Reading time: 12m 36s

When I was searching for the definition of a neobank, most of them sounded something like this:

Neobanks are digital-only banks that operate primarily through mobile apps and websites. They offer financial services similar to those of traditional banks, including savings and checking accounts, loans, and payment and money transfer services.

Well, damn, if that’s the case, most of what CT calls a neobank simply isn’t one.

And I’m not a generational hater or anything. As a matter of fact, I’m an avid user of them myself. It’s just that the word “bank” isn’t really fit for most, is it? Perhaps 10 years later, when everyone is using stablecoins, that’ll be the case.

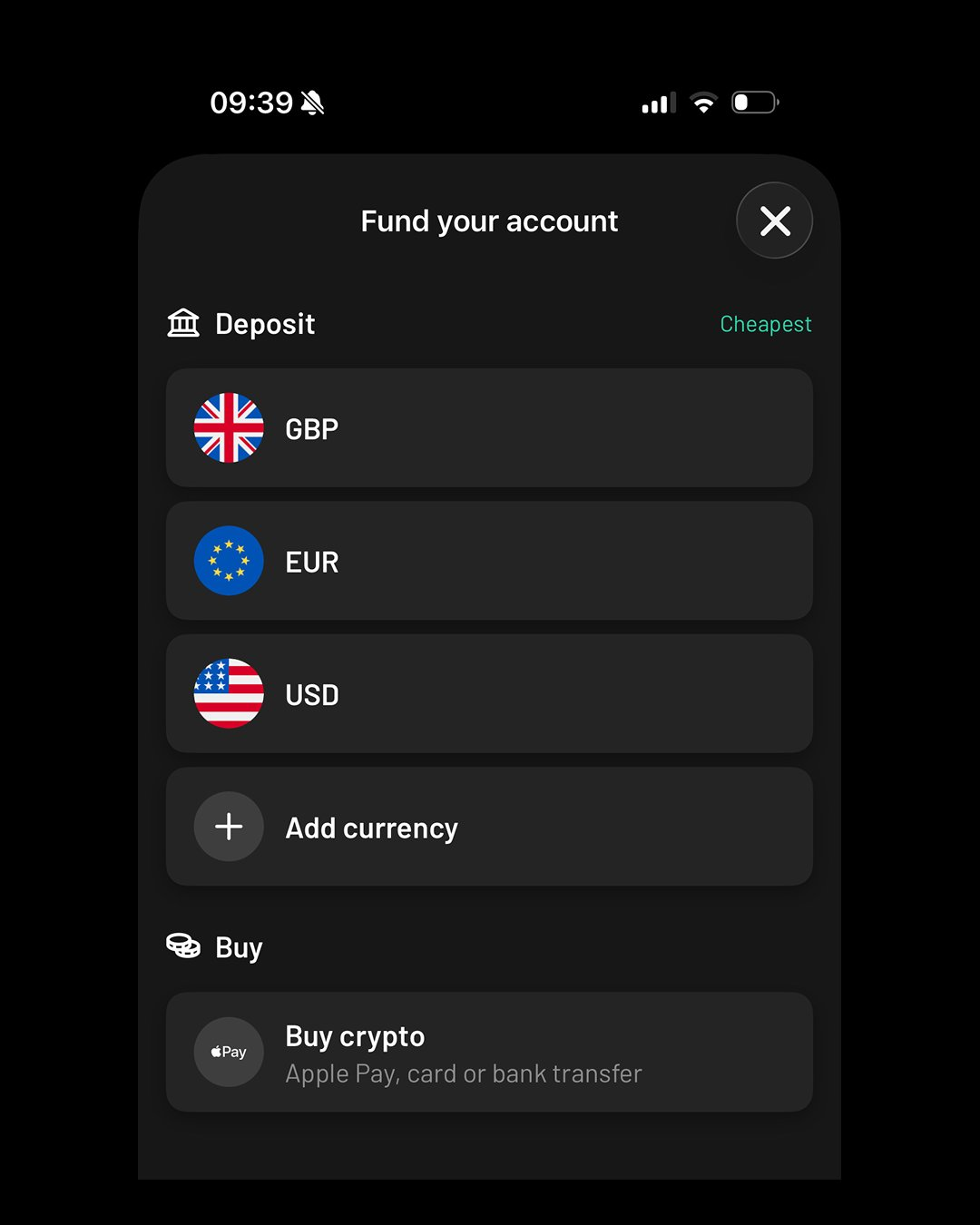

For now, the key missing link for most is the connection to traditional banking rails, think virtual IBANs, ACH/routing numbers, SEPA transfers, direct bill pay, and savings/investment opportunities. Basically, an app that can replace your everyday banking needs.

Because if we ever dream of competing with the likes of Revolut or NuBank, who, by the way, are already integrating crypto for payments and savings, these features are a must to attract users.

With that in mind, here’s how the neobank sector looks today.

