Reading time: 8m 15s

Yield in DeFi used to mean serious double-digit numbers - 20%, 35%, and when it was straight up ponzi, six-figure APYs were basically the norm (printer goes brrrr).

That era feels extinct. DeFi yield today is mostly T-bill wrappers and other TradFi Trojan horses, leaving yield seekers asking, "What's the point?"

The yield keeps shrinking, vaults keep getting ransacked by hackers (April was scary), and the risk-reward has quietly inverted.

You're underwriting smart contract risk, custodian risk, and depeg risk to earn a yield that, after gas and slippage, barely beats what Jon Hamm in Your Friends & Neighbors would make if he were running a money market fund.

For example, three-month US treasury bills are currently yielding roughly 3.65%. Onchain tokenized treasury products have tracked slightly lower, posting a seven-day APY of around 3.4%.

Aave’s USDC supply rate on Ethereum has sat in the 3.7–4% range recently, while Sky’s sUSDS is offering approximately 3.7%.

Ethena’s sUSDe, one of the higher-yielding mainstream DeFi options, has been delivering around 5% lately, though this figure fluctuates with perp funding rates and carries active basis risk.

Yield farmers who once chased four-figure APYs on cat-themed forks are now arguing about 30 basis points of basis trade on a tokenized treasury. Something had to give.

Based on this premise, our eyes are turned to an unlikely yield source: Saylor’s newest financial product, STRC. In the next few paragraphs, we will look into what it is and how it’s being integrated into DeFi to form the core for improved yield offerings.

What is STRC?

Stretch (STRC) is Saylor’s strategy to keep up with massive Bitcoin buys. It is the fourth and most recent “preferred stock” issued by Strategy (MSTR), following STRK, STRF, and STRD.

In simpler terms, these are investments of sorts that sit between stocks and bonds - meaning that holders get a dividend, enjoy priority over MSTR holders in a situation where Saylor’s worst nightmare happens (Bitcoin down significantly), but basically have no real voting rights.

Each one (STRK, STRF, STRD, STRC) sits at a different point on what analysts have started calling Strategy's Bitcoin-backed yield curve, with STRC parked at the short-duration, high-yield end.

STRC currently pays an annualized dividend of 11.5%, distributed monthly. You buy it, Strategy takes your cash, buys more BTC with it, and pays you the dividend in cash every month.

STRC has a $100 par price, no maturity date, and a dividend rate that adjusts monthly to keep the share price anchored near $100. If STRC trades above par, Strategy can cut the dividend. If it trades below, the dividend goes up.

A number of yield-bearing stablecoin protocols have begun using STRC as collateral because it generates real, non-inflationary cash flow that can back a stable without relying solely on overcollateralization or ponzi-like incentives.

A key attribute of STRC is its reflexivity. What we mean by this is that it has a pretty great loop: STRC raises dollars, Strategy buys BTC, and if Bitcoin doesn’t flat-out rug, Strategy’s balance sheet is safe.

This, of course, leads to confidence in STRC driving more buys and a higher notional. With such a loop, DeFi steps in. Too juicy to ignore, eh?

Considering that this loop has funded the purchase of about 77,000 BTC in the first quarter of 2026, it is proof that it’s working.

What's left to see is how the STRC strat works for end users. We paint that picture in the next few paragraphs.

STRC tokenization layer: Who’s wrapping it?

We’ve identified three protocols pulling STRC onchain, turning a Nasdaq-listed preferred into programmable DeFi collateral. Let’s take a look:

xStocks

The RWA scene is booming, and though STRC is a hybrid TradFi asset, it attracts tokenized equity players like xStocks.

xStocks tokenizes the preferred itself, turning STRC into STRC-x, allowing users to hold the economic exposure onchain with minimal added mechanics.

xStocks provides a low-friction, high- transparency exposure without overcomplicating things.

They’ve partnered with Apyx to tokenize $50 million worth of STRC > STRC-x, bringing transparency to Apyx’s STRC holdings (users can see tokenized holdings onchain), and deepening liquidity for tokenized stocks.

Apyx Finance

Apyx says double-digit savings are for everyone. Well, they’re not wrong, these guys are 5.5k followers deep on X but are currently running one of the purest dividend-backed stablecoin models you’ll come across onchain.

On Apyx, users deposit collateral (heavily STRC plus other preferreds like SATA), mint apxUSD (the non-yielding stable), or lock apxUSD into apyUSD (which pays the underlying dividend stream).

So far, at peak, Apyx guarantees a median yield of 12.09% and an implied annualized yield of up to 17.2%, effectively turning Strategy’s cash payouts into programmable onchain money.

Apyx's strategy is high transparency, direct dividend pass-through, but you’re fully exposed to STRC or SATA dividend risk.

They’ve hit $125 million in STRC value, with apxUSD supply at a little above $230 million.

Apyx’s apyUSD is also now tranched on Royco, split into a senior and junior tranche.

The senior tranche is built for more conservative yield, pushing risks to the junior tranche while allowing users to farm apyUSD points.

