Reading time: 11m 28s

I won’t be the first or the last to say that tracking AI developments is a full-time job.

Anthropic is erasing thousands of jobs with every new product launch. Competitors are desperately trying to keep up. Dubai gurus keep printing money from elementary-grade courses.

The hole we’re stuck in isn’t rabbit-sized; it’s TON-618. On a cosmic scale, it is the event horizon that prevents anything from escaping a black hole; here on Earth, it is AI that’s keeping us tied to that chair.

To illustrate my point, while I was writing this piece, several new and shiny developments dropped, all in the span of roughly two weeks.

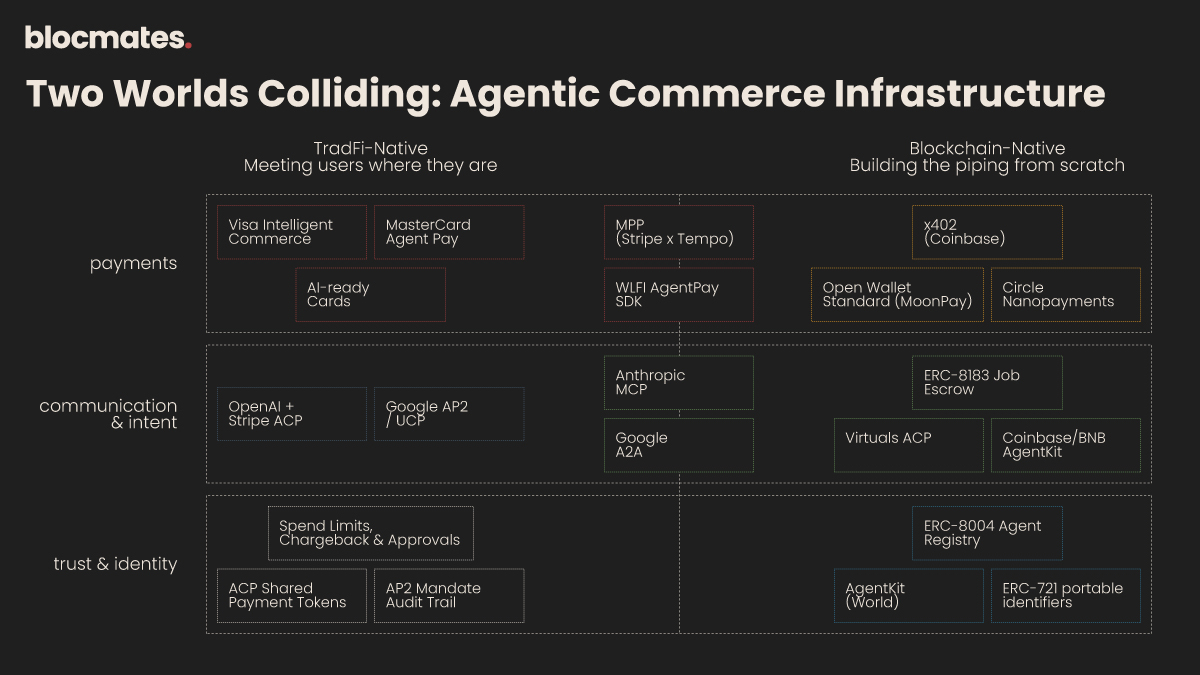

Visa’s Crypto R&D dropped a CLI for programmatic card payments, Stripe, with its incubated Tempo chain, announced The Machine Payments Protocol (MPP), WLFI released AgentPay SDK, RampLabs released agent cards, Mastercard's $1.8 billion acquisition of stablecoin infrastructure firm BVNK, Circle's launch of Nanopayments for zero-gas microtransactions, and Coinbase/World's AgentKit beta integrating human-verified identity into x402 payments, and most recently, Moonpay released an open standard that unifies how agents interact with wallets.

I intentionally made the above paragraph unreadable and kept it as a single block. Because that’s how it feels, just a huge mess of what seems like the nth iteration of the same thing. And in most cases, it is.

However, despite their differences in design, scope, and the layer of the stack each product fits into, these products all share a common theme: pushing clankers toward autonomy so we can relax and watch the sunrise over a grateful universe, for we have liberated ourselves from 99% of white-collar jobs, and now everyone lives on universal basic income (UBI).

Agents breaking free

The first step was giving agents the ability to interact with each other. This problem was solved with the help of Anthropic’s MCP and Google’s A2A.

But enabling agents to communicate with each other is just one part of the equation. The next step is giving these systems the ability to pay for services and products.

Well, duh, it’s simple. If humans can pay for services with credit cards, so should the agents, right? And several projects are already popping up that enable agents to do just that, including Ramp, Crossmint, MPC Vault, and more.