The neobank sector at a glance

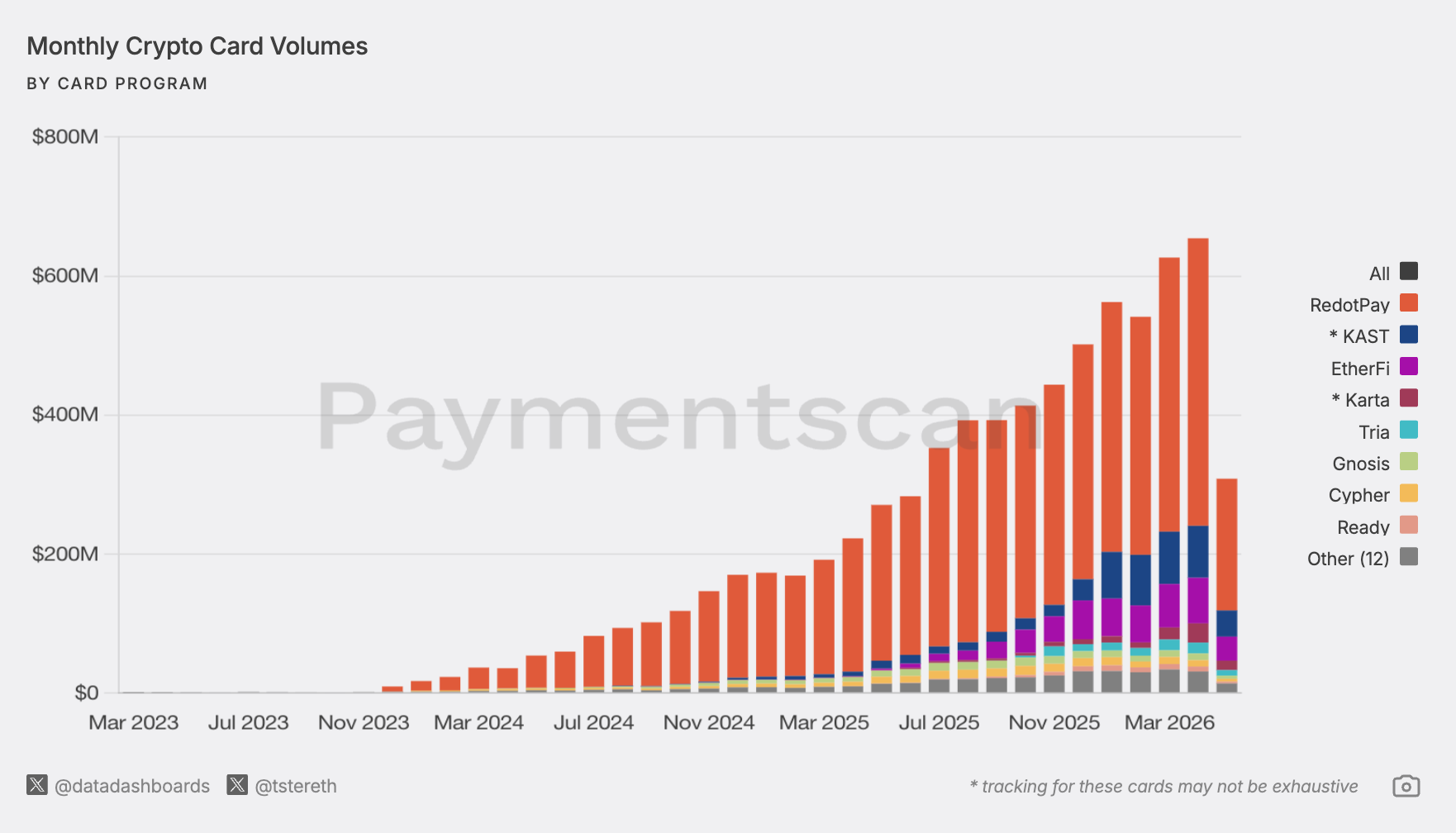

Although I don’t believe a crypto card alone qualifies an app as a neobank, it's nonetheless the central product. And boy, have people been spending lately.

Last month saw the highest spending ever, totaling $665 million. I thought we were in a bear market?

It’s important to note that a crypto neobank isn't a single, uniform product. Instead, it's a blend of various infrastructure providers, solutions, and features that differ based on the jurisdiction in which it operates.

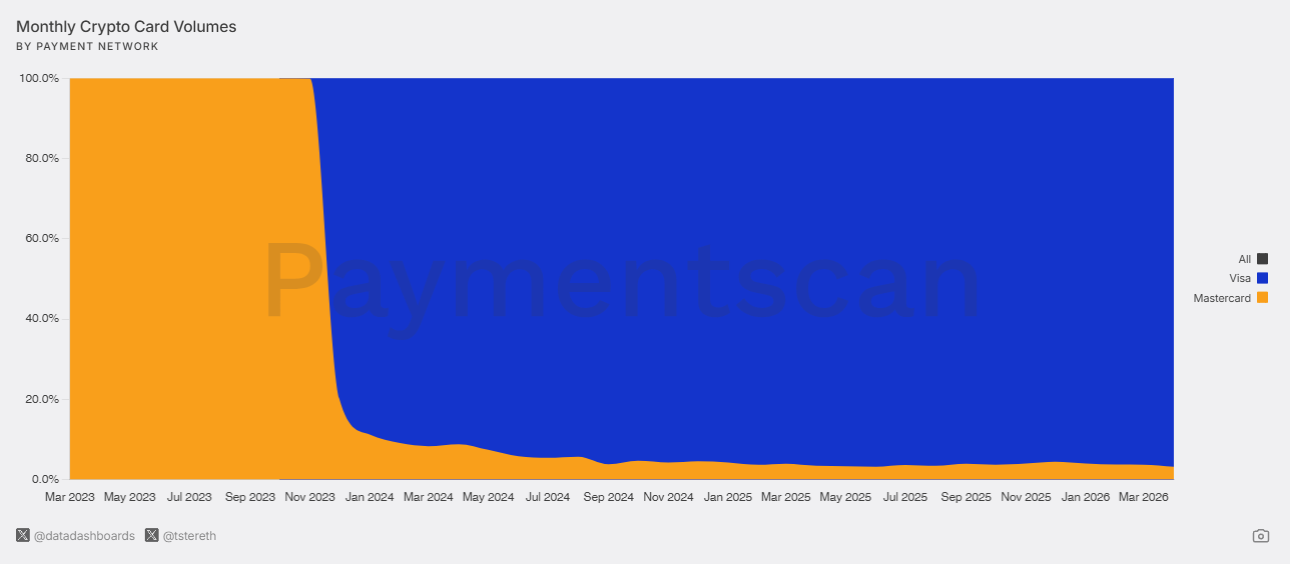

Two core pillars anchored in traditional finance enable these neobanks to offer spending: the card network (Visa or Mastercard) and the card issuers (companies authorized by those networks to issue cards).

If you're like me and have used multiple crypto cards, you probably already know this anecdotally, but Visa's branding is visible on almost all of them, and the data confirms that.

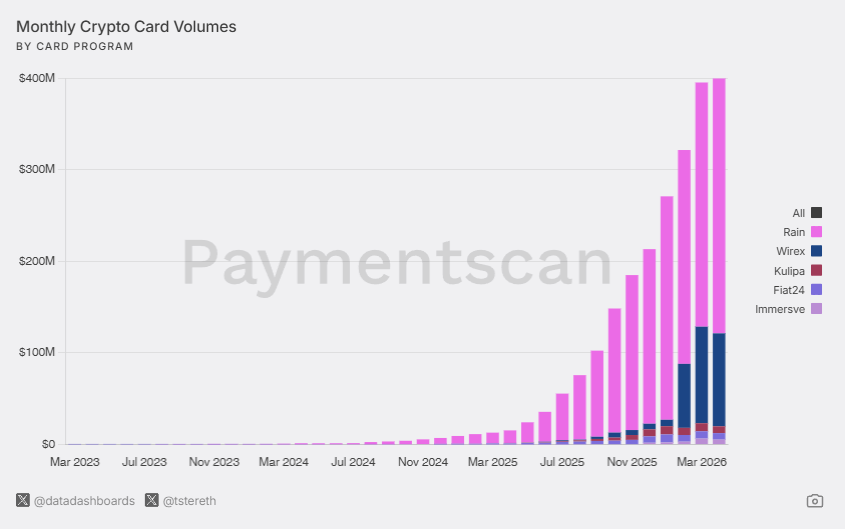

When it comes to issuance (entities that work directly with Visa or Mastercard to issue cards for user-facing card programs), Rain takes the crown as the undisputed champion, with roughly 7 out of 10 neobanks today using it to offer this feature.