The junior apyUSD tranche is more risk-welcoming, multiplying exposure to depeg losses from STRC and SATA, with a lot more yield as a result.

Saturn Credit

Saturn Credit takes a hybrid part T-bill collateral, part STRC approach. In this scenario, USDat is the base stable with lower risk, fully collateralized by tokenized US treasuries; sUSDat, on the other hand, lets you opt into the higher STRC yield slice that combines yield from Tbills and STRC base yield.

This setup appears to be a lot cleaner than the rotational plays in the sense that if you just hold USDat you have zero direct STRC exposure unless you choose it.

A pretty interesting setup with Saturn is its categorization of the yield products into senior and junior tranches.

Saturn’s in-house senior tranche product, srUSDat, is tailored to target 65% of the current STRC dividend rate with reduced yield variability. The yield is distributed from STRC shortfalls being absorbed by the junior tranche principal.

For example, a user accesses Strata markets (app.strata.markets) and selects a tranche; in this case, the senior srUSDat, proceeds to deposit.

The yield from STRC dividend accrues automatically to the position, while the protocol dynamically adjusts the split based on TVL ratios between senior & junior, underlying APY, and risk premiums to keep the system balanced.

On the other hand, Saturn’s junior tranche product, jrUSDat is an amplified STRC derivative exposed to higher risks.

The leverage layer (Pendle, Morpho, Spreads)

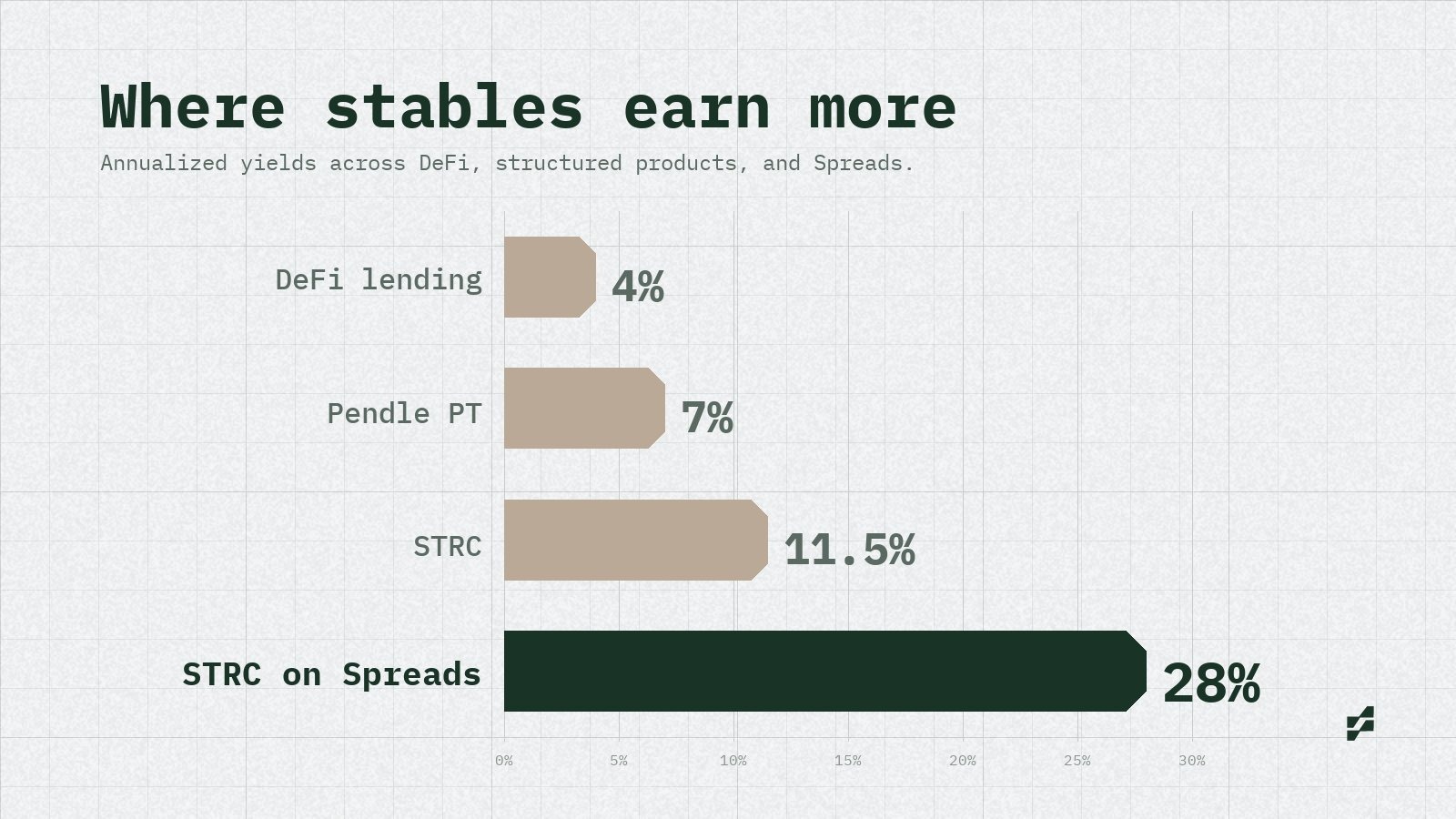

For players with a little more risk tolerance, leveraged products are available via the culprits Pendle, Morpho, and Spreads.

