.webp)

Reading time: 6m 44s

Somewhere in downtown San Francisco (no idea why that location), someone’s dad is uttering these exact same words:

“Oh, Jimmy? Yeah, he’s good! You know, he makes money online.”

The popular boomer phrase for explaining the internet stuff their child is into that they just never seem to understand, so they can escape saying they’re unemployed.

In the history of the internet, there are two industries that are familiar with this exact experience - those teaching people how to make money online and the left-forsaken crypto bros.

But in a weird turn of events, these two are being aligned in a way like never before to create what might truly become the most unlikely multi-billion dollar company in the world, and not just that, but also the eventual means through which crypto finally achieves that thing called “mass adoption.”

If you haven’t figured it out yet, we are referring to Whop.

What is Whop?

Before we get into the rudiments of why Whop is so important to crypto, let us set the scene.

Whop is designed as the one-stop shop for e-commerce and internet-native business formations, offering its own chat, forums, courses, live streaming, file hosting, and an App Store.

The founders, Steven Schwartz and Cameron Zoub went from building software to cop limited-edition Nikes to failing at four startups together (respect), before launching Whop in 2021.

The platform has since grown into 21 million+ users, over $3 billion in annual payouts flowing to creators across 144 countries, and a valuation that recently hit $1.6 billion.

Whop’s user base cuts across sports bettors selling picks, crypto traders with signal groups, sneaker resellers with cook groups, course creators, SaaS founders, clippers, and every flavor of digital hustle in between. It's the internet's informal economy, formalized.

However, what we find interesting about Whop is the direction it’s taken in 2026 in terms of partnerships and integrations, nothing less than strategic to become a full-stack app for internet-native businesses, handling formation, payments, and even yield!

Whop x Tether

A few weeks ago, Whop announced an investment-partnership with top stablecoin company, Tether, to the tune of $200 million.

As part of the deal, Whop is integrating Tether's Wallet Development Kit (WDK), which means users can hold and transact in stablecoins like USDT and the newer USAT (a US-focused digital dollar) directly on the platform.

Creators get the option to accept stablecoin payments and settle globally.

All things considered, this single integration introduces the concept of stablecoins to 21 million+ people.

But it didn’t stop there.

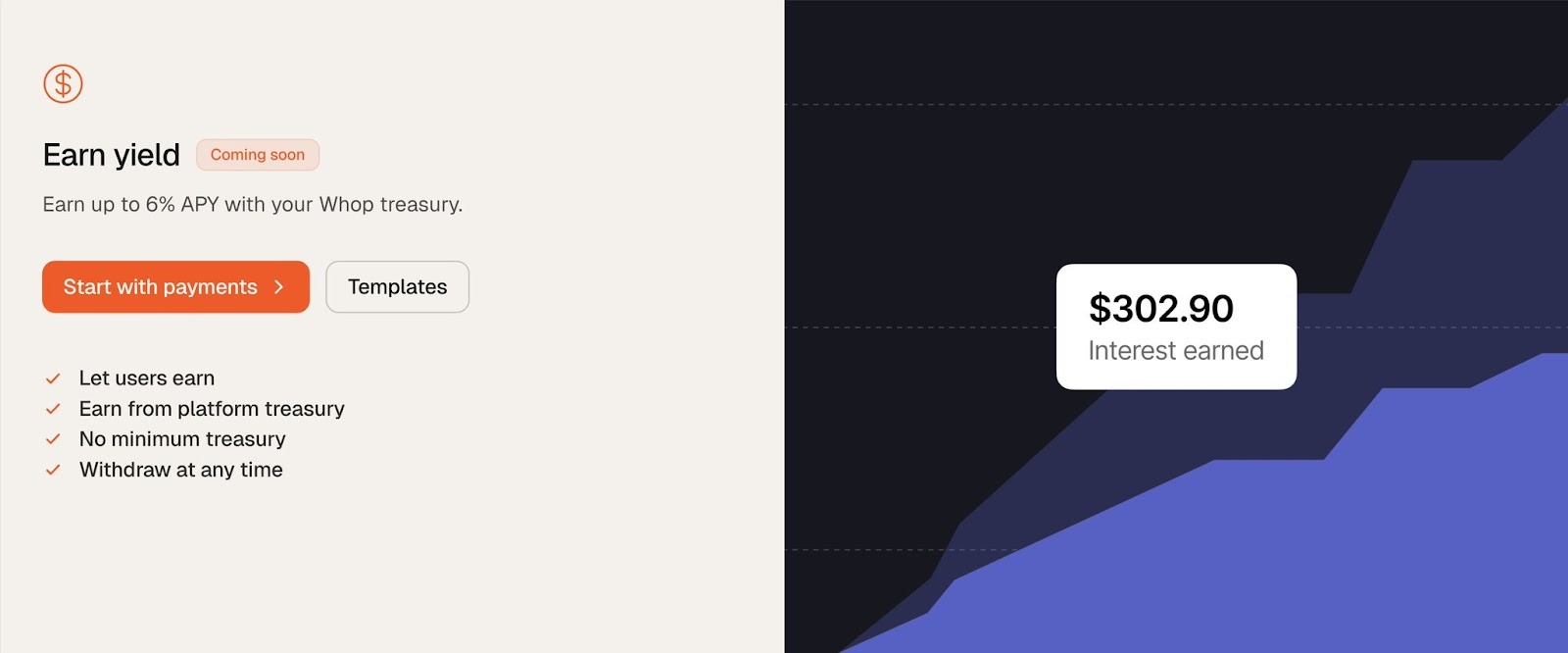

Whop Treasury

We believe that the Tether investment was the horse entering the city, and the Whop Treasury is the soldiers climbing out at midnight.

Whop Treasury is, and we're not being dramatic here, one of the most significant DeFi integrations into a mainstream consumer platform that we've ever seen.

Here's how it works.

When a Whop user opts into Treasury, their balance gets converted to USDT0 stablecoins (issued by Tether).

Those tokens get routed through a Veda Labs vault operating on the Plasma network, purpose-built for efficient, low-cost stablecoin transfers.

From there, the capital flows into Aave's lending markets, where it earns yield automatically. The whole thing autocompounds, meaning returns get continuously redeployed without the user paying gas fees or managing any positions.

Deposits come in through MoonPay, so users can fund their accounts with a card or crypto.

In short, you click a button, and your Whop balance starts earning roughly 6% APY. That's it.

To put the scale in perspective, Aave V3 on Ethereum has around 200,000 total daily unique users. Whop's user base is 100x that.

The vast majority of those 21 million users have never interacted with DeFi, never heard of Aave, and couldn't tell you what a lending protocol is if you offered them 6% APY to explain it (which, ironically, is exactly what they're getting).

Merchant-side checkouts

Whop has also made it easy for users to receive payments in crypto through its flexible merchant-side checkout infra.

It is built on two core options: checkout links and embedded checkouts. For users who want simplicity, the former offers the easiest way to receive payments.

Creators can simply set up a plan (one-time payment or recurring subscription), and Whop will proceed to generate a shareable URL that the merchant can paste on their page, send directly to a customer, or put in their bio.

However, relevant to our discourse is the integration of Tether’s WDK to support stablecoin settlement, allowing customers to pay merchants with USDT, which settles instantly onchain.

Whop also supports the full spectrum of TradFi payment methods, including crypto. This integration allows creators to bypass complex fees on most of these traditional payment services.

Why is this different from every other "mass adoption" play

Every cycle, someone announces a partnership that's supposed to bring crypto to the normies. "PayPal now supports Bitcoin," "Visa settles in USDC," "Starbucks accepts crypto through whatever!”

And yet, every time, the adoption numbers underwhelm because, at the end of the day, they're bolting crypto onto an experience that already works fine without it.

Whop is different. The crypto rails are the foundation. They're rebuilding their entire financial stack on stablecoin infrastructure. This covers payments, settlements, yield, and treasury management.

This matters because Whop's users aren't early adopters or crypto enthusiasts. They're creators who sell courses about dropshipping, sports bettors running Discord groups, and SaaS founders in Accra and Salvador who just want to get paid without a bank taking a 5% cut.

When their Whop balance starts earning 6% through Aave, and their payouts settle instantly through stablecoin rails, they're not going to ask how. They're just going to notice that the old way sucked and this way doesn't.

That's the playbook for real adoption. Not "here's a wallet, go figure it out," but "your money already works better, you're welcome."

Besides, crypto has always had a distribution problem. We build incredible financial infrastructure, and then we expect regular people to navigate through the turds of our native setups like, “Hey! Go bridge across four different chains.”

Agents may solve a part of our distribution problem, but stuff like Whop solves this for the human-facing distribution layer that DeFi has been missing.

Lastly, talking about agents, Whop has also leaned into AI agents to drive even further growth.

Whop users can basically build businesses, spin up agents to run them, utilize the Whop tool suite, and interact with everything we’ve mentioned above by just putting in a prompt or a few prompts. Can’t deny that the lads are absolutely cooking here.

What comes next?

The platform is also building out lending and borrowing features powered by DeFi infrastructure, essentially creating a self-custodial banking layer for creators.

Considering how fast they’re shipping, we’re certain that it’s gonna be a record-breaking short breath hold before users can spin up businesses on Whop, manage communities and growth with tools provided, settle in stablecoins, earn yield on proceeds, and earn more yields by participating in DeFi without even knowing that crypto powers half of that entire flow.

Whop vs. Stripe

Anyone monitoring the situation knows Stripe is also firing on all cylinders with integrations and partnerships that covertly drive crypto adoption.

And if you’ve read this far, you must’ve also said, “Doesn’t Stripe do the crypto payments thing, too, and is by magnitude a far larger company?”

Yeah right! But Stripe and Whop are playing completely different games, even if they’re both sneaking stablecoins into the mainstream.

Stripe is the top-down play engendering institutional, invisible adoption of stablecoins. Merchants accept USDC through wallets or on-ramps, get instant fiat settlement in their balance, and never have to think about all of the wiry stuff.

With Tempo, Stripe is optimizing for sub-second, programmable payments, tilting towards efficiency and reliability in processing onchain transactions.

Whop, on the other hand, is the bottom-up play. Whop is creator-led and fundamental, building an entire house for end-to-end e-commerce activity with crypto layered at the foundations.

Whop has transformed into a merchant of record platform that handles pretty much all the annoying stuff with selling or running a business online, while making crypto a path of least resistance, especially for businesses domiciled in emerging markets.

Both Stripe and Whop fit into the Trojan thesis, silently doing the painful distribution work for crypto’s flaccid distribution setups. It’s a thing to be thankful for and a huge relief for the industry.

And hey! For what it’s worth, we’ve been ardent believers in the invisibility of crypto as adoption rages. In fact, we believe the trait that has made DeFi and crypto successful is that they have quietly become the layer that powers finance, businesses, transactions, social networks, and, basically, the internet.

Concluding thoughts

For years, the crypto industry has been asking, "How do we get the next billion users?" And for years, the answer has been some variation of: build better wallets, simplify UX, educate the masses.

All valid.

But Whop suggests a different path entirely that simply requires bringing crypto to where the users already are.

We believe that Whop is the tip of the iceberg and probably the major indicator that crypto is finally ready to disappear into large consumer products, which are undoubtedly the perfect Trojan Horse for its global adoption.

The future this brings to the kids is one where Jimmy's dad might still be confused about what his kid is up to these days. However, it will also be one where he isn’t just “making money online” but is also unknowingly using DeFi as a bank.

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)