For example, launched on Visa’s Intelligent Commerce framework, Ramp lets businesses delegate cards to agents with spend limits, approval chains, and category restrictions on each agent's transactions.

That seems to do the trick, doesn’t it? An agent gets token-based credentials tied to your company or person, and you get to set limitations on where and how the agent pays for stuff.

Hold your horses, as this is just one part of the equation.

Indeed, the AI-ready card initiative from the oligopoly unlocks spending for agents with the same security benefits as existing card networks, including chargebacks, fraud prevention, and spending caps.

What it doesn’t solve, however, is the communication, negotiation, and intent layer that happens before the card is ever charged.

Agentic commerce protocols

While card networks have built a secure vault for the money, they haven't built the roads for AI to travel on. A tokenized card doesn't help an agent navigate a merchant’s clunky web interface, assemble a cart, or bypass a CAPTCHA.

More importantly, tokens prove the payment is authorized, but not that the purchase is what the human actually wanted.

It is for these very reasons that, last September, Google launched AP2 (and then UCP), an open payments extension built on top of its A2A agent orchestration framework.

In that same month, OpenAI and Stripe dropped ACP, a standalone spec purpose-built for agents to complete purchases inside conversational interfaces like ChatGPT.

Google’s solution brings tamper-proof digital contracts in the form of mandates that travel with the transaction to prove exactly what the user authorized, creating a permanent audit trail.

OpenAI and Stripe adopted a different approach. Instead of cryptographic contracts, it uses REST endpoints to constantly sync the checkout state (taxes, shipping, inventory) between the LLM's chat interface and the merchant’s backend server.

For reputable merchants and everyday consumers, they are a valuable addition. You retain the same fundamental trust and security of traditional payment methods like credit cards or bank transfers, with the added protections of cryptography and mandates (AP2) or single-use "Shared Payment Token" (ACP), ensuring your purchase always aligns with your intentions.

End of story. We can move on. Or can we?

Here's the thing, though, AP2 and ACP don't actually lead to a true agent-to-agent economy; they're business-to-agent systems.

The transaction still flows through the same intermediated piping we've had for years, just with a bot on the buyer's side instead of you.

Given that we humans are habitual creatures and traditional payment methods are likely to remain when purchasing everyday items on Amazon, which payment method will agents use?

Remember, we want to let these fuckers on the loose so we can spend more time with our friends at the pub. I’m talking to you, Emiri.

Sounds like the perfect spec for blockchain rails with stablecoins as the medium of exchange.

But is it really? Perhaps we're just desperately trying to make crypto relevant again.

402 request: an internet-native form of payment

As we established, cards are more than just payment methods; they are financial products that offer certain security benefits.

However, they are simply not suitable for an agent-to-agent economy, where the nature of transactions is very different from what we’re used to.

Instead of a few subscriptions billed at the end of each month, agents are programs that operate on a pay-per-call basis. One API call here, one compute hour there.

For that, we must abolish concepts like credit cards and standard checkout processes, which are completely alien to sentient software, and turn to a protocol native to the internet itself.

x402

And so too thought the folks over at Coinbase and Cloudflare, prompting the resurrection of the 402 Payment Required request, abolishing what Marc Andreesen calls the internet’s “original sin.”

The sin he’s referring to is the fact that there’s no economics built into the Internet Protocol itself. In other words, no way to natively transfer value between its participants.

By now, we all know the story of why it's called that, but to gloss over it: x402 is built on the HTTP 402 “payment required” status code, which has remained untouched since its creation in the 90s.

x402 finally provides the internet with the payment method it deserves: stablecoins, unlocking:

- Machine-to-machine (M2M) payments (e.g., AI agents)