Regarding the specific apps and their cards, the data varies greatly between sites. Understandably so, since each product's underlying operation can differ, making what qualifies as a “spend” quite subjective.

For instance, some card issuers use centralized or batched settlement systems, which can't be directly compared to those that record each payment with a separate onchain transaction.

Either way, there is a cohort of cards that consistently appear at the top in terms of spend volume: RedotPay, EtherFi, and Kast.

But thanks to advancements in infrastructure services that enable the rapid deployment of financial solutions such as on/off-ramps and virtual bank accounts, many competitors have entered the market in recent months, each adopting a unique strategy to attract users.

Some bank on exclusive, physical metal cards; others on membership perks, and then there are those that offer a Claude Pro subscription in their program.

The race is on.

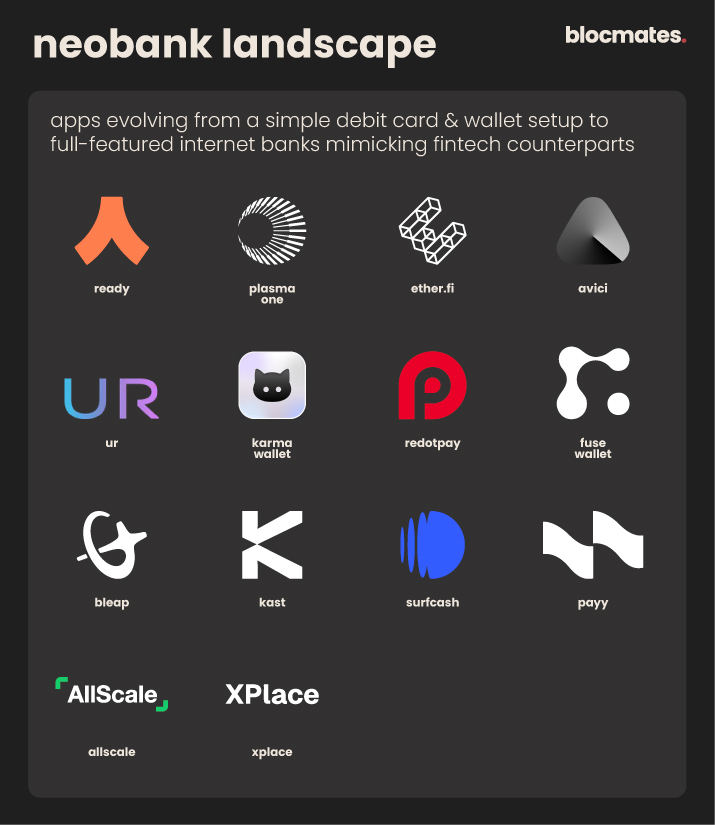

Internet banks in 2026

Avici

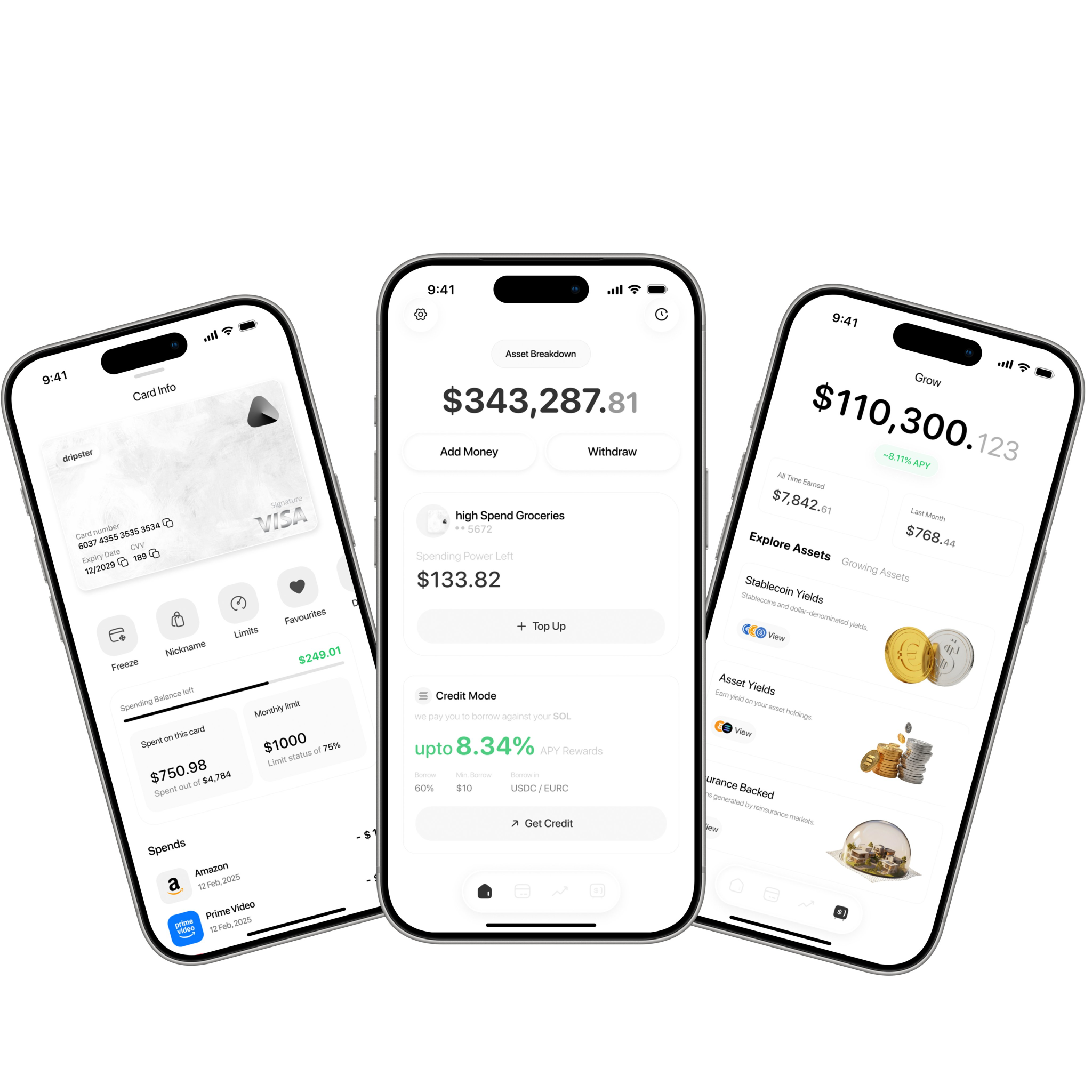

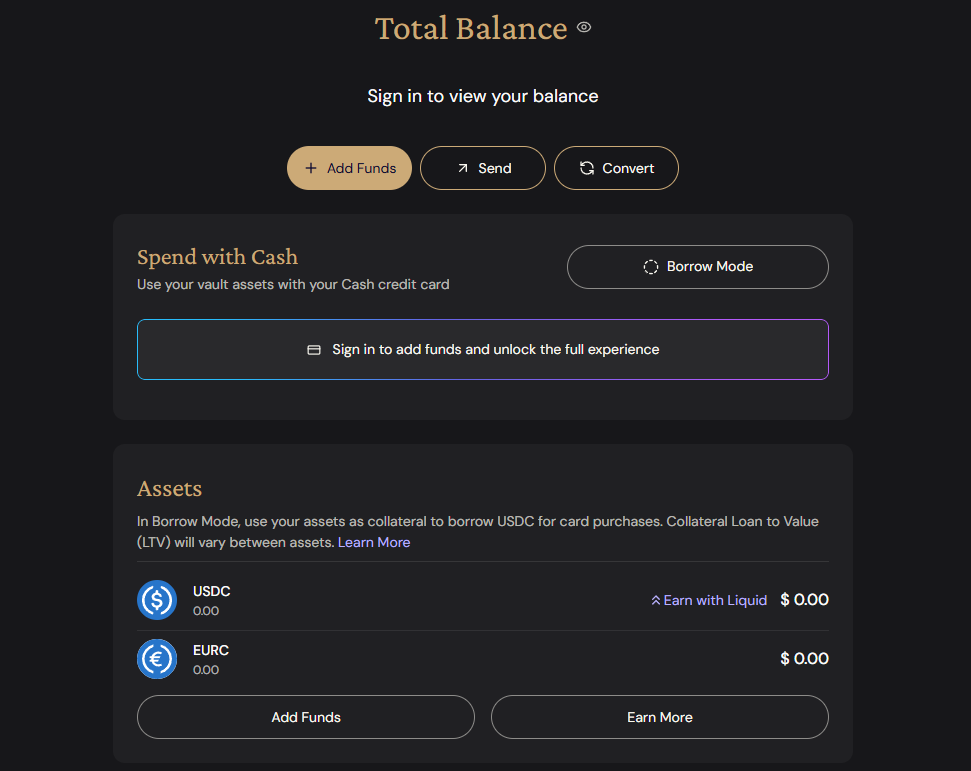

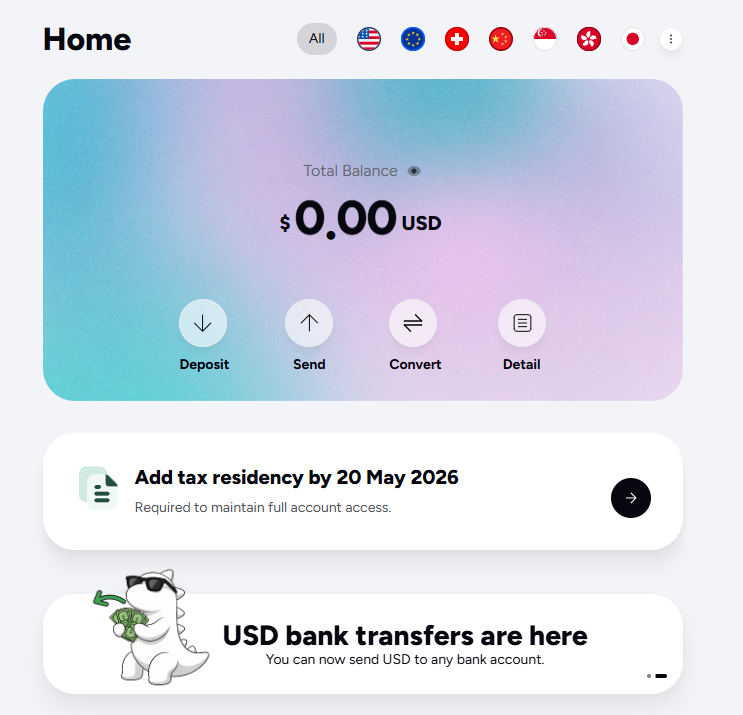

You know we’re ownership coin bulls here, so we’ll start off the list with @AviciMoney, aka the people’s bank. When we last spoke about it on our previous Neobank report, Avici was still raising money via MetaDAO.

Avici has come a long way since. Today, it boasts of one of the most extensive feature sets, including virtual USD and EUR accounts, a savings section offering yields on stablecoins and assets such as wSOL, and even a reinsurance product (with OnRe) called ONyc.

Additionally, users can open a credit line against their SOL holdings and get paid to do so.

