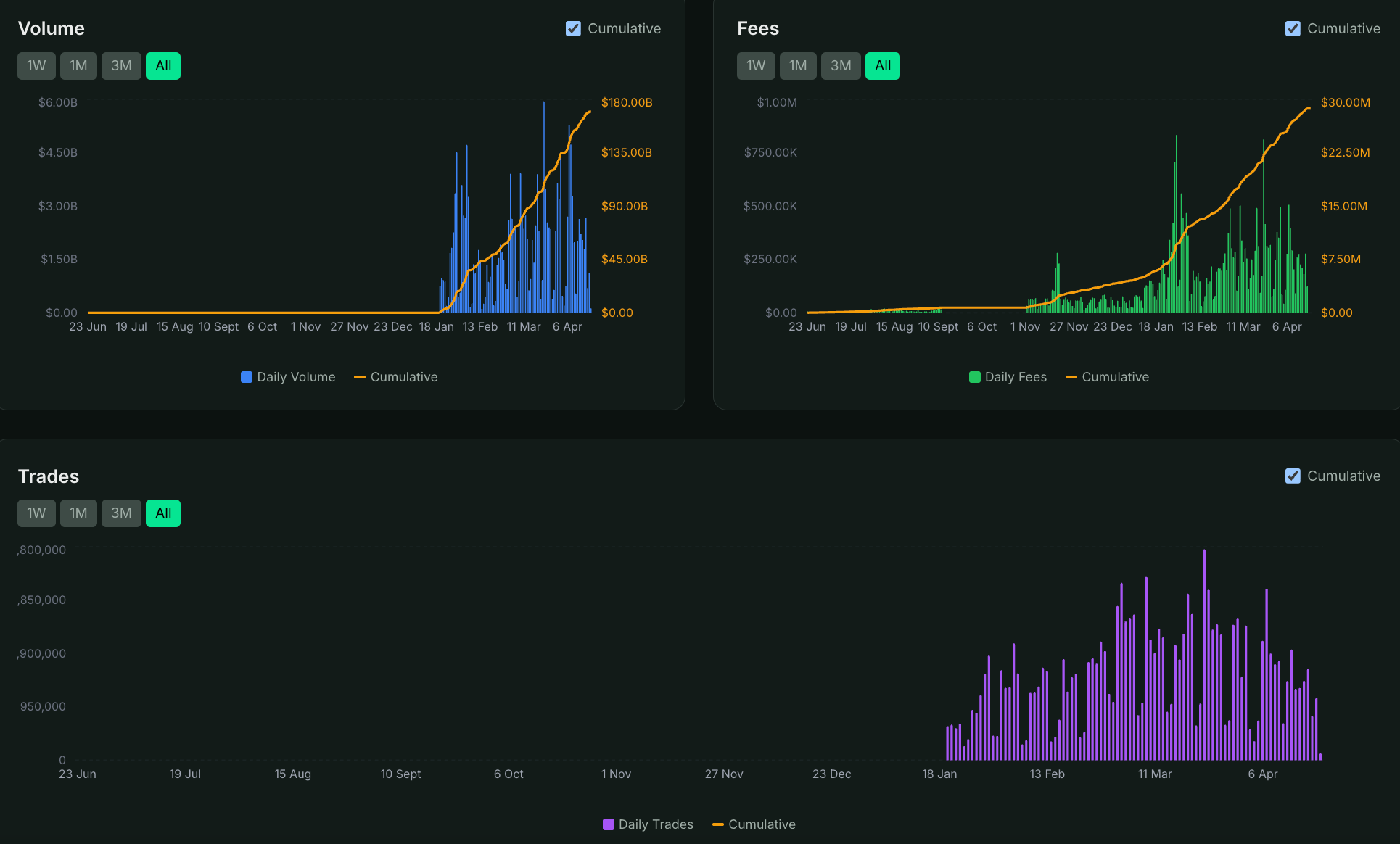

The results have been nothing short of spectacular:

- $169 billion in total volume

- $2 billion in open interest

- $28.7 million in fees generated

- Over 1 million trades daily

- Consistently averaging over $1 billion in daily volume for the last 2 months

But, in order for Hyperliquid to truly become ‘the house of all finance’ at scale, and by scale I mean on a global scale, it needs easy access to all finance 24/7/365.