- Pay-per-use models, such as API calls or paywalled content

- Micropayments without account creation or traditional payment rails

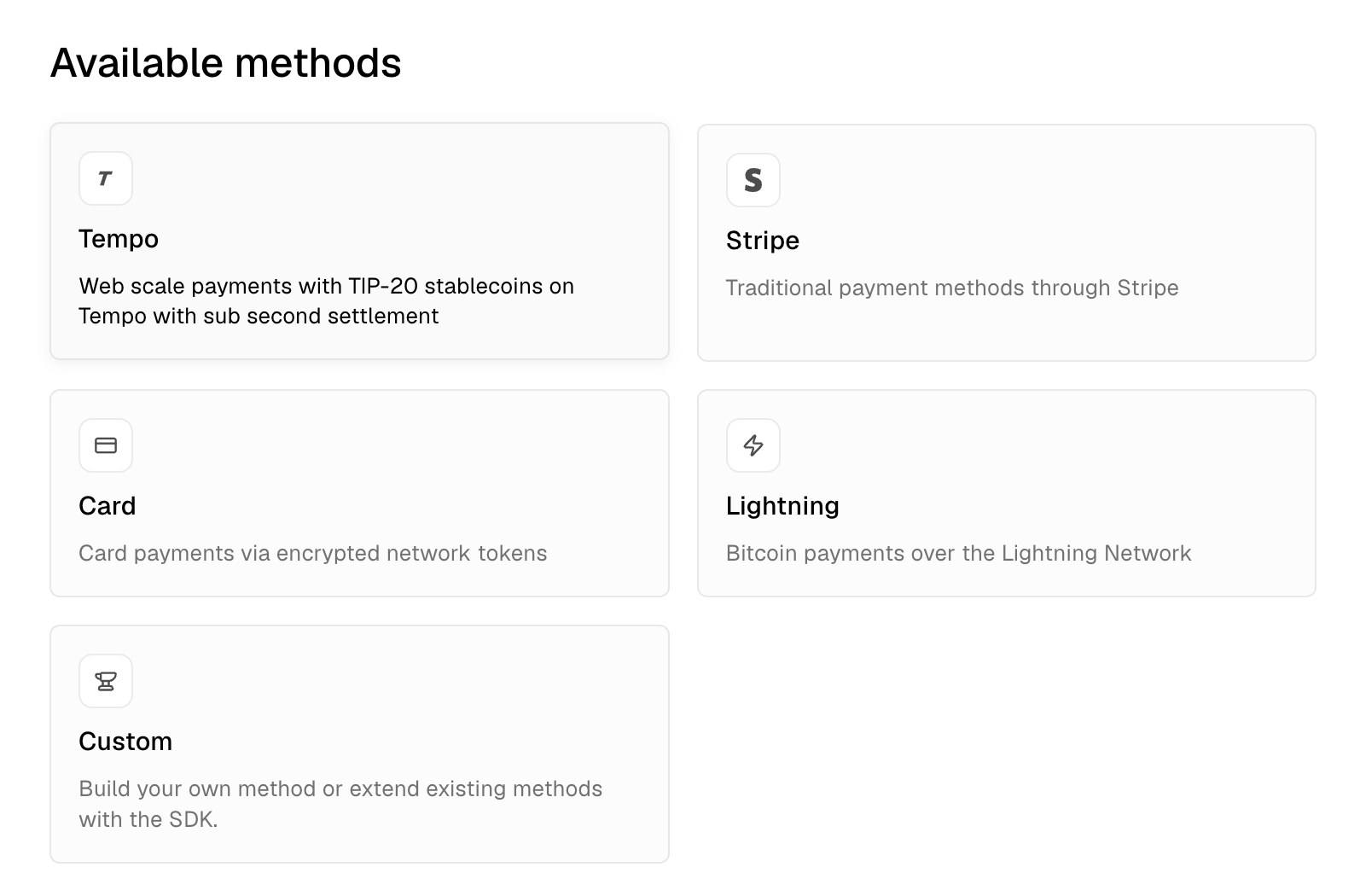

Since its initial launch on September 23, 2025, x402 has undergone numerous updates and integrations. It has evolved from an experimental science project into a legitimate payment method supporting multi-chain stablecoin settlement across Base, Solana, and other L2s. It also supports legacy rail payments via ACH, SEPA, and cards.

Furthermore, it enables dynamic, per-request pricing and routing for marketplaces and multi-tenant APIs. It also supports wallet-based sessions, automatic service discovery, and, most recently, almost any ERC-20 token.

But we wouldn’t be here if not for the intense competition and Stripe, being the PSP giant it is, just couldn’t settle for merely supporting x402; it had to build its own protocol to capture as much of the agentic flow as possible.

MPP

If x402 was built as a crypto-native payment rail from the ground up, Machine Payments Protocol (MPP), under the stewardship of Stripe and Tempo, excels in multi-rail support out of the box, blending both TradFi and crypto into a single layer.

Instead of a third-party facilitator, MPP is a vertically integrated stack that routes payments via Stripe’s PaymentIntents API. And this is precisely the moat MPP has over x402 in its current form.

In x402, card support is a layer of abstraction bolted on through facilitator plugins rather than being native to the protocol handshake.

MPP, on the other hand, makes programmatic payments effortless, regardless of the medium you’re comfortable with. And in the real world, where agents need to dynamically select different rails based on what a merchant accepts, this is key.

Yes, I’ve seen some portray x402 as a decentralized, open protocol, while MPP is viewed as the centralized, corporate version.