Furthermore, Avici recently announced the launch of trading for equities and pre-IPO companies through partnerships with xStocks and PreStocks.

RedotPay

@RedotPay commands 60-80% of global crypto card volume, depending on which source you look at.

What’s funny, though, is that it seems like no one on CT really uses it or knows anyone who does. If the numbers are true, one thing is proven - appealing to the terminally online crowd is not a prerequisite for launching a successful business.

The app features include crypto-to-fiat payments, a P2P stablecoin marketplace, a modest Earn tab with two stablecoin strategies, and a credit mode allowing users to spend without selling.

However, given that they’ve raised $194 million across three rounds, I honestly would’ve expected more. Plus, the card fees are quite hefty: 1% is added to every transaction, and there's a 2% ATM withdrawal fee.

Nonetheless, it’s apparent that Redotpay is the number 1 option for most crypto natives in the eastern hemisphere.

EtherFi

@ether_fi originally launched in early 2024 as a liquid restaking protocol on Ethereum. Not long after that, they introduced their Card product.

Today, EtherFi is known for boasting among the highest usage and spend metrics across all crypto cards, with numerous tiers based on points earned from how much you spend and for depositing in either the Liquid or Stake Earn strategies.

Across all tiers, users receive 3% cashback, global wire transfers, exclusive hotel discounts, on/off-ramps to USD or EUR accounts, yield opportunities on BTC, ETH, and USDC, and the option to use credit mode, where instead of spending your crypto, you borrow against it.