That access can only be provided by SEDA.

SEDA is already well entrenched in the HIP-3 ecosystem, as it is used by one of the biggest deployers, Dreamcash, for oracle pricing.

Let’s quickly understand how Dreamcash leverages SEDA.

Dreamcash partially leverages Pyth’s oracle infrastructure for standard price data on common assets, giving price feeds during regular market hours. But it’s SEDA that makes all the rules for the pricing logic to work.

So SEDA wraps all the individual Pyth price feeds, applies the logic as per the Oracle Program, and then allows Dreamcash to consume one single endpoint with a single data output for continuous 24/7 price updates.

To keep a continuous price stream even during off-market hours, Dreamcash’s pricing logic uses the oracle price (of course), a 150-second EMA, an 8-hour EMA, and a smoothed price, which basically takes into account the discount/premium from Dreamcash’s own orderbook (this is to prevent liquidation with sharp price triggers).

Using SEDA’s Oracle Programs, Dreamcash can combine all these elements into its own pricing logic and create a continuous (24/7) blended price for any non-crypto asset.

SEDA also provides the rules, which means that the Oracle Program will define when to switch between Pyth’s oracle (during regular market hours) and the off-hour pricing logic.

It also provides the logic for how price is handled as feeds switch from off-market to on-market pricing logic, which prevents spikes between sessions, protecting traders against unfair oracle liquidation cascade events.

Here’s a quick sneak peek at how SEDA has been able to successfully price assets on Dreamcash 24/7.

With the help of SEDA’s oracle infrastructure, Dreamcash at one point was averaging over $2 billion in weekly volume.

Looking beyond Hyperliquid

Although SEDA’s involvement in Hyperliquid is impressive, its programmable oracle infrastructure can be used for a wider variety of assets in multiple different ways, seeing that it also powers 24/7 markets for pre-IPO products, T-Bill yields, and volatility reference markets, among other things.

The primary benefit from SEDA’s programmable infrastructure is that when an asset comes onchain, it comes with context-awareness.

What does this mean?

Context in this scenario refers to things like:

- What happens when the exchange for an asset shuts/pauses?

- If an oracle feed becomes stale, how does the system transition to keep the price continuous?

- If a futures contract has a cost-of-carry embedded, how does that get baked into the price?

- How does the asset behave when it’s transitioning across sessions (regular hours vs. off hours)?

All of this (and more) is what is offered by SEDA’s Oracle Programs. It shifts from a one-size-fits-all oracle solution to a more dynamic and customizable oracle infrastructure suited to efficiently price any asset in the world.

Developers have the freedom to encode any sort of market-specific logic, whether it’s session-awareness or staleness handling, directly into the oracle layer, which will automatically self-execute.

It’s because of this that SEDA is trusted by many other top protocols, including Injective, Helix Markets, Outcome, and Stratium, to name a few.

SEDA powering ALL markets

Now that you have a practical understanding of how SEDA’s oracle infrastructure works on the ground, it’s time to understand the real magnitude of what’s possible, because all of this is just the beginning.

SEDA unlocks a completely new design space, which is why we firmly believe that it will be the backbone of ALL 24/7 markets.

1. Volatility indices

Products like the VIX, or CBOE Volatility Index, are really popular. However, pricing these products is generally tough. The final value is derived from options markets, which themselves depend on a vast number of other underlying variables.

Despite the complexity, the ability to trade the VIX or other volatility indices is certainly a compelling product that many traders would be interested in.

Prior to SEDA, building an oracle to price volatility indices was pretty much an insurmountable task. I think it would genuinely be easier to teach your grandma crypto and turn her into a full-time shitcoin trader than build this oracle from scratch.