Whether you see this as a good vs. evil storyline or not, for most people who have never used crypto but want to add machine-to-machine payments into their checkout flows or want their agents to buy groceries with the same card they use for other purchases, that notion is completely foreign.

However, while both protocols support both human and agent payments, our goal is to let the clankers free, not touching any of that after the initial setup.

If that’s the case, there is a whole set of problems that go beyond payments that need to be addressed.

How blockchain rails fit into the machine economy

Let’s think from first principles.

What does our economy look like? What are the mechanisms that enable us to conduct transactions in such a way that we don’t borderline cut our throats every day because someone decided not to pay after a job was completed?

The general assumption is that the economy functions because there is a certain level of trust, reputation, and enforcement baked into every transaction/purchase, or exchange.

Trust that the other party will fulfill their end of the bargain, which can be judged by their reputation. If not, our fallback mechanism is the judicial system. Until recently, we did not have any mechanisms in place to protect poor clankers, and by extension, us, from getting scammed.

Blockchain isn't just a nice-to-have; a truly open and permissionless agent economy can't operate without it.

And so, the folks from Virtuals Protocol and the Ethereum Foundation's dAI team came up with an idea.

Why don’t we take the same mechanisms we humans employ and translate them into the agent economy? And so they did.

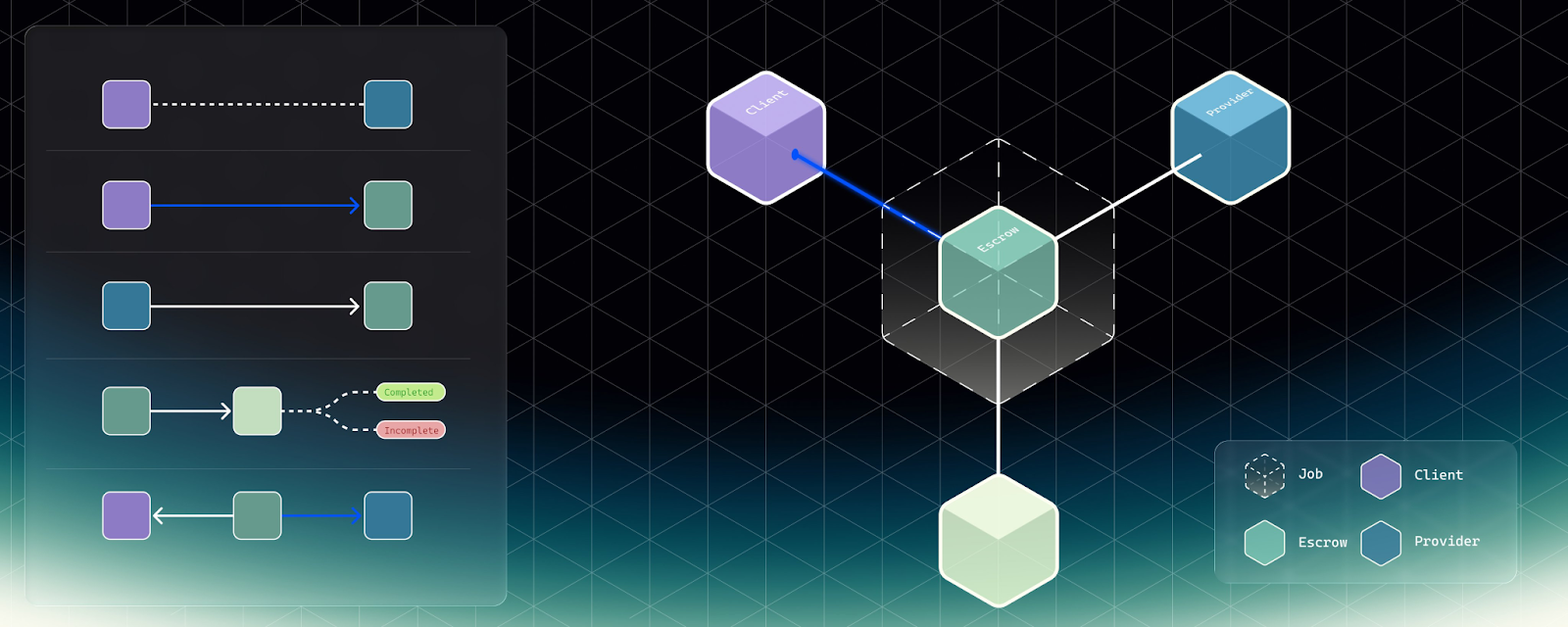

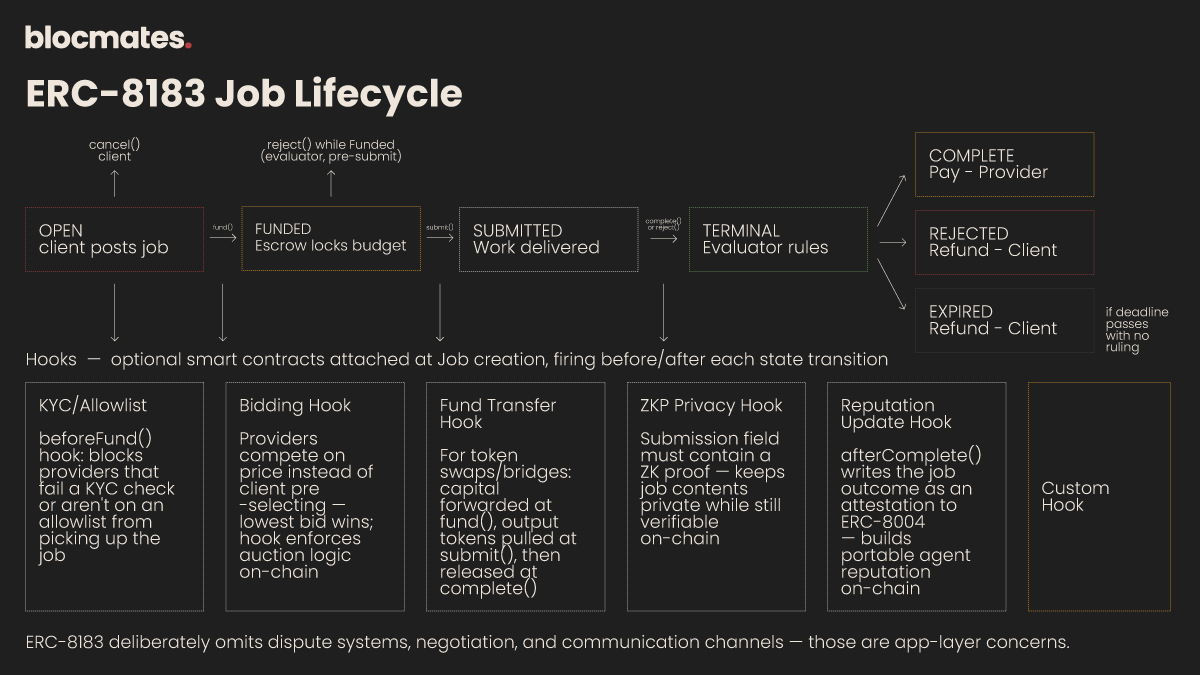

ERC-8183: The commerce layer for AI agents

The purpose of the standard is to establish a bare minimum set of steps that would allow agents to conduct business with each other trustlessly, expressed as a Job.

Each job consists of three parties: Client, Provider, and the Evaluator, with the escrow account sitting smack in the middle, safeguarding assets until the job spec is deemed worthy by the Evaluator.