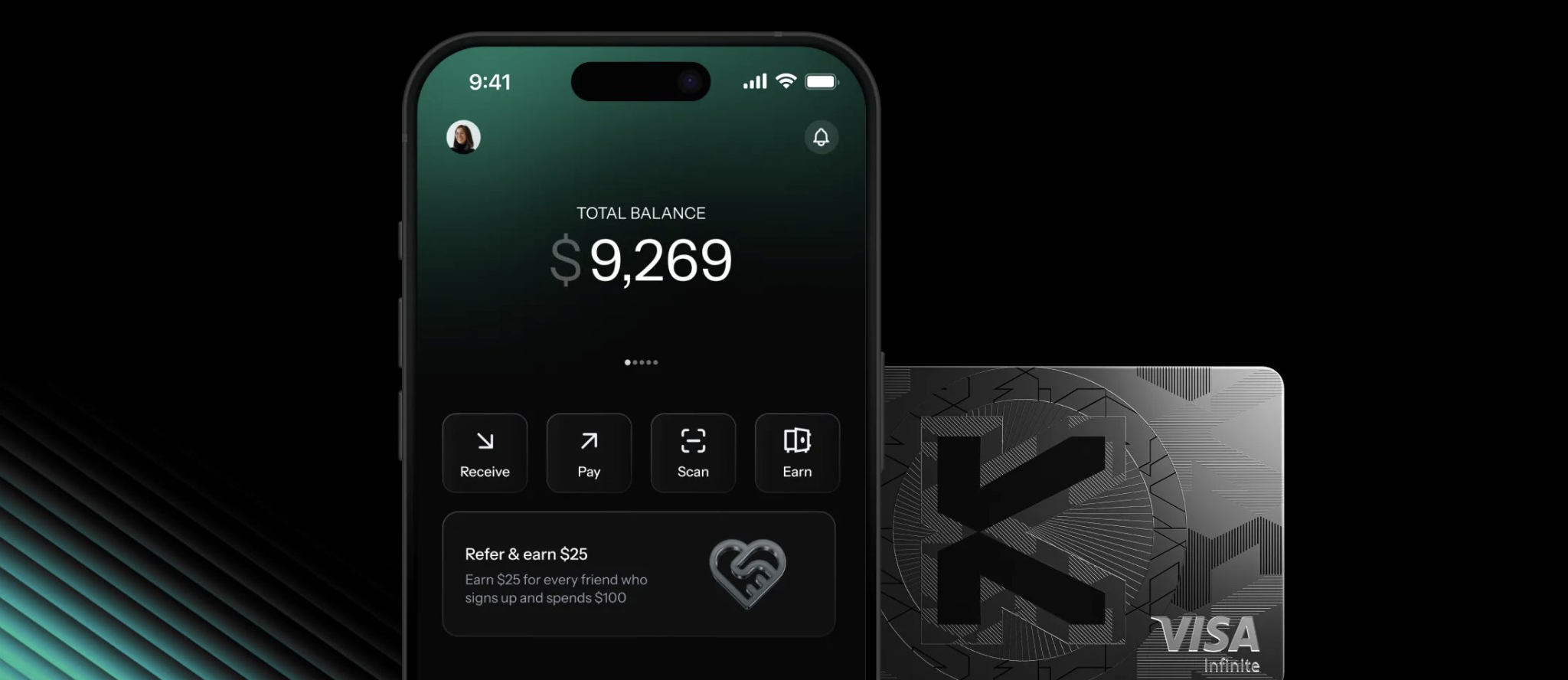

Kast

Launched in the same year as the previous player, @KASTxyz is another heavyweight in terms of spend volume.

The app features a virtual USD account, two Earn vaults, a dedicated pay section with payouts to EUR via SEPA, USD via SWIFT, and a vibrant mix of exotic currencies, such as IDR (Indonesia), VND (Vietnam), PHP (Philippines), THB (Thailand), MYR (Malaysia), NGD (Nigeria), and TRY (Turkey).

For such a well-funded neobank, having raised $90 million across two rounds, I would like to see more features already available on smaller competitors, such as credit mode, more Earn opportunities, and the ability to on-ramp from a bank account.

As for the card, Kast has both physical and virtual cards with three tiers: K Card, X Card, and Solana Gold card, with 1%, 4%, and 6% cashback, respectively. Oh, and did I mention you can order a Physical Pengu Card? How awesome is that?

But the standout feature Kast is known for is its unlimited spending limit on its cards, which has undoubtedly attracted the wealthiest of Solana memecoin bundlers.

Plasma

When Plasma originally announced the product back in 2025, it quickly became the central talking point in the newly forming neobank sector. After months of development, the app is finally landing in people’s hands through invite codes, with a full public rollout slated for June.

