.webp)

Reading time: 6m 54s

In a seemingly everlasting endeavor to bring all of finance onchain, we’ve been in a constant cat-and-mouse game of innovation and reiteration to find the perfect formula that can make fully onchain markets more efficient than TradFi markets.

Although we’ve barely landed a scratch on our TradFi counterparts, we continue to see this industry fight. Will David beat Goliath this time?

Over the last year, we’ve seen the sneaky rise of what many crypto proponents claim will be the innovation to finally take the crypto industry to the next level. That product is proprietary automated market makers, or propAMMs for short.

PropAMMs have facilitated over 60% of Solana’s onchain spot trading volume, with aggregators like Jupiter now being heavily reliant on propAMMs for liquidity. During peak times, they averaged well over $1 billion in daily trading volume and are estimated to be 1000x more efficient in compute terms for oracle updates.

Although everybody will tell you that it’s the next best thing since sliced bread, there is a darker truth beneath the surface that very few people talk about.

So let’s get into everything you need to know about propAMMs.

What is a PropAMM?

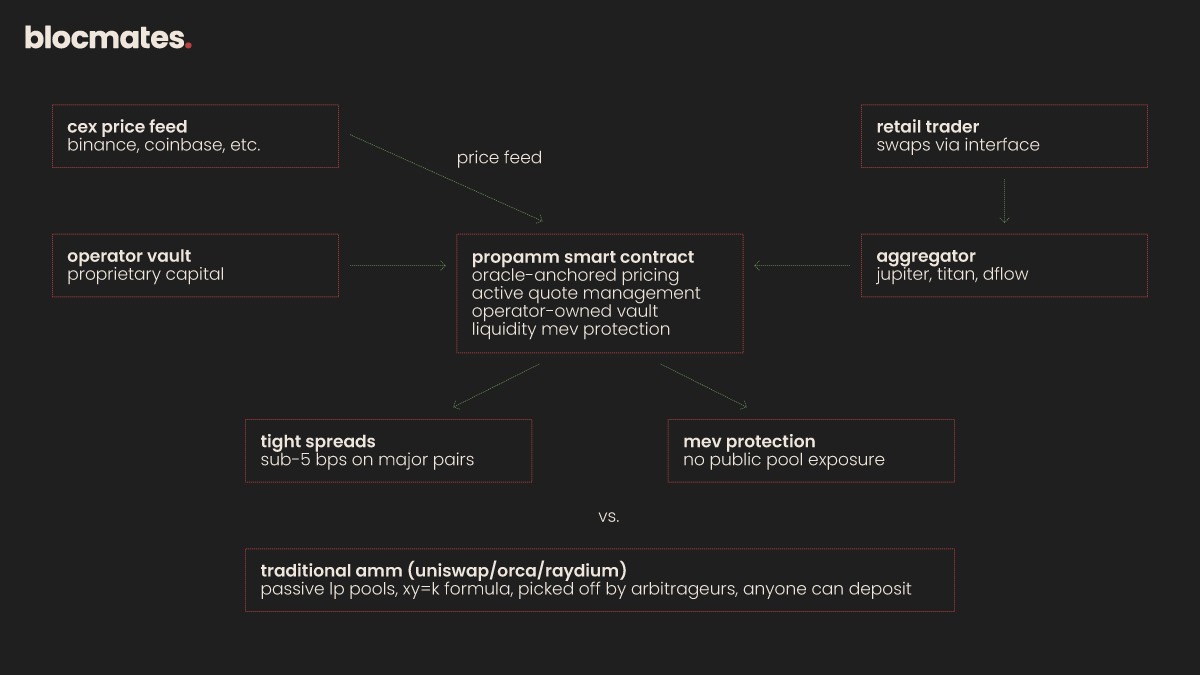

PropAMMs are an automated onchain market-making primitive that operate on the backend of DEXs/aggregators rather than being directly client-facing.

A market-making/trading firm can encode its market-making strategy into a smart contract, which then gets plugged into the backend of an aggregator like Jupiter, for example, from where it automatically executes and gives efficient prices for traders.

Here’s how it works.

There are two components to this setup. An offchain pricing engine and the onchain smart contract.

Both components constantly communicate with each other.

The offchain pricing engine constantly monitors price feeds from top CEXs like Binance, Bybit, or any other top CEX and computes a fair price, which is sent to the onchain contract via an oracle and a signed transaction.

The onchain is essentially a vault that contains the liquidity deployed by these market-making firms, which also executes the trades.

So when the offchain engine’s oracle update lands onchain, the contract is effectively receiving a range of executable prices across ticks. Each tick represents a configurable share of the inventory pool in the vault.

If the price of ETH is $2,493.5 according to the oracle, the contract might place ask liquidity at $2,493.55, $2,493.63, $2,493.7, and so on. This is just a hypothetical example, by the way.

Then, when it comes to placing a trade, a retail trader like you and me doesn’t interact with this propAMM. You place a trade on a DEX or aggregator that has propAMM running in the background.

When a trade is placed, the propAMM contract runs through a checklist on a number of things, like oracle freshness, recent flow history, pool inventory, and a whole plethora of other things.

Based on the criteria, the propAMM effectively scores each transaction before committing to a price, unlike a traditional AMM that executes every trade identically.

So, if a trader is looking to buy 100 ETH, it may get filled across the closest two ticks or five ticks, depending on what the contract deems most efficient based on the criteria.