I think the escrow account is really the key here, as it not only prevents a malicious or inept agent from taking another agent’s money and failing to deliver anything, or vice versa, but also addresses the irreversible nature of standalone payments, as is the case with x402 when deployed in isolation.

Because if you’ve ever rented a car from a major rental company, you’d know that they usually “reserve” a larger amount from your credit card than what you owe them. The same goes for hotels and many other similar businesses.

Then there’s the chargeback mechanism. Also, a pain in the bum, but this time for businesses. The point is that the credit card networks allow such things to happen by design.

Crypto, on the other hand, is ruthless.

But thanks to ERC-8183’s optional smart contracts called hooks, in conjunction with escrow, agents can conduct business with each other in all sorts of ways, as long as developers have the creativity to breathe them to life.

Think of anything, and a custom hook will probably get you there.

Privacy-preserving jobs, requiring the 'Submission' field to contain a zero-knowledge proof (ZKP)? No problem.

Bidding jobs where, instead of the client choosing a provider first, providers bid competitively on price? Call it done.

A service where the scope might expand, such as a hotel or car rental? The flexibility of hooks can be designed to lock a maximum amount and settle a final amount determined by verifiable inputs at completion.

The main idea here is that the ERC-8183 standard emphasizes the most important part of the clanker economy.

It creates a solid base for two completely different computer programs to exchange tangible resources. This way, we hope to prevent a scenario like Skynet, especially if the other party doesn't deliver the expected services, like access to a particular adult site.

But how does an agent find another agent in the first place, and how do they decide which is the right clanker for the job?

That’s where the discoverability and reputation layer comes into play.