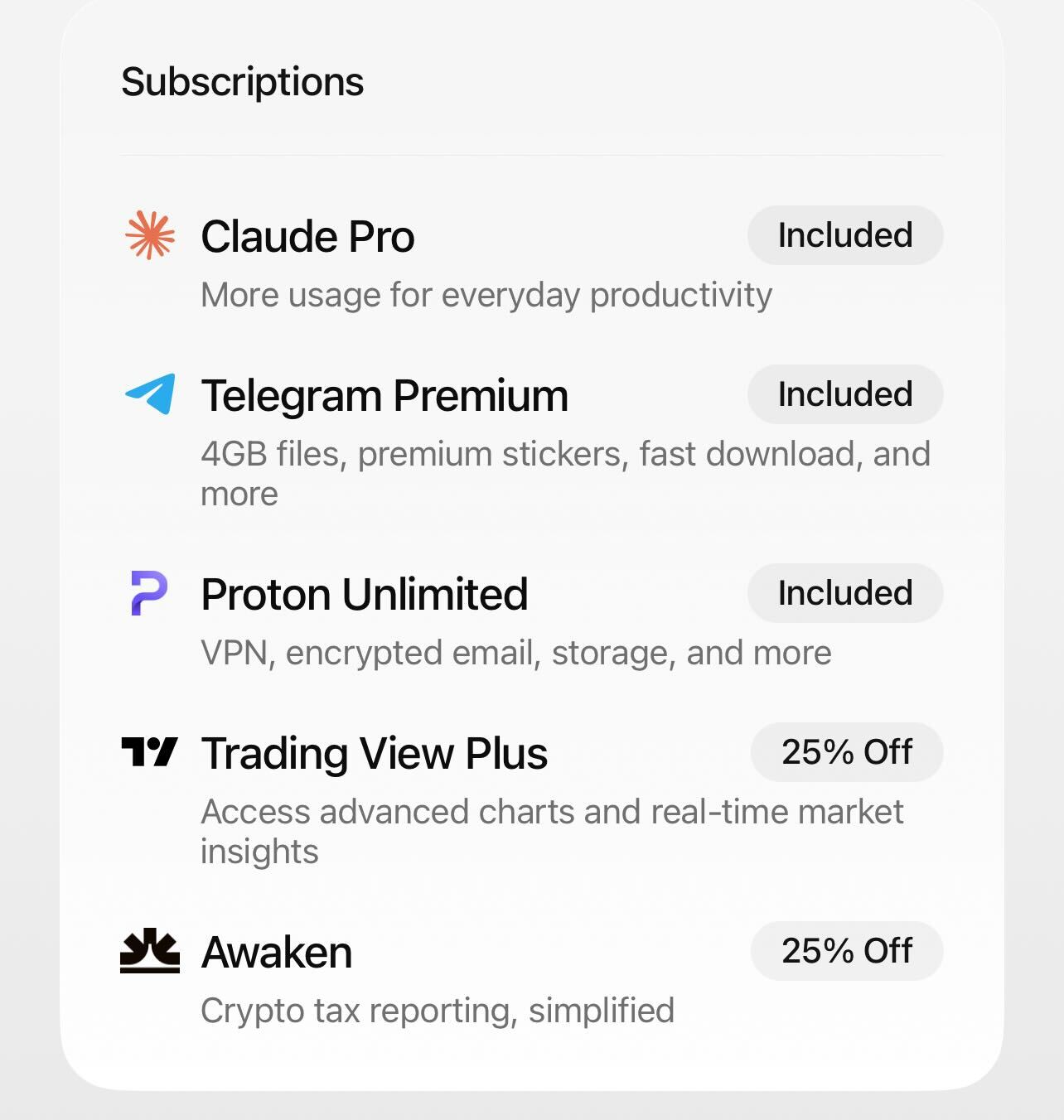

@Plasma lets you pay with stablecoins and offers 3% cash back with no FX or monthly fees. Once it launches, the Platinum card will take this to a whole new level with a 19-gram metal card, boosted Earn yields, 10% Uber cash back, travel perks, and, hear this, benefits like a Claude Pro subscription, Telegram Premium, and Proton VPN included.

Other noteworthy features include zero-fee USD₮ transfers and the imminent arrival of virtual USD and EUR accounts, which I suspect will be live by the time the public gets their hands on it.

Undoubtedly, some of you are on the lookout for codes Just shoot us a DM on the blocmates main Twitter and we’ll give you one. FCFS, so don’t miss it!

Ready (formerly Argent)

What started as a browser wallet, @ready_co has pivoted to building a crypto alternative to your bank.

Though the connection to the fiat world is currently limited to bank deposits, which are auto-converted to USDC, Ready offers an Invest section that provides yields on USDC, Ethereum, STRK, and Bitcoin, as well as the option to borrow against Bitcoin with no fixed term.

As for the Card, Ready has two tiers: Lite and Premium. The Premium tier costs $10 per month and offers 3% cashback (in points), no FX markup, and free ATM withdrawals.

On top of that, the Premium tier includes perks like “Ready Travel,” with discounts on hotels, as well as discounts on Claude, Spotify, Netflix, NordVPN, Nansen, Koinly, and others.

UR Global

@UR_global is one of those apps that genuinely resembles a fintech neobank, offering a regulated, multi-currency Swiss bank account with a personal IBAN, along with self-custodial stablecoin balances.

The account holds balances in seven currencies: USD, EUR, CHF, SGD, HKD, JPY, and RMB. Users can seamlessly move between fiat and crypto, perform FX conversion with an on/off-ramp at 0% fees (for Pro users). UR currently offers one Earn strategy for users holding USDe on the Mantle Network.

The features I appreciate most include a unified account balance that covers both stablecoins and fiat currencies, and the ability to send and receive money directly with other UR users.

As for the debit card, the unified account balance also applies, allowing you to settle transactions in fiat or stablecoins, whichever is available on your account at the time.

Recently, the company has shifted its focus from the app to becoming a B2B provider for other fintechs, although yours truly has confirmed that the UR app is still available and will be maintained.

It is now positioned as the account layer serving wallets, developers, and financial platforms globally, offering Swiss IBAN, 7 currencies, SEPA, SWIFT, Mastercard, and compliance, all through a single API.

Bleap

@BleapApp is a self-custodial neobank founded by two former Revolut employees.

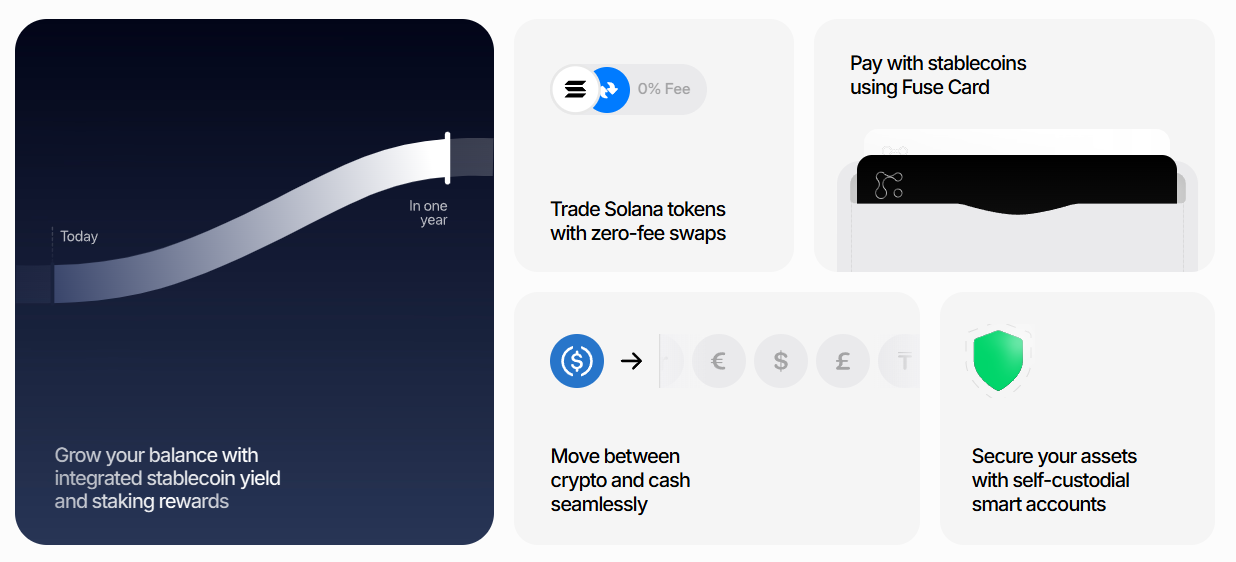

Bleap puts everything you need in one powerful app. On the crypto side, users can trade 18,000+ tokens across 8+ chains with no fees, deposit money, and a bridge function on the way.

On the fiat front, the app supports deposits and withdrawals in euros or dollars to a bank account, and seamless movement in and out of crypto or fiat directly on the app.

What I like most is the focus on transfers, allowing users to send stablecoins or fiat to other Bleap users, with the option to import contacts. A feature that lets users pay anyone via simple links is also on the way. It’s clear these guys were working at Revolut.