Through a simple Oracle Program, SEDA gives deployers the tools to build their own price feed for volatility indices that runs continuously with minimal overhead and is easy to tweak after testing to ensure everything is working as expected.

2. Fixed-income instruments

It’s the same story for fixed-income products.

Let’s take something like three-month treasury bills, for example. T-bill rates don't move continuously the way equities do - they're driven by Fed policy, treasury auction results, and macro factors that can shift on a weekend announcement.

Pricing a T-bill perpetual correctly requires an oracle that understands yield dynamics, can factor in Fed funds futures, and applies appropriate smoothing during low-information periods. SEDA's programmability handles all of this natively.

3. Exotic structured products

Structured products are a very broad, all-encompassing term, but for this case, let’s narrow it down to one hypothetical example.

Think of a yield product that combines DeFi rates, equities, and real estate into one structured yield vehicle that people can invest in.

The success of such a product depends solely on the quality of the data and how it is used to create a blended price of sorts.

Such products will clearly be in demand, as they offer investors diversity and customization. However, creating such products without SEDA is incredibly difficult.

Through an Oracle Program, data can be sourced from multiple providers, and a blended price mechanism can be coded into the contract to ensure that it updates automatically in line with the data.

Allowing for the creation of such structured products is a sure-shot way to attract serious institutional money into the onchain world.

4. Exotic markets

Whether it's something more topical, like prediction markets, or something more unconventional, like a perps market for collectibles, SEDA has the unique ability to efficiently price any type of market.

With HIP-4 bringing binary markets to Hyperliquid, SEDA has the ability to power this new wave of prediction markets that rely on contextual data and have a unique struggle with conflict resolution for certain markets.

If you go beyond and look at a product like Perps.fun, which allows for the creation of a perpetual market for ANYTHING, whether it's collectibles, niche indices, or pre-IPO companies, you can trade anything, all thanks to SEDA's underlying programmable oracle infrastructure.

5. Composability

Composability across applications has always been a core tenet of DeFi, and this is something that is only going to grow in strength with non-crypto assets coming onchain.

There’s a growing popularity of platforms accepting tokenized stocks or commodities for protocol functionality - whether it be an onchain lending platform using xSTOCK as collateral, or a yield-generating vault leveraging xCOMMODITY, or a platform allowing for long/short bets on xPRE-IPO.

The composability possibilities are endless, but they can only be made possible if price behavior is predictable and relatively stable, especially during thin sessions, pauses, or session transitions.

SEDA’s Oracle Program is the solution that offers this reliability, ultimately powering a whole new suite of composable applications. Applications that you and I have probably not even thought of yet.

Concluding thoughts

The narrative around 24/7 markets usually focuses on the product layer - and understandably so. The ability to trade Tesla at midnight or buy S&P 500 exposure on a Sunday is genuinely exciting, and the numbers coming out of HIP-3 prove the demand is real.

But none of that works without solving the infrastructure problem underneath it. Bad oracles don't just cause mild inconvenience. They cause incorrect liquidations. They create arbitrage surfaces that sophisticated players exploit at the expense of regular users. They make it impossible to scale to more asset types without an army of engineers rebuilding custom pricing logic from scratch every time.

SEDA is the infrastructure-level solution that ultimately makes everything possible. This opens up doors for increased retail participation, more significant institutional investment, and more market maker involvement, while also simplifying the lives of devs/deployers.

The proof is already live with over $5 billion in volume facilitated on Hyperliquid.

24/7 markets for traditional assets are not coming - they're already here. The remaining question is whether the oracle infrastructure beneath them can keep up with the pace of demand.

Right now, SEDA is the only thing purpose-built to answer that question at scale.

Thanks to the SEDA team for unlocking this article. All of our research and references are based on public information available in documents, etc., and are presented by blocmates for constructive discussion and analysis. To read more about our editorial policy and disclosures at blocmates, head here.

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)