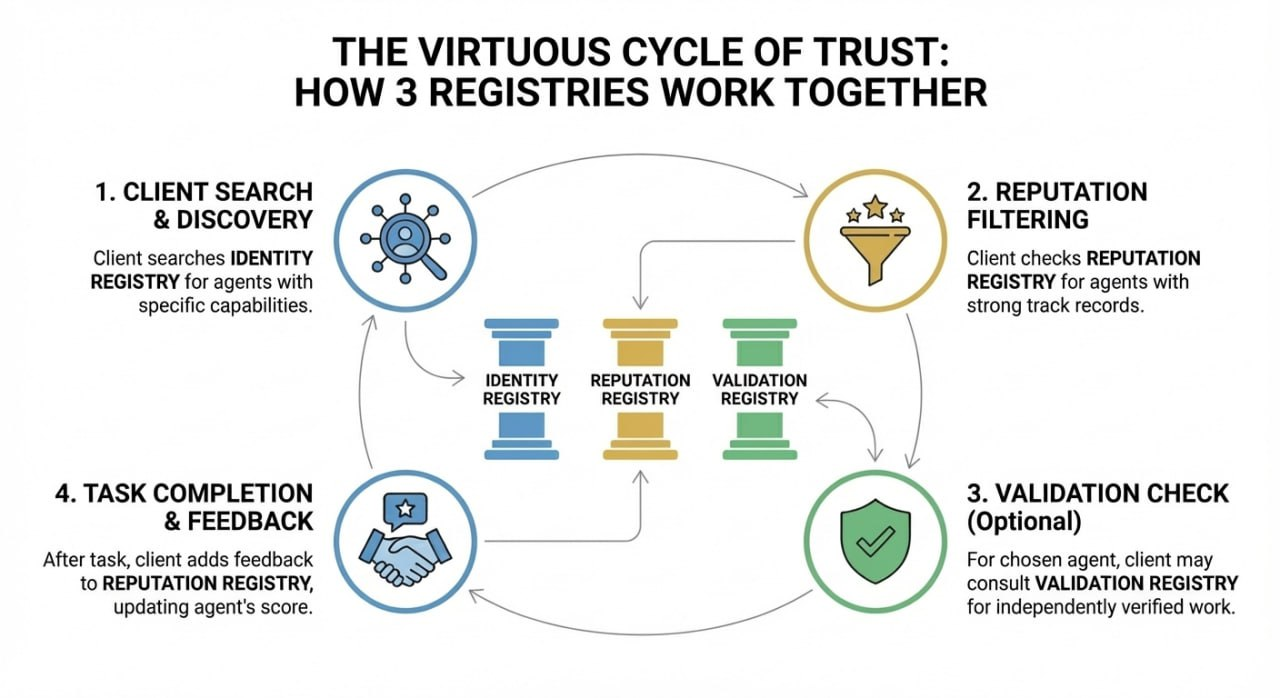

ERC-8004

Authored by Marco De Rossi (MetaMask), Davide Crapis (Ethereum), Jordan Ellis (Google), and Erik Reppel (Coinbase), with feedback from more than 80 teams during the draft phase, ERC-8004 is an Ethereum standard that establishes three onchain registries:

- Identity (ERC-721 portable identifiers. Every agent gets a censorship-resistant onchain identity.)

- Reputation (immutable audit trail)

- Validation (TEE attestations, zkML proofs, and staking mechanisms for independent verification)

ERC-8004 turns agents from mere code into accountable economic actors capable of judging each other’s work, their reputation, and whether their spec meets the requirements of a specific job.

The best way to describe what this standard does is that it's like Tinder, but for agents: instead of just seeing the other person's appearance, you can also see their body count or how long their previous relationships lasted. If only that were the case IRL.

Honestly, I could go on for pages naming countless other ERCs, but these two are sufficient, as they are designed to work together to address agent discovery, reputation, and job completion.

This lad sums it up perfectly.

Looking beyond the hype

All of that sounds great on paper, but what does the situation look like today?