Starting with Spreads, a tokenized stocks trading platform, users can choose to lever up STRC-x, up to 3.5x for ~30% annualized yield.

Spreads make the user experience crisp through one-click deposit into levered STRC-x positions without having to cross the hurdles of looping for exposure.

On Pendle, tokenized STRC wrappers are split into PT and YT Yield Tokens. The former (PT) has traded at implied fixed rates in the 13–14% range recently (mostly driven by incentives, i.e. the points program).

Users can lock in a high fixed rate and walk away, or buy YT if they want leveraged variable exposure to dividend hikes.

On Morpho, users can borrow against tokenized STRC collateral and loop. Bluechip lenders love the cash-flowing collateral, so loan-to-values stay healthy. Users borrow stablecoins, buy more tokenized STRC, repeat.

Here’s a clear example of this playing out:

User deposits, say, $50k into a Pendle-wrapped STRC position, splits into PT and YT, then uses the YT on Morpho for 2–3x leverage. Base ~11.5% becomes ~25% APY net (after borrowing costs) in a stable dividend environment, basically separating yield from volatility and depeg exposure. In exchange, they get amplified cash flow that compounds.

Users can choose to leverage STRC up to 3.5x on Spreads, a tokenized stocks trading platform.

This brings us to the next consideration, the risks.

What’s the catch, Ollie?

Ayyy, if you’re anything like me, big yields must scare you. Some weird wiring must be under this, innit?

You won’t be wrong because STRC yields do come with risks.

Firstly, STRC itself. There are possibilities of volatility via dividend cuts or risks through sustained depegs. In November, STRC dropped to $90.52, and a few months earlier, volatility triggered STRC to fall to $93.10.

The point is, the $100 floor is not ironclad; it’s defended by dividend policy.

A few paragraphs above, we painted STRC reflexivity as some cool thing. The truth is that it can also make you wet your pants, while Saylor posts his 100th AI-generated underwater image that drives you nuts, if you’re neck deep.

Dividends are ultimately funded by new capital raises and the strength of the BTC treasury strategy. If Bitcoin enters a prolonged drawdown, Strategy may have to issue more equity at unfavorable terms or cut payouts.

Additionally, these new protocols are yet to go through a proper stress test. Like most DeFi protocols, they are nowhere near a too-big-to-fail level. They are, as a matter of fact, susceptible to smart contract vulnerabilities and other risks that could put a user in a frustrating redemption queue, in panic mode, and yelling wtf is this [****].

How to play it?

If your balls are tingling and you want to play, here’s a snapshot of how participants are currently positioning.

Remember that this is still pretty much early and with a lot of risks.

For the cold feet, “I don’t want to get hurt, folks,” you could hold a base wrapper like apxUSD or USDat. The latter gives you access to roughly ~3-5% yield (before fees) from T-bills, with relatively straightforward exposure, while the former (apxUSD) earns you a higher points multiplier, accruing more points than you would if you were to lock your apxUSD for apyUSD.

The main trade-off here is custodial reliance, but you avoid the complexity and liquidation risk that comes with leverage.

If you’re feeling a little more ballsy, you could use Pendle principal tokens (PTs) to lock in a fixed yield. Rates north of ~13% are available depending on the market.

This route is popular for those who prefer certainty. Users commit capital, secure the rate, and don’t actively manage the position.

If you’re wild like Lorna from JPMorgan (was a farce, btw), the path to go is clearly via YT or looping strategies through Morpho that can push returns beyond 25%.

Be careful now, you dirty chad! You’re now exposed to variable yield dynamics and underlying asset risk (including BTC-linked performance in some cases). The returns are higher, but so is sensitivity to market changes.

Wrapping up

Like The Rock, it’s hard not to “smell what’s cooking” here. Preferred stock–driven yield streams like STRC have the potential to become a more transparent and competitive alternative to inflationary yield.

That said, the opportunity doesn’t exist in a vacuum. A large part of the thesis depends on Michael Saylor sustaining his ability to continuously raise capital at scale. Smell the (un)certainty, fren.

For now, STRC stands out as one of the clearest and most compelling yield sources in the space. But it’s not something to passively trust. That said, you better watch out for these five signals:

- Persistent trading below par value

- Any change in the trajectory of dividend growth

- Any sign that Strategy’s cash balance is falling too low

- The balance between the tokenized supply and the actual circulating float of STRC

- Donald Trump

If any of these start to drift in the wrong direction, it’ll become a race for the door, and boy, do I have news for everyone in this hot-damn industry.

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)