The overarching idea is that propAMMs are the most efficient onchain pricing mechanism, with a study done by Jump Crypto finding that across 20 million transactions executed through propAMMs, 90%-91% of them were cheaper for the end user than even being VIP tier on any of the top CEXs.

This brings us to the first aspect of propAMMs, the good.

The good

The main reason why propAMMs are lauded as this needle-moving innovation for onchain markets are because they are more efficient than traditional AMMs, but also more efficient than CEXs at times.

Traditional AMMs use the x*y=k formula, where two assets are paired in a pool, and the price is determined by the ratio of assets in the pool.

This works fine, but in reality, the AMM doesn’t know the real price. It relies on arbitrageurs to bring the pool to the asset's price on CEXs/other venues. This leaves room for liquidity providers to get picked off. Not ideal.

Yeah, you do have the new school AMMs like UniV3 and DLMMs, which are much better, but they still aren’t optimal.

Onchain orderbooks are another solution to enhance efficiency with better pricing, but they are extremely expensive to run on a blockchain, as every price change, order update, cancellation, and any other action costs money. Simply not ideal for large volumes of onchain trading at scale.

PropAMMs offer tighter spreads and better execution by simply plugging in a market-making contract into the backend of existing DEXs/aggregators.

Beyond this, it’s a more capital-efficient system when compared to any other onchain trading mechanism, especially for spot trading.

Another key benefit is that the liquidity provision is fully programmable and dynamic. It auto-adjusts based on order types and a variety of other criteria to maximize efficiency, offering traders the best prices with minimal slippage.

Now here’s where a double-edged sword comes in.

Since propAMMs are ‘closed’, they are protected from MEV attacks, as there is no public pool of transactions for sandwich attacks and related attacks. On the other hand, it also leads us to the next section of this article.

The bad

Centralized, no permissionless LP, integration gatekeeping, no long tail assets.

For all the good that propAMMs offer in terms of execution, they are also completely antithetical to all the core pillars of DeFi.

For security purposes, propAMMs are centralized and closed by design. Although that means most of you inept LPs won’t lose a fortune to impermanent loss or get MEV attacked, it also introduces a massive centralized point of failure.

Only the developer of the propAMM and other approved entities can deposit into the vault. This isn’t a permissionless LP that anyone with a wallet can deploy, which means you have to fully trust that the company is not doing anything shady/manipulative, as it is incredibly difficult to audit how exactly they are operating.

Although centralization is the main ‘BAD’ aspect of this, there are also other drawbacks.

The reliance on CEX feeds to derive pricing means that they aren’t well-suited for market-making long tail assets. Something that is very popular among onchain retail traders looking to get in early before the VCs and funds.

Then there’s also an element of integration gatekeeping.

These propAMMs rely on aggregators and DEXs. At one point, HumidiFi derived 95% of its volume from Jupiter. This means there is an additional permissioned layer, as the propAMM must approach the aggregator's team before it is integrated. No permissionless composability, like is usually the case in DeFi.

But beyond the centralization and permissioned nature of propAMMs, there is actually something much uglier brewing under the surface.

The ugly

A recent study conducted by 0x found that behind the closed and opaque nature of propAMMs, there has been a shocking amount of exploitation of retail users.

So let's get into it.

The telltale sign of concern is that the PropAMM narrative is largely told by the people running them - Jump Crypto, Temporal, Wintermute. Their framing is straightforward: tighter spreads, better execution, and DeFi finally competing with Binance.

Pretty neat, right?

Behind the narratives, marketing, and opacity lies an ugly truth: the same funds and trading firms are further exploiting crypto users.

Quote spoofing

This is where the propAMM publishes an attractive price, as advertised, at the very end (the last 200ms) of a block. Then, in the very beginning of the next block, it reprices to a worse price.

The way aggregators work is that they route trades based on the best quote price at the time of routing. So, towards the end of the block, the propAMM offers the most attractive price, which makes the aggregator choose that price.

Then, in the very next few milliseconds, when the trade is already being routed through the propAMM, the price quietly reprices to a worse level, and the trader ends up bearing the brunt.

The study shows that the impact of this quote spoofing is roughly 5-10 basis points per trade, yes, you heard that right, PER TRADE.

So if $1 billion in monthly volume is routed through a propAMM, they can extract roughly $500k per month through quote spoofing. Usually much more.

Random spread fluctuations

Although similar in nature to quote spoofing, this is harder to detect because it's more passive and structural. It can happen as a result of simply running frequent oracle updates.

This is what it looks like.

A propAMM quotes a tight spread to win the routing decision from aggregators. In the milliseconds between the aggregator querying the price and the trade actually settling onchain, the contract updates its oracle to show a worse price.

The trade settles at the worst level. The aggregator routed correctly based on what it saw, but the price the trader actually gets is materially different.

It's a repricing pattern that simply exploits the latency between quote and settlement.

Concluding thoughts

Look, it's crypto. The only constant in this industry is that there is somebody on the other end trying to fuck you over, and there is somebody engaging in shady, unethical behavior.

At the end of the day, it comes down to a choice.

Are you someone who only cares about efficiency and is willing to blindly trust the firms running these propAMMs?

Or, are you someone who believes the way propAMMs operate completely defeats the purpose of DeFi, meaning you are willing to sacrifice on that “efficiency” for an alternative solution down the road?

It’s difficult. But in order to beat TradFi, building TradFi onchain shouldn’t be the answer.

Yes, there are great things that can be taken away from the innovation itself, but beyond that, it’s important not to lose sight of the benefits of a permissionless and trustless future.

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

%20(1).webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)