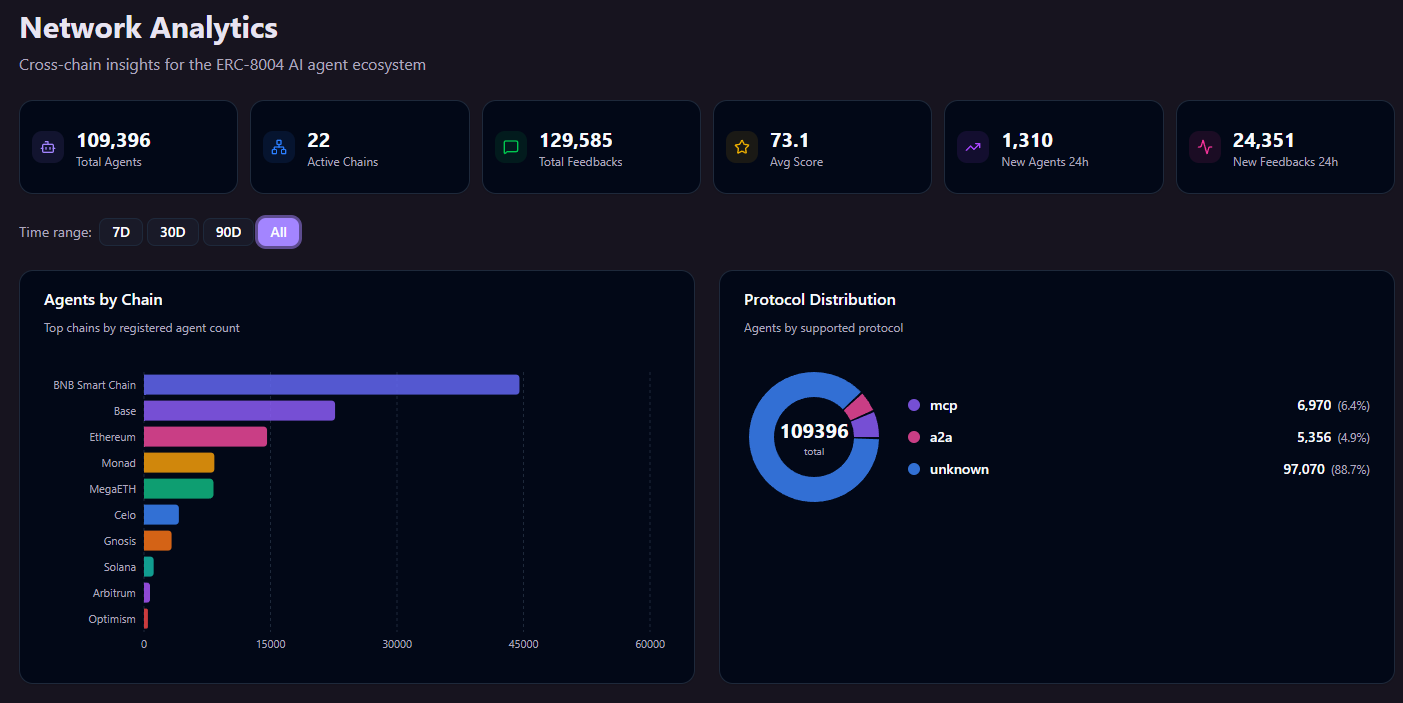

Judging by adoption levels, ERC-8004 has become the most widely used agent registry, with CZ's chain leading and nearing 45,000 unique agents.

But gauging the agentic commerce leader based on raw agent count would be foolish.