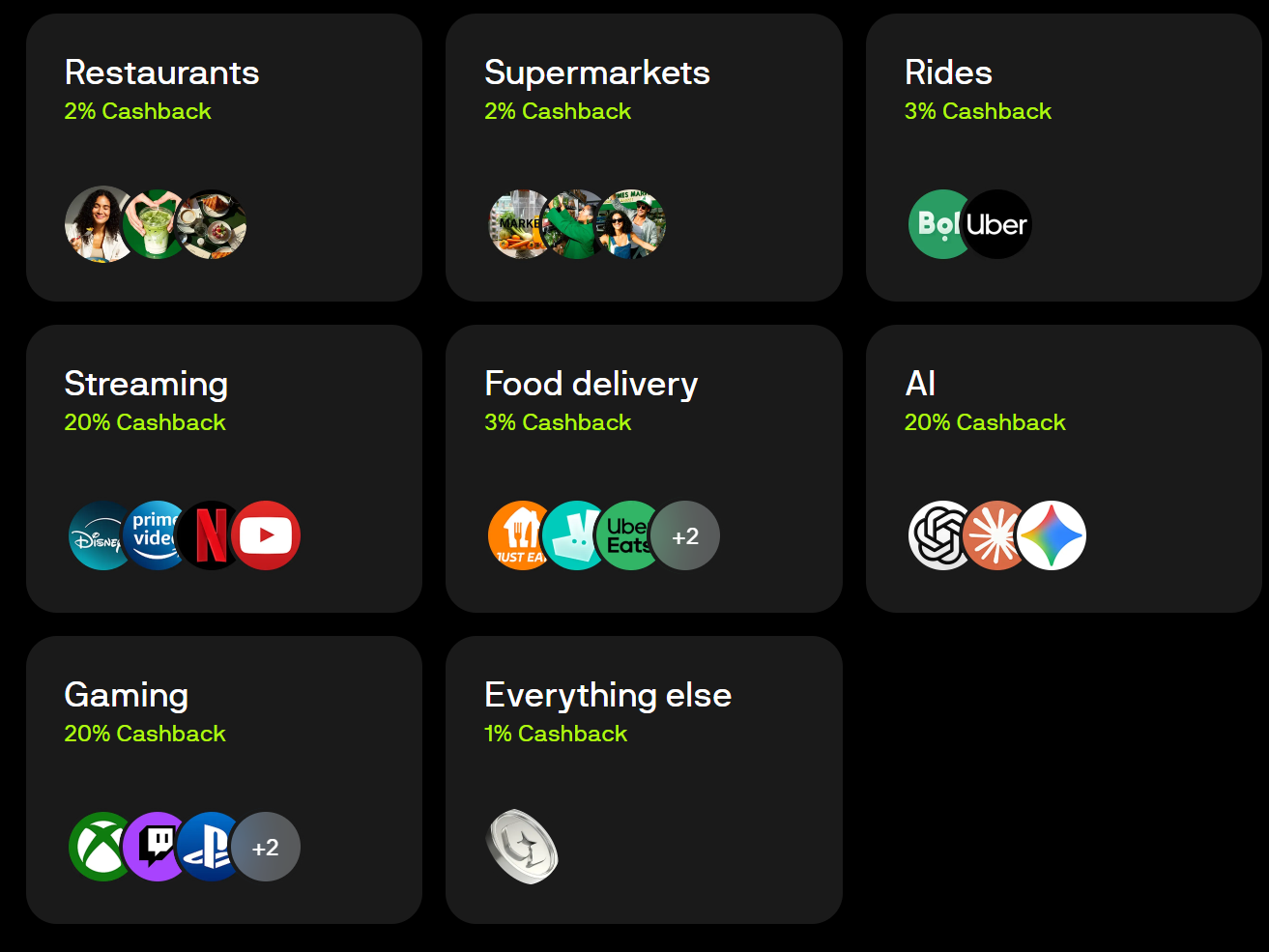

The debit card features a compelling cashback program that offers higher rewards at frequently used merchants and services. It provides up to 20% cashback on specific expenses, including AI subscriptions, car sharing, delivery, gaming, and streaming services.

Fuse

Launched by the team behind Squads Labs, Solana’s leading multisig solution, @fusewallet is a neobank that fuses crypto with TradFi by offering virtual USD and EUR bank accounts that automatically convert stablecoin balances to fiat and vice versa.

The app supports only Solana and currently offers one Earn vault and swaps for SPL tokens.

Similar constraints also apply to their card program, which offers only a virtual debit card and is available in select regions, with support mainly for the Americas and a few African countries. Asia and the EU are not supported at all.

Where the app does shine is in security. Fuse is built on programmable smart accounts (Squads) that offer advanced security features such as two-factor authentication, recovery, spending limits, and key rotation.

Karma

@KarmaWallet, another Solana-native neobank with the slogan “Spend money, earn good karma,” offers the essential features I consider the minimum viable product for a neobank.

Featuring a Visa debit card with fiat on/off-ramps with support for SEPA and ACH, users can move in and out of crypto.

Although an Earn tab is not available at the moment, one feature that stands out is the recently announced multi-wallet support, which lets you import multiple wallets and assign each one a unique IBAN.

Karma features two cards, Signature and Black. However, the benefits depend on how much $KARMA you stake and your tier (Seed, Rising, Elite, Black), with cashback up to 25% for the Black tier.

XPlace

@xplaceapp is a product that hasn't received much attention on CT but deserves to be discussed. Dubbed as Solana’s first genuine credit card, XPlace is a non-custodial neobank offering a global bank account with IBAN supporting USD, EUR, and BRL, a yield hub, and a credit mode.

Unfortunately, since the Drift exploit, both the credit mode and yield features have been suspended. However, judging by their comms, they should relaunch them soon, with Kamino powering them.

The app offers multiple membership tiers, each with different benefits and fees. For instance, the Silver Club membership, priced at a flat $200, allows a $10,000 monthly limit and charges a 0.5% FX fee and a 1.5% fee on bank transfers. The same tier includes perks like a 1% USDC cashback and 3% XP cashback.

For those looking for a stimmy or at least recoup some of the money lost to fees, Xplace is a great option, with a token slated towards the end of the year.

Different sauce

The products we mentioned so far largely compete by offering the same breadth of features, but some approach the sector from a different angle, as you shall see.

Payy

@payy_link focuses on privacy-first stablecoin payments facilitated through its own L2 network atop Ethereum.

In practice, this brings several benefits for the cypherpunks that none of the above apps offer at the moment, with the biggest being that your onchain wallet balances and activity cannot be linked to card transactions thanks to zk proofs.

Although I know some people managed to get their hands on the physical card with the nice feature of lighting up whenever a contactless payment is made, it's currently not available to order, and for now, you’ll have to make do with the virtual card.