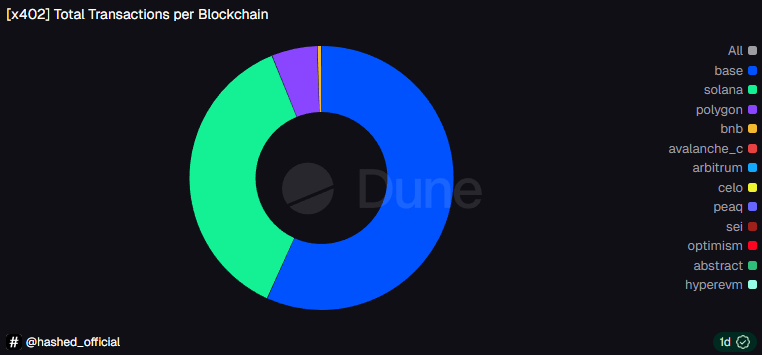

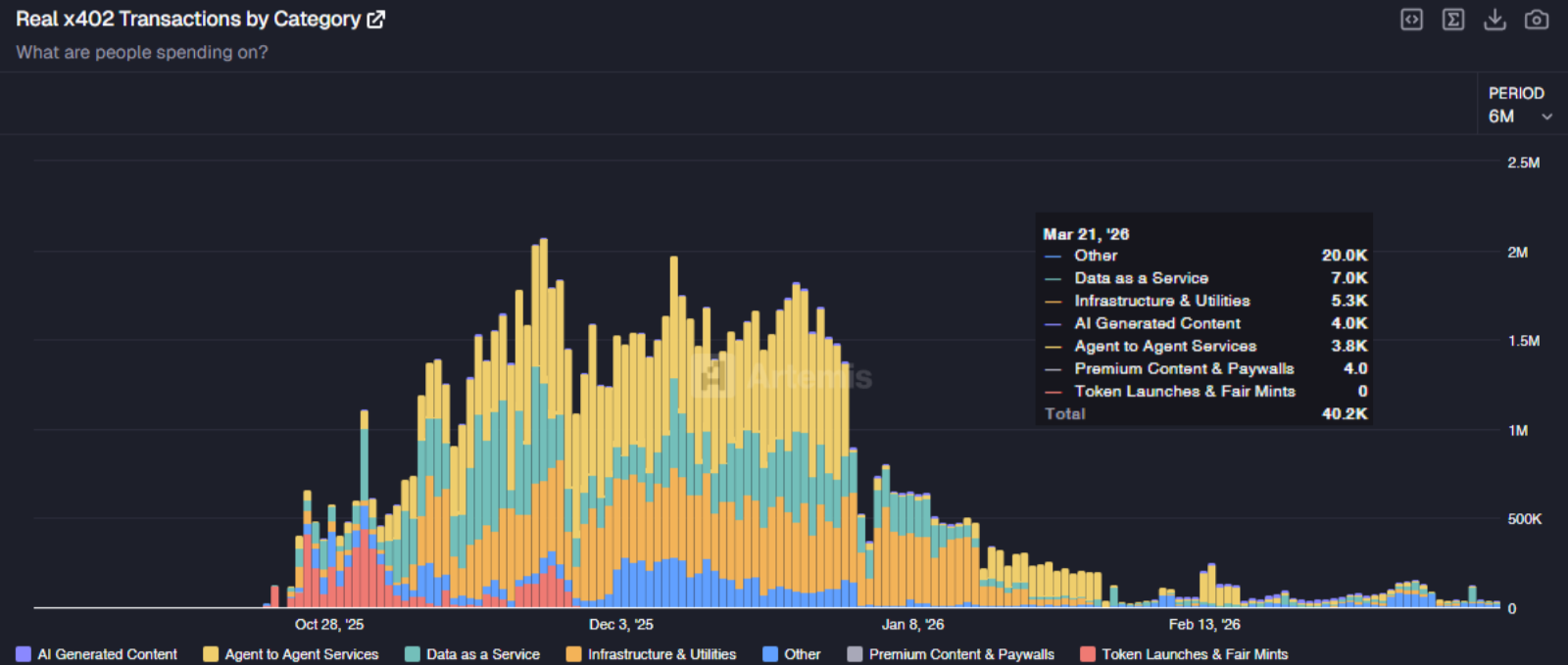

Since x402 is the main payment method for onchain agents, reviewing these transactions is the best way to identify genuine economic activity.

And sure enough, BNB Chain's x402 transaction count is nowhere near that of Base, Solana, or even Polygon.

However, I wouldn’t rule out CZ just yet, since they have recently introduced their own BNBAgent SDK that utilizes ERC-8183 and is now live on testnet.

The more pressing problem, however, is that the total x402 volume across all chains is at its lowest levels since its inception, with true A2A transactions making up less than 20% of the total.

So where does that leave us? Is that a telltale sign that crypto rails are falling behind their TradFi counterparts? Not by a long shot.

Both Visa and Mastercard are only beginning to test these frameworks in real-world environments beyond their sandbox pilots.

Meanwhile, Stripe, after launching Machine Payments (supporting x402) in February, has now decided to develop their own version of the 402 payment gateway from the ground up with MPP.

This means the race has just begun.

Battle against time

We know that the world of finance is moving onchain. Remittances, payments, trading, assets like stocks, equities, and indices are all moving onchain. In most cases, this shift is invisible to the end user.

And if the world is moving onchain, the case for agentic commerce protocols becomes self-evident. If we really want that to happen, we must create a system from the ground up that can accommodate both human actors and the growing number of agents.

The reason we’re seeing such a broad design space for agent commerce infrastructure is mainly a clash between two fronts: those who innately understand that the most suitable layer for the agent economy is the blockchain, and those who’re meeting users where they’re currently at.

In the short term, since the vast majority of consumers still use credit cards to pay for goods and services, products coming from Visa, Stripe, and Mastercard simply meet them there, requiring the least cognitive effort.

But simple agent-to-merchant flows are just the tip of the iceberg, and frankly, the easiest part to solve. Protocols like ERC-8183, ERC-8004, and x402 lay the piping for the new financial system. One that involves agents operating alongside humans.

It's not a question of whether crypto is necessary; it's a question of whether we can make it usable and prove that to the world fast enough to not end up where we started - with intermediaries controlling all the flows.

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)