The second benefit appears whenever users send money to each other using the, I must say, rather convenient QR code or link generation system. In these cases, payments are fully private, with the sender, receiver, amount, and asset all hidden.

It's important to note that the app is stablecoin-first, meaning you can either deposit or withdraw stablecoins, and it currently does not offer fiat-to-crypto conversions.

So if you’ve ever wanted to send some money to your friends or family without explaining how any of this works, this app makes it dead simple and retains your privacy.

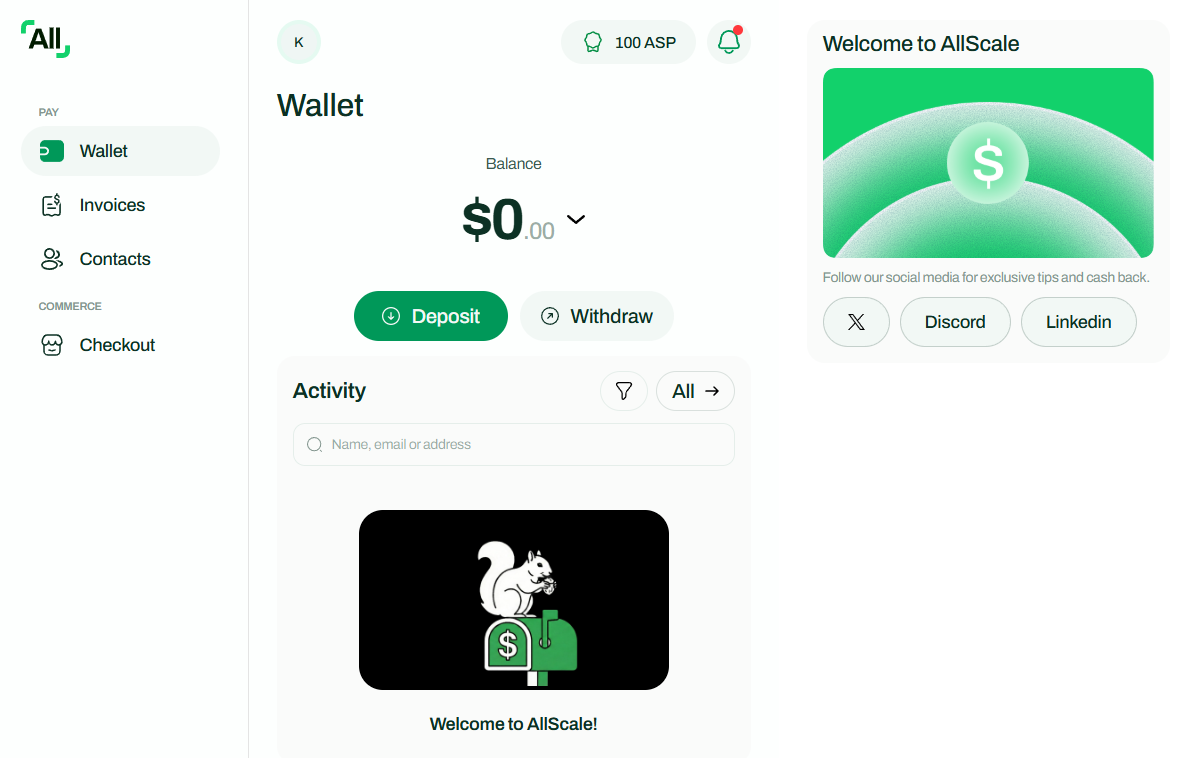

AllScale

Instead of going for the everyday spender, @allscaleio aims to become the stablecoin-native bank for businesses. In practice, AllScale is a desktop app, and at its core sits a non-custodial stablecoin wallet.

From there, a wide range of actions is available to streamline your business’s operations, such as:

- Sending payroll to your employees across the globe, including EOR services in 100+ countries, alleviates the pain of paperwork and, thanks to stablecoins, makes it cheap.

- Create, e-sign, and send professional contracts and invoices, and get paid by clients in their preferred method (credit card, wire transfer, or crypto) and instantly receive stablecoins.

- And to top it all off, the AllScale Checkout feature lets you create storefronts for your business and accept crypto or traditional methods with instant stablecoin settlement, built-in Auto-KYT compliance, and zero-knowledge data protection.

SurfCash

While the debit card solves the hurdle for everyday payments, it does not account for all scenarios.

Firstly, you can’t always pay utility bills, rent, or other bills with a debit card. Also, larger corporate landlords won’t accept cash, which means you still need to deposit funds into a traditional bank account. If you’re living abroad, this is far from ideal.

Secondly, in the SEA region, most businesses use VietQR, Pix, PromptPay, and other local payment systems and often rely on QR codes rather than credit card terminals. Here, you’ll be left scrambling for an ATM or looking for locals who conduct P2P exchanges from crypto to cash.

Since @surfcashx directly taps into local payment rails, users can simply scan any standard merchant QR code, and the app converts USDC and pushes local fiat to the merchant’s account. No need for the merchant to accept crypto, for the merchant to have a card terminal, or for you to open a new account.

Honorable mentions

When reading this list, some of you might’ve noticed it was missing a few players you’d normally see on such lists.

While they're doing notable things in the neobank arena, we've limited this list to companies most closely aligned with the framework and criteria we defined at the beginning of this article.

Nonetheless, if there's a product not listed in this article that you think should be included, let us know.

@Cypher_HQ_, @useTria, @galaxyoneapp, @vPay_Global, @xapobankapp, @itstuyo

Conclusion

Contrary to popular belief, the crypto card phenomenon is not new, and most CEXs have offered them for a long time.

What’s new are crypto-native solutions that combine onchain infrastructure with traditional banking services, while allowing users to retain ownership of their crypto assets. This is important because some of the listed apps are not non-custodial, so I’ve left that detail out for you to DYOR. After all, it’s your money.

Setting aside the different features and solutions these apps provide, I want to highlight the true heroes of the neobank story: the infrastructure providers. I categorize them as Banking-as-a-Service operators, as they bridge the gap between TradFi and crypto, packaging it into simple API calls or SDKs.

By handling compliance, KYC, KYB, AML checks, card issuance, FX conversion, fiat-to-crypto (and vice versa) ramps, i.e., the most challenging aspects of launching such a product, neobanks can deploy their services rapidly without the need to develop proprietary infrastructure or acquire licenses.

Companies like @moonpay, @iron, @wirexdevelopers, @crossmint, @Stablecoin, @lightspark, @multisig, and others specialize in bridging that gap, eliminating the highest-friction point.

Just a few years ago, this wasn’t possible without serious money. Today, judging by the sheer number of apps popping up, that barrier has been lowered significantly, all thanks to these services.

And for that, I salute them because owning my money has never felt